Biden's New SAVE Plan: Lower Student Loan Payments with Forgiveness

With student loan payments set to restart in October 2023, the Biden Administration recently announced a new student loan income-based repayment plan called the SAVE Plan. Not only is the SAVE plan going to significantly lower the required monthly payment for both undergraduate and graduate student loans but there is also a 10-year to 25-year forgiveness period built into the new program. While the new SAVE program is superior in many ways when compared to the current student loan repayment options, it will not be the right fit for everyone.

With student loan payments set to restart in October 2023, the Biden Administration recently announced a new student loan income-based repayment plan called the SAVE Plan. Not only is the SAVE plan going to significantly lower the required monthly payment for both undergraduate and graduate student loans for many borrowers, but there is also a 10-year to 25-year forgiveness period built into the new program. While the new SAVE program is superior in many ways to the current student loan repayment options, it will not be the right fit for everyone. In this article, we will cover:

How does the new SAVE Plan work?

How does the SAVE program compare to other student loan repayment options?

How are the monthly payments calculated under the SAVE program?

What type of loans qualify for the SAVE plan?

How do you apply for the new SAVE plan?

How does loan forgiveness work under the SAVE plan?

Who should avoid enrolling in the SAVE plan?

The new Fresh Start Plan to wipe away defaults and delinquent payments in the past

The SAVE Student Loan Repayment Plan

The SAVE plan is a new Income-Driven Repayment Plan (IDR) for student loans that also contains a loan forgiveness feature. The monthly payments under this program are based on a borrower’s annual income and household size. Once a borrower is enrolled in the SAVE program, any balance remaining on the loan is forgiven after a specified number of years.

Replacing The REPAYE Plan

The SAVE Plan will be replacing the current REPAYE plan, but the terms associated with the SAVE plan are enhanced. Any borrowers previously enrolled in the REPAYE plan will automatically be transitioned to the SAVE plan.

What Types of Loans Are Eligible?

Only federal student loans are eligible for the SAVE plan. Private student loans and Parent PLUS loans are not eligible for this repayment option. Both federal undergraduate and graduate student loans are eligible for the SAVE plan, but the monthly payment calculation and forgiveness terms differ depending on whether the borrower has undergraduate loans, graduate loans, or both.

SAVE Plan Monthly Payment Calculation

There are several income-driven repayment plans currently available to borrowers, but those plans typically require the borrower to commit 10% to 20% of their discretionary income toward their student loan payments each year. The new SAVE plan will only require individuals with undergraduate loans to commit 5% of their discretionary income toward their student loan payments each year. As mentioned above, individuals currently enrolled in the REPAYE plan, which requires a 10% of income payment, will automatically be transitioned to the SAVE plan, which could lower their monthly payment amount.

Definition of Income

The SAVE program limits the borrower to only having to pay 5% of their household discretionary income toward their undergraduate loan balance each year. While that seems pretty straightforward, there are a few terms that we need to define here. First, it’s 5% of household income, meaning if you are married and file a joint tax return, you must use your combined income when applying for the SAVE plan. If there are two incomes, that could naturally raise the amount you pay each month toward your student loans.

However, if a borrower is married but chooses to file their tax return, married filing separately instead of married filing jointly, then only the spouse applying for the SAVE plan has to report their income. While at first this might seem like a no-brainer, I would urge extreme caution before electing to file your tax return married filing separately. While this tactic could lower the required monthly payments for your student loan and potentially increase the forgiveness amount at the end, electing to file as married filing separately could dramatically increase your overall tax liability depending on the income level between the two spouses. It creates a situation where you could win on the student loan side but lose on the tax side. For this reason, I strongly encourage married couples to consult with their tax advisor before completing the SAVE plan application.

If you are a single filer, there is nothing to worry about; it’s just your income.

We also have to define the term discretionary income. Discretionary income usually means your total income minus all your living expenses like rent, groceries, utilities, etc. But that is not how it’s defined for purposes of the SAVE plan, which makes sense because everyone has different living expenses. For purposes of the 5% SAVE plan calculation, your discretionary income is the difference between your adjusted gross income (AGI) and 225% of the U.S. Department of Health and Human Services Poverty Guideline based on your family size.

