The New PPP Loan Forgiveness Application & Early Submission

It just keeps getting better for small business owners. On June 17, 2020, the SBA released the updated PPP Forgiveness Application. In addition to making the forgiveness application easier to complete, the new application also provided additional guidance on a number of questions that arose when the SBA extended the forgiveness period to 24 weeks.

But it gets better. On June 22nd, the SBA issued additional guidance allowing borrowers to apply for forgiveness prior to the end of the 8 week or 24 week covered period if the borrowers had already spent their full PPP loan amount.

With so much that has happened since the Paycheck Protection Program was first launched. Here is a quick recap of the events leading up to the release of the new PPP Forgiveness Application and the new guidance:

March 27, 2020: Congress passed the CARES Act which created the PPP Loan Program

April 2020: The SBA opens the window for companies to access the PPP Loans

May 15, 2020: The SBA released the first version of the PPP Loan Forgiveness Application

June 5, 2020: Congress passed the PPP Flexibility Act

Extended Covered Period to 24 Weeks

Reduced payroll cost requirement from 75% to 60%

Extended rehire safe harbor from June 30th to December 31st

June 17, 2020: SBA releases the updated PPP Forgiveness Application

June 22, 2020: SBA allows companies to apply for forgiveness prior to the end of the covered period

In this article we are going to address:

How to complete the new PPP Forgiveness Application

The EZ Forgiveness Application vs the Long Form PPP Forgiveness Application

Which companies are eligible to submit the PPP EZ Forgiveness Application

The new max comp limits of $20,833 and $46,154

Ability to apply for forgiveness prior to the end of the covered period

PPP EZ Forgiveness Application – Form 3508EZ

Instead of releasing just one forgiveness application, the SBA actually released two separate PPP Forgiveness applications:

PPP Loan Forgiveness EZ - Form 3508EZ

PPP Loan Forgiveness Revised – Form 3508

The good news is both applications are much shorter than the initial 12 page Forgiveness Application that was released on May 15th, but making it even better, we now also have an EZ application which will make the Paycheck Protection Program Forgiveness Application process even easier for many companies. The EZ application is only 3 pages long. giving companies access to a shorter forgiveness application made sense to us because the PPP loan amount was calculated based on 10 weeks of payroll and with the extension of the covered period to 24 weeks, companies now have 24 weeks of payroll to cover a loan amount based on 10 weeks. The result, most companies will most likely be able to reach the full PPP forgiveness amount on Payroll Costs alone without having to take into account rent, utilities, and other qualified expenses.

Who Is Eligible To Use The PPP EZ Forgiveness Application?

Companies will only be able to utilize the PPP EZ Forgiveness Application if they satisfy one of the following three criteria. I will give you the short and sweet version first followed by the long technical version of the criteria. Short and sweet:

You have no employees (Sole Proprietors or Owner Only Entities)

You did not reduce employee HEADCOUNT (FTE’s) and did not reduce WAGES by more than 25% for employees making less than $100,000 in 2019 during the covered period compared to January 1, 2020 – March 31, 2020

You did not reduce employee WAGES by more than 25% for employees making less than $100,000 in 2019 but you reduced the number of FTE’s during the covered period. However, the reduction in FTE’s was because CDC, OSHA, or other government agencies limited the capacity that the business could operate at during the covered period.

Here is the long technical version of the three criteria:

The borrower is a self-employed individual, independent contractor, or sole proprietor who had no employees at the time of the PPP loan application and did not include any employee salaries in the computation of the average monthly payroll in the PPP Application Form (SBA Form 2483).

The borrower did not reduce annual salary or hourly wages of any employee by more than 25% during the covered period compared to January 1, 2020 and March 31, 2020 AND The borrower did not reduce the number of employees or the average paid hours of employees between January 1, 2020 and the end of the covered period.

The borrower did not reduce annual salary or hourly wages of any employee by more than 25% during the covered period compared to January 1, 2020 – March 31, 2020 AND the borrower was unable to operate during the covered period at the same level of business activity as before February 15, 2020, due to compliance with requirements established or guidelines issued between March 1, 2020 and December 31, 2020 by the Secretary of Health, CDC, or OSHA, related to the maintenance of standards of sanitation, social distancing, or any other work or customer safety requirement related to COVID-19.

Again, you just have to be able to satisfy ONE of the three criteria listed above. You do not need to satisfy all three.

