Why Do You Owe More In Taxes This Year?

“I thought there was a tax break. Last year I got a refund. This year, I owe money to the IRS. How did this happen and what do I need to change to fix this?”

As more and more people file their taxes for 2018, the situation described above seems to be the norm instead of the exception to the rule. Taxpayers are realizing that either their tax refund is lower, they owe money for the first time, or their tax bill is larger than it normally is. While this is a shock to many families and individuals, we saw this issue coming in February of 2018. We even wrote an article at that time titled “Warning To All Employees: Review The Tax Withholding In Your Paycheck Otherwise A Big Tax Bill May Be Waiting For You”.

Below we will highlight some of the catalysts of this issue and provide you with some strategies on how to better prepare for the coming tax year.

New Tax Withholding Tables

When tax reform was passed, the government issued new federal income tax withholding tables to your employer in February which provides them with the amount that they should withhold from your paycheck for tax purposes. Since the federal tax brackets dropped, so did the withholding tables. In February 2018, this seemed like a great thing because most taxpayers saw an increase in their take home pay. However, it simultaneously created a big tax problem for a lot of employees.

Gross Income vs. Taxable Income

There is a difference between your “gross income” and your “taxable income”. If your salary is $80,000 per year, that is your gross income. At tax time, you get to take deductions against your gross income, to reach your total “taxable income” which is a lower amount. Your taxable income is the amount that you actually have to pay taxes on.

For example, you have a married couple, husband has a W2 for $60,000 and his wife has a W2 for $70,000. Their combined gross income is $130,000. Let’s assume they take the standard deduction in 2018 which is a $24,000 deduction. Their total taxable income for 2018 is $106,000.

Impact of Tax Reform

While tax forms did bring lower federal income tax brackets, it also made a lot of changes to the deduction side of the equation. For those of us living in New York, California, and other high tax states, the biggest change was probably the $10,000 cap that they placed on property taxes and state income taxes. The other big change for taxpayers with children was the elimination of the personal exemption deduction which was replaced with a credit. The personal exemption change works for some taxpayers and against others. For more on this topic reference: More Taxpayers Will Qualify For The Child Tax Credit In 2018

For that married couple above that made $130,000 in 2018, under the new tax rules their total taxable income may be $106,000 but if they applied the old tax rules it may have only been $95,000. People are finding out that while the federal tax rates dropped, their total taxable income for the year increased because the higher standard deduction did not make up for all of the itemized deductions that were lost under the new tax rules.

To further aggravate that wound, at the beginning of 2018, the federal government instructed your employer to withhold less federal income tax from your paycheck which put some taxpayers further behind on their withholdings. If you were used to getting a refund when you filed your taxes, technically you may have already received it throughout the year in your paycheck but you just didn’t know it. There are of course taxpayers in the even more difficult camp that were banking on getting a refund only to find out that they actually owe money to the IRS.

How Do You Fix This?

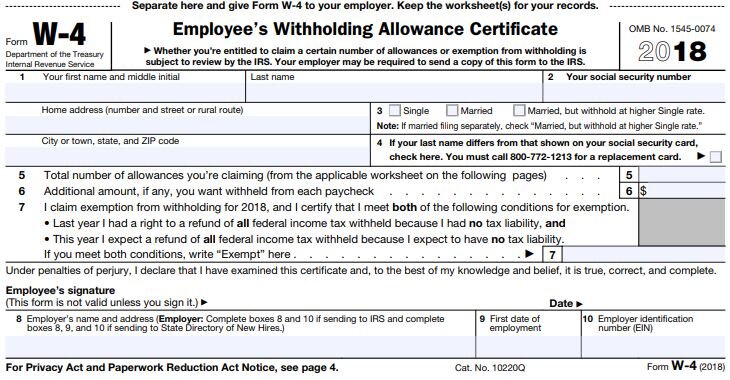

If you unexpectedly owed money to the IRS this year or if you want to restore that refund that you typically receive when you file your taxes, you are going to have to change your tax withholding amount with your employer. You have to request a Form W-4 from your employer. I looks like this……

Form W-4

You can reduce the number of allowances that you are claiming on line 5 or you can instruct your employer to withhold an additional flat dollar amount each pay period on line 6.

There are also other options beside increasing your tax withholdings like increasing your contributions to your 401(k) account or contributing money to a Health Savings Account for your health expenses. These moves may assist you in reducing your taxable income which could lead to a lower tax liability.

Consult With Your Accountant

While I have highlighted the more common catalysts leading to this under withholding issue, there were a lot of changes made to the tax rules so there could have been other factors that led to your higher tax liability this year. Your gross income could have been higher, maybe you took a distribution from an IRA account, or you have realized gains from an investment that you sold during the year. You really have to work with your tax professional to identify what triggered the additional tax liability and determine what action should be taken to reduce your tax liability going forward.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future