For 2023, here are the Federal Poverty Levels based on family size:

Individuals: $14,580

Family of 2: $19,720

Family of 3: $24,860

Family of 4: $30,000

The list continues as the size of the family increases, and these amounts change each year. Let’s look at an easy example:

Sarah is a single tax filer

She has $80,000 in undergraduate federal student loans

Her adjusted gross income (AGI) is $40,000

Here is how her student loan payment would be calculated under the SAVE Plan.

Adjusted Gross Income: $40,000

Minus 225% of Individual Household Poverty Rate: $32,805 ($14,580 x 225%)

Equals: $7,195

Multiply by 5%: $359.75

So Sarah would only have to pay $359.75 for the YEAR (about $30 per month) toward her student loan under the new SAVE plan.

Some Borrowers Will Pay $0

No payments will be required under the SAVE plan for borrowers with an adjusted gross income below 225% of the Federal Poverty Level. In the example above, if Sarah’s AGI was only $30,000, since her $30,000 in income is below 225% of the Federal Poverty threshold of $32,805, she would not be required to make any monthly student loan payment under the SAVE plan until her income rises above the 225% threshold.

Size of the Household

As you can see above, it’s not just the annual income amount that determines how much a borrower will pay under the SAVE plan but also how many individuals there are within that person's household. More specifically, they ask for individuals who qualify as your “dependents.” If Sarah is a single filer with 2 roommates, she cannot claim those roommates as household members for the SAVE repayment plan. The SAVE application specifically asks for the following:

How many children, including unborn children, are in your family and receive more than half of their support from you?

How many other people, excluding your spouse and children, live with you and receive more than half of their support for you?

Studentaid.gov has the following illustration posted on their website to give borrowers a rough estimate of what the monthly payment student loan payment will be based on varying levels of income and family size:

The 5% Payment Will Take Effect July 2024

You will notice something odd in the illustration above. When I presented the example with Sarah, her AGI was $40,000 for a household of 1, which resulted in an estimated monthly payment of $30 but the chart above says $60 per month. Why? Under the current REPAYE plan which the SAVE plan is replacing, the payment amount is 10% of discretionary income. The lower 5% of discretionary income amount associated with the new SAVE plan is not expected to be phased in until July 2024. This means that borrowers who enroll in the SAVE plan now, while their payment may still be lower than that standard 10-year repayment plan, they will have to pay 10% of their discretionary income toward their student loans until they reach July 2024 when the new 5% rule becomes effective.

Going Into Effect in 2023

There are three components of the SAVE Plan that are going into effect in 2023, some of which we have yet to address in this article.

The larger income shield. Most of the current income-based student loan repayment plans only shield the borrower’s AGI up to 100% to 150% of the Federal Poverty Level compared to the new SAVE plan’s 225%. Under the SAVE plan, the 225% shield is in effect for 2023 reducing the amount of the borrower’s AGI subject to the current 10% repayment allowance. Also, more borrowers will be completely relieved of making payments when they restart in October because the income protection threshold is higher under the SAVE Plan.

The treatment of unpaid interest: We have not covered this yet but we will later on, the treatment of unpaid interest and the compounding of the interest for loans covered by the SAVE plan will be much more favorable for borrowers. This feature goes into effect in 2023.

Married Filing Separately: Married couples who choose to file their tax return married filing separately will no longer be required to include their spouse’s income in their monthly payment calculation under the SAVE plan.

Graduate Loans

The more favorable 5% income repayment amount that takes effect in July 2024 is only available for undergraduate loans under the SAVE plan. Individuals with graduate loans are eligible to enroll in the SAVE program but the minimum payment amount is based on 10% of discretionary income instead of 5%.

For borrowers that have both undergraduate and graduate student loans, they will take a weighted average between their undergraduate loans at 5% and graduate loans at 10% to reach the percent of discretionary income that will be required under the SAVE payment plan. Example: If you have $20,000 in undergraduate loans and $60,000 in graduate loans, you have $80,000 in student loans in total: 25% are undergraduate and 75% are graduate.