Reduction In Wages of Employees

Per the criteria mentioned above, if you reduced wages by more than 25% during the covered period for employees that made under $100,000 in 2019, you would not be able to complete the PPP EZ Application.

At first look this seems pretty self-explanatory but it’s really not. If you just read that statement for what it is, it would lead you to look at just your year-end payroll report for 2019, determine who had an annual compensation of $100,000 or less, and then you would look to see if any of those employees had wage reductions of greater than 25% during the covered period.

However, the way the guidance was written, it would imply that the $100,000 annualized compensation applies on a per pay period basis, meaning if in ANY pay period in 2019, you paid an employee higher than a $100,000 annualized wage, that employee would not be subject to the wage reduction calculation. It’s best to illustrate this in an example.

Let’s say Jim is one of your employees and in 2019 you paid Jim a total of $80,000. His $80,000 in compensation included $75,000 in base pay plus his $5,000 annual bonus that was paid to him in the final pay period in December. Your payroll is run on a biweekly basis meaning for purposes of assessing the $100,000 annual compensation limit, any employee that received more than $3,846.15 in any bi-weekly pay period in 2019, would not be subject to the wage reduction calculation. Since in Jim’s last paycheck of 2019, he received his regular bi-weekly wage of $2,884.15 plus his annual bonus of $5,000, his final paycheck in December was for $7,884.15. Thus Jim is excluded from the wage reduction calculation and can be ignored for purposes of assessing whether or not you are eligible to complete the PPP EZ Forgiveness Application even though his total compensation for 2019 was under $100,000.

Whether or not it was the SBA’s intention to assess the $100,000 limit in this manner, we cannot be 100% certain, but as of today, that’s how it reads.

Now that we have all of that fun stuff out of the way, let’s get to completing the PPP Forgiveness EZ Application. For the purpose of this article we are focusing on the EZ application because given the new 24 week covered period, the new safe harbor exceptions, and the ability to submit the application early, we expect that a lot of companies will qualify to submit the EZ Forgiveness application.