5% x 25% = 1.25%

10% x 75% = 7.50%

Average Weighted: 8.75%

This borrower would have to commit 8.75% of their discretionary income toward their SAVE student loan repayment plan.

SAVE Plan Loan Forgiveness

There is also a loan forgiveness component associated with the new SAVE Plan. Once you have made payments on your student loan for a specified number of years, any remaining balance is forgiven. The timeline to forgiveness under the SAVE plan can range from 10 years to 25 years. The original principal balance of your student loan or loans is what determines your forgiveness timeline.

Beginning in July 2024, borrowers who had original student loan balances of $12,000 or less, may be required to make monthly payments in accordance with the income-based payment plan, but after 10 years, any remaining loan balance is completely forgiven.

For each $1,000 in original student loan debt over the $12,000 threshold, they add one year to the borrower's forgiveness timeline up to the maximum of 20 years for undergraduate debt and 25 years for graduate debt. For example, Sue has a student loan with a current balance of $ 8,000 but the original principal balance of the loan was $14,000. Since Sue is $2,000 over the $12,000 threshold, her forgiveness timeline will be 12 years. If Sue continues to make income-based payments under the SAVE plan, any remaining balance after year 12 is completely forgiven.

Payments Made In The Past Count Toward Forgiveness

A big question for borrowers, for years that you had already made student loan payments, do those years count toward your SAVE plan forgiveness timeline? Good news, the answer is “Yes” and it gets better. You also receive credit for the specific periods of deferment and forbearance which will count toward the forgiveness timeline.

For example, Jeff graduated from college in 2017, he has an original loan balance of $20,000 and made payments on his student loans in 2017, 2018, 2019, and then did not make any student loan payments 2020 – 2023 due to the COVID relief. Jeff enrolls in the SAVE repayment plan. Since his original loan balance was $8,000 over the $12,000 10-year threshold, his timeline to forgiveness is 18 years. However, because Jeff started making student loan payments in 2017 and he also receives credit for the years of deferred payments under the COVID relief, he is credited with 7 years toward his 18-year forgiveness timeline. After Jeff has made another 11 years' worth of income-based student loan payments under the SAVE program, any remaining loan balance will be forgiven.

Forgiveness May Trigger A Taxable Event

If you are forgiven all or a portion of your student loan balance, you may have to pay taxes on the amount of the loan forgiveness. It states right on the SAVE plan application that “forgiveness may be taxable”. As of 2023, forgiven loan balances are a tax-free event but that rule sunsets in 2025. With the SAVE plans having a 10-year to 25-year forgiveness period, who knows what the tax rules will be when those remaining loan balances become eligible for forgiveness.

Borrowers Who Consolidate Multiple Loans

It’s not uncommon for college graduates to have 3 or more federal student loans outstanding at the same time because they will typically take multiple student loans over their college tenure and then at some point consolidate all of their loans together. When borrowers consolidate all of their loans into one under the SAVE plan, they receive a credit for a weighted average of payments that count toward forgiveness based upon the principal balance of loans being consolidated.

That’s the technical way of saying if you consolidate two of your student loans into one and the first loan that you consolidated began repayment 9 years ago and had a $1,000 original balance but then you consolidated it with a second loan with an original balance of $8,000 that you just started making payments on last year, if you qualify for 10-year forgiveness under the SAVE plan, the full loan balance will not be forgiven next year which would be the 10th year since you started making payments on the $1,000 loan. They are going to weigh the balance of each loan and how long you have been making payments on each loan to determine how much credit you receive toward your forgiveness timeline once enrolled in the SAVE plan.

Does Interest Accumulate In The SAVE Plan?

A concern will often arise with these income-based repayment plans that if your income is low enough and it does not require you to make a payment or if the payment is very small, does the interest on the student loan continue to accumulate which in turn continues to increase the amount that you own on your student loan?

Under the new SAVE plan, the answer is “No”. The SAVE plan cancels unpaid interest. For example, if under the SAVE plan your monthly payment is $150 but the monthly interest on your loan is $225, instead of the $75 being added to your loan balance, the $75 in unpaid interest is canceled by the Education Department. This new feature associated with the SAVE plan will prevent outstanding loan balances from ballooning due to unpaid compounding interest.