How To Complete the PPP Loan Forgiveness EZ Application

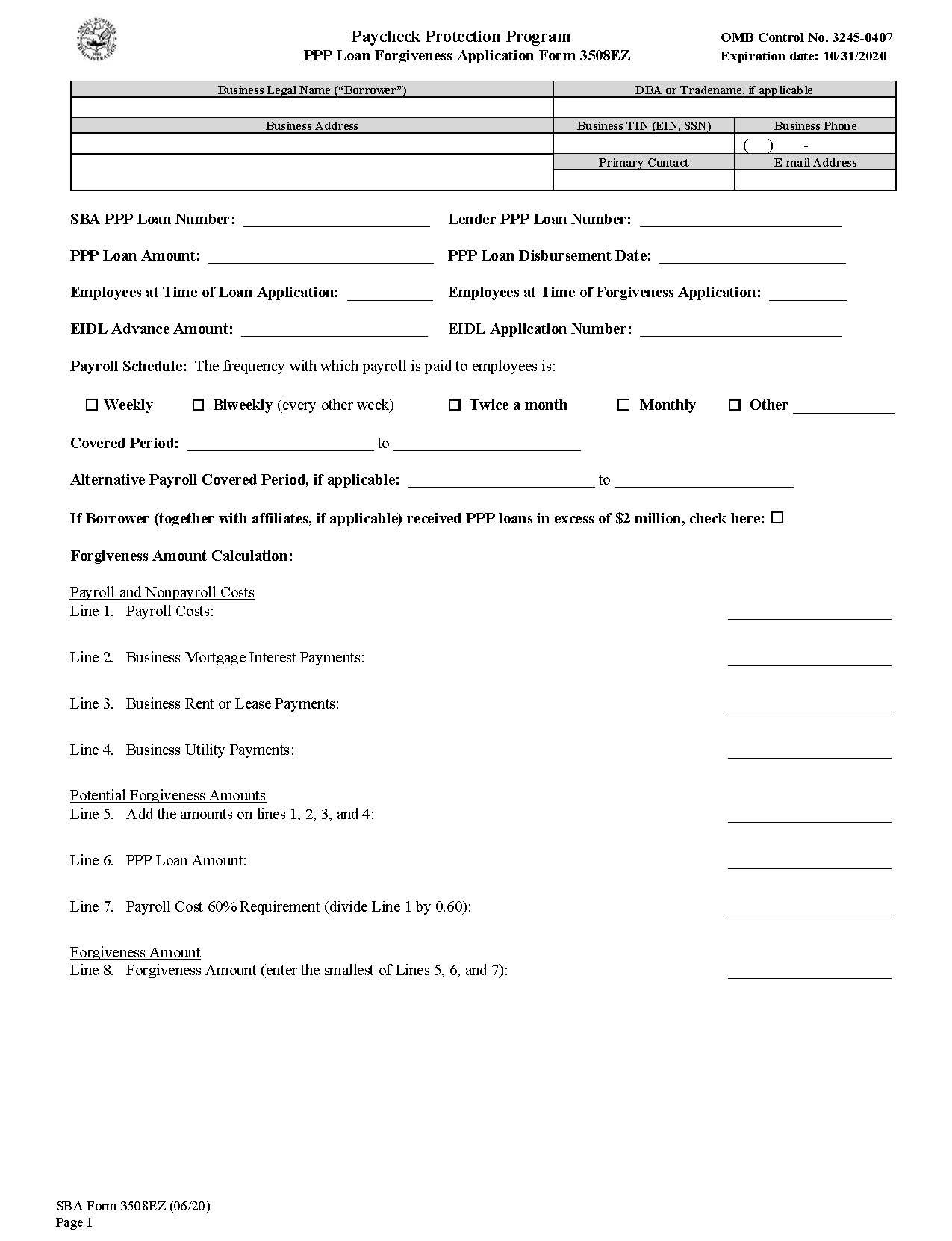

Here is what the first page of the PPP Loan Forgiveness Application Form 3508EZ looks like:

SBA PPP Loan Forgiveness Application

There are no worksheets that need to be completed!! It’s just this page and a second page that has a bunch of lines that Borrower has to initial certifying that they followed all of the rules associated with the PPP Loan Program.

Top Section: The top section of the form is just general information on your company, your PPP loan, and your payroll schedule.

Covered Period: If your PPP loan was issued prior to June 5th, you have the option to either select the 8 week covered period or 24 week covered period. The covered period beings on the date that you received the PPP loan. One might ask, why would anyone choose the 8 week covered period? There are actually a few reasons.

Reason 1: The company has already spent all of the PPP loan money within the 8 week period.

Reason 2: By electing the 24 week covered period, it also potentially creates a 24 week covered period for the FTE (full time equivalent employee) calculation and the 25% wage reduction calculation. But the guidance that we just received from the SBA on June 22nd which allows companies to file the forgiveness application prior to the end of the covered period could change this. The SBA issued guidance allowing companies to file the forgiveness application early but they did clarify what happens if the company receives full forgiveness but then reduces wages or FTE’s prior the end of the full 24 week covered period. We are flying blind right now until we get more guidance from the SBA on this.

For companies that have not spent 100% of their PPP loan amount, it think this new guidance creates a wait and see approach, as to whether the company should select the 8 week covered period or select the 24 week covered period with the ability to apply for forgiveness early.

For companies that have been able to spend 80% to 90% of their PPP loan during the 8 week covered period, that were planning on reducing employees or wages after the covered period was complete, depending on the guidance that the SBA issues, it may be advantageous for those companies to stick with the 8 week period, as opposed to being subject to the 24 week covered period calculations that could reduce the forgiveness amount.

The only other downside to selecting the 8 week period is the compensation limit for each owner and each employee is capped at a lower level compared to the 24 week covered period. We will cover this when we get to the Payroll Cost portion of the forgiveness application.

What is the “End Date” of your Covered Period?

With this change, I’m not really sure what is considered the new “end date” for the Covered Period. Being able to apply for forgiveness prior to the end of the covered period makes the end date of the covered period seem irrelevant. Maybe the new end date of the covered period is the day that you submit the forgiveness application. That makes more sense to me because that would be the time period that you would be submitting payroll data for and the nonpayroll expenses that have either been paid or incurred, but it’s not clear at this point.

Alternative Payroll Covered Period: As mentioned above, the covered period begins the day the PPP loan hit your business checking account. However, companies are allowed to elect to begin their covered period at the beginning of their next payroll period following the receipt of the PPP Loan.

Example: Company XYZ has a bi-weekly payroll schedule. They receive their PPP loan on April 26th in the middle of one of their payroll periods. The company could voluntarily elect an alternative payroll covered period beginning on May 5th with would be the first day of the next payroll period. This could make the calculations a little easier since the payroll dates will match up with a covered period.

The extension of the covered period to 24 weeks and the ability to file for forgiveness early may render the Payroll Covered Period feature irrelevant for many companies. It was more relevant when companies had to make sure they could fit in their 8 weeks of payroll into their 8 week covered period to maximize their forgiveness amount.

Line 1: Payroll Costs: The new PPP Forgiveness Application came with different compensation limits for owner-employees and regular employees.

Sole Proprietors & Owner Only Entities

If you are a sole proprietor or owner only entity, the Payroll Cost calculation is going to be very easy. For each owner, the payroll cost is the LESSER OF $20,833 or 2.5 months of compensation from 2019. If you are a sole proprietor that made more than $100,000 in 2019, you can just enter $20,833 on that line and move on. For companies with multiple owners with no employees, you would just total up the compensation amounts with the cap for each owner and enter it on that line.

For Companies With Employees

If your company has employees and satisfies one of the three criteria making you eligible to complete the PPP Forgiveness EZ Application, using your own personal excel spreadsheet, you can total up the Payroll Costs for the owners and employees as follows:

Different Max Compensation Limits For Owner-Employees & Employees

The new forgiveness application provided updated guidance on the maximum compensation allowed for both owners and employees during the covered period. Under the old 8 week covered period, compensation was capped at $15,385 for both owners and employees. With the new 24 week covered period, compensation is capped at the following:

Owner-employees: $20,833

Employees: $46,154

The math makes sense because it’s the $100,000 compensation cap, dividend by 52 weeks, multiplied by a 24 week forgiveness period. Unfortunately for owners, the cap was only increased to $20,833 and there is an additional restriction. The compensation cap for owner-employees will be the LESSER OF:

$20,833; or

5 months of the owners 2019 compensation

But also using the same math, it would seem prudent that the $46,154 compensation cap for each employee would be reduced if you submit your PPP Forgiveness application prior to the end of the covered period. Example: If you file your forgiveness application after 15 weeks it would seem prudent that each employee's compensation would be limited to $28,846 which is the $100,000 cap, divided by 52 weeks, multiplied by 15 weeks, but the SBA has yet to issue guidance on this.

So column 1 of your excel spreadsheet is compensation paid during the covered period to owner-employees and employees with these compensation caps imposed.

For Employees: Health & Retirement Contributions Are In Addition To Comp Limit

The next two columns in your excel spreadsheet should be “Health Insurance Costs” and “Employer Retirement Contributions”.

For employees, the maximum compensation for any single non-owner employee during the 24 week covered period is $46,154, but that cap just applies to their compensation. In addition to the $46,154 cap, the company can also include the following amounts in “Payroll Costs” for each employee:

Employer contributions for employee health insurance

Employer contributions to employee retirement plans

For sole proprietors and partners, these amounts are not counted in addition to the $20,833 for owner employees. It’s not 100% clear how retirement contributions will work for owner-employees of S-corp and C-corp, but as of today, I would guess that they are going to be limited as well to the $20,833 for compensation, health insurance, and employer contributions to retirement plans. Guidance needed from the SBA on this.

But again, we expect this to be irrelevant for many companies because most companies will be able to meet the full forgiveness amount on just the 24 weeks of payroll without having to factor in these other “Payroll Costs”.

Total up all of those columns on your excel spreadsheet and you have reached your Line 1: Payroll Cost for the forgiveness application.

Line 2: Business Mortgage Interest: Any interest payments on a covered mortgage obligation that was in place prior to February 15, 2020. As of right now the definition is either PAID or INCURRED during the covered period.

Line 3: Rent or Lease Payments: Payments of rent during the covered period for a lease that was in place prior to February 15, 2020. Similar to mortgage interest, the cost can either be PAID or INCURRED during the covered period.

Line 4: Business Utility Payments: The payment of utilities during the covered period include electricity, gas, water, transportation, telephone , and internet services that were in place prior to February 15, 2020.

The Forgiveness Calculation

The rest of the form, Lines 5 – 8, are fairly self explanatory. You are adding up your total qualified costs in comparing that to your loan amount to determine the percentage of your forgiveness.

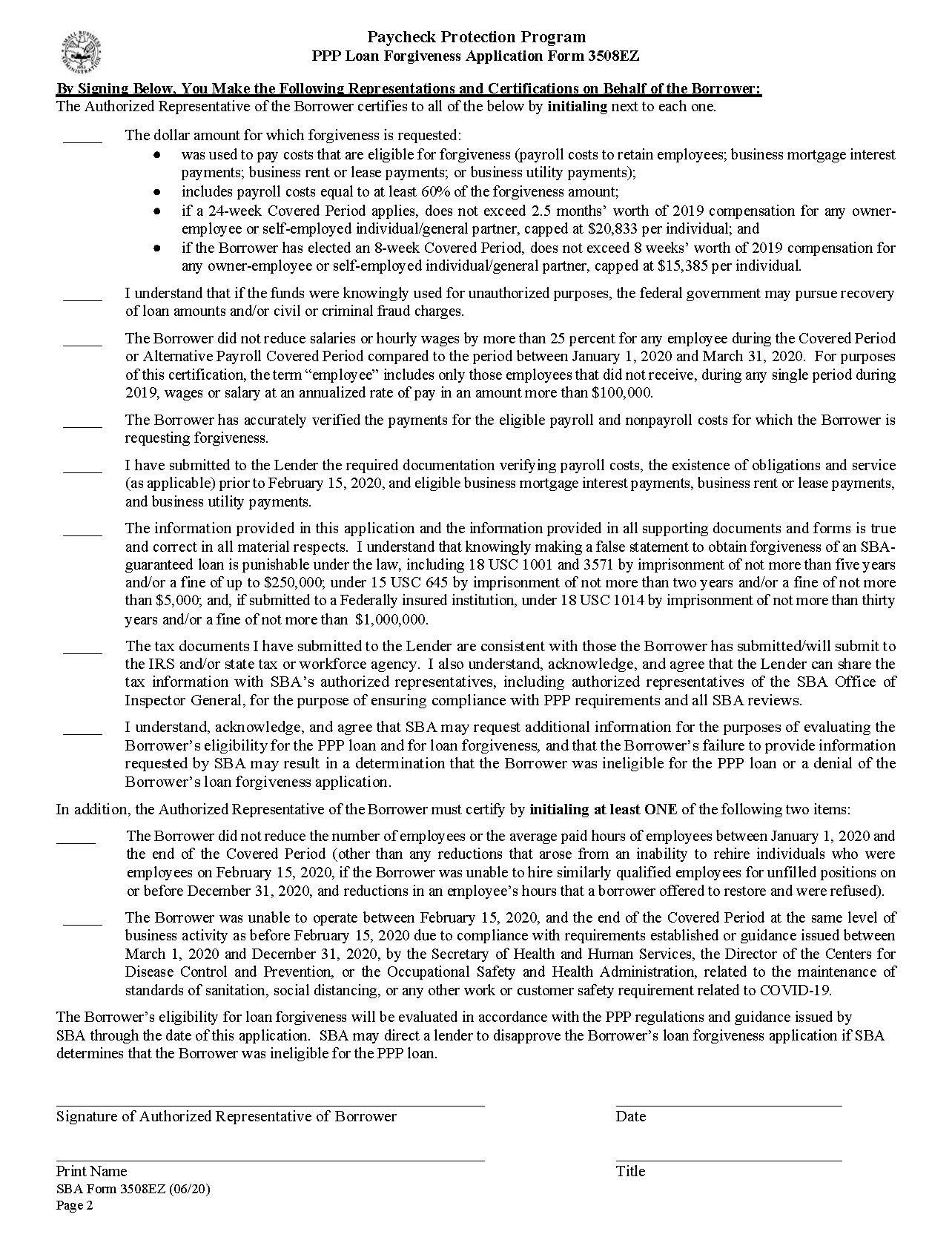

Page 2: PPP Loan Forgiveness EZ Application

Page 2 of the PPP EZ Loan Application looks like this:

New PPP Forgiveness Application

The Borrower just has to initial on each line, sign the bottom of the form, and the application is complete. The next step is to gather all the supporting documentation for the expenses that are listed on the PPP application and submit the forgiveness application with those supporting documents to your bank to formally begin the forgiveness process. the bank has 60 days from the date you submit your forgiveness application to either accept the application or reject it.

The PPP Loan Forgiveness Application - Form 3508 ("Long Form")

If you don't qualify to submit the EZ Loan Forgiveness Application, then you would have to complete what I call the PPP Loan Forgiveness Long Form. Now even though I call it the long form it's still shorter then the 12 page loan forgiveness application that was released by the SBA on May 15th. The long form requires you to:

Complete the PPP Application Worksheets

Run the FTE Calculations

Run the Wage Reduction Calculation

Determine if you satisfy any of the Safe Harbors

We will cover the long form in a separate article.

Michael Ruger

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.