Loan Defaults and Delinquent Borrowers (Fresh Start Program)

The Department of Education is giving all student loan borrowers a fresh start under what is specifically called the Fresh Start Program. For all borrowers that either fell into default prior to the COVID payment pause or have delinquent student loan payments on their credit history, all student loan borrowers are allowed to enroll in the new Fresh Start program which brings everyone current regardless of what their student loan payment history was prior to the COVID payment pause.

But action needs to be taken prior to September 2024 to qualify for this Fresh Start. This does not happen automatically. I have been told that you will need to contact either the Education Department’s Default Resolution Group or your student loan service provider and ask to be enrolled in the Fresh Start Program. Once in the Fresh Start Program, the loan default and/or late payments are also permanently removed from your credit report.

How Do You Enroll In The SAVE Plan?

To enroll in the SAVE plan, you can visit the StudentAid.gov website. You will be able to apply for the SAVE program, get an estimate of what your monthly payment amount will be, and ask any questions that you have about the SAVE program. You can also call 1-800-433-3243. There is also a printable PDF of the SAVE application that you can download from the website.

SAVE is one of many “Income-Driven Repayment” (IDR) plans that are available to borrowers. Fortunately, on the first page of the SAVE application, you can check a box that says, “I want the income-driven repayment plan with the lowest monthly payment.” For many borrowers, this will be the new SAVE plan, but if one of the other IDR programs like IBR, PAYE, or ICR offers a lower monthly payment, you will be enrolled in that Income-Driven Repayment Plan.

The SAVE Plan Is Not For Everyone

While there are no income limitations that restrict borrowers from enrolling in the SAVE Plan, this plan will not be the right fit for everyone. It will take careful consideration on the part of each borrower to determine if they should enroll in the SAVE plan, continue with the standard 10-year repayment plan, or select a different Income-Driven Repayment option. Right on the SAVE application, it states that there is no cap on that amount of the monthly payment and “your payments may exceed what you would have paid under the 10-year standard repayment plan”.

Everyone’s situation will be different depending on your annual income amount, the size of your outstanding loan balance, the type of loans that you have, the size of your household, tax filing status, how long you have already been paying on your loans, and what you can afford to pay each month toward your student loans.

In general, for higher-income earners with small to medium-sized loan balances, the SAVE program may not make sense because the payments under the SAVE program are based solely on your income and household size rather than your loan balance.

The Monthly Payment Amounts Change Each Year

Since the SAVE Plan is an income-driven repayment plan, your required monthly payment amount can vary each year as your income level and household size change. If you were making $30,000 as a single filer in 2024, you might not be required to make any payments, but if you change jobs and begin earning $80,000 per year, your payments could increase dramatically under these Income-Driven Repayment plans.

In the past, these income-driven repayment plans have been a headache to maintain because you had to go through the manual process of recertifying your income each year, but there is good news on this front. The SAVE plan will give borrowers the option to give the Department of Education access to the IRS database to pull their income from their tax return automatically each year to avoid the manual process of recertifying their income each year. Section 5A of the SAVE application is titled “Authorization to Retrieve Federal Tax Information From the IRS”, so you can elect this when you enroll in the SAVE plan.

You Are Not Locked Into The SAVE Plan

Once you are enrolled in the SAVE plan, you are not locked into it. At any time, you may change to any other student loan repayment plan for which you are eligible, so if your circumstances change in the future, you could enroll in a different repayment option that better meets your financial situation.

Student Loan Repayment Strategy

As borrowers, it's very tempting to quickly select the student loan repayment program that offers the lowest monthly payment amount, but that may not be the best long-term financial solution. As I mentioned before, the standard repayment schedule for student loans is fixed payments over 10 years. With the SAFE plan potentially lowering the monthly payment amounts and stretching the loan out over a longer duration, borrowers could end up paying more over the life of that loan. In addition, for borrowers aiming for forgiveness, it isn’t easy to know what your income may be 5+ years from now.

While interest does not compound in the SAVE program, if your payments are only being applied toward the interest portion of your loans, the principal amount of the loan is not decreasing, which could cause you to pay more over that 20 to 25-year period than you would have just keeping the standard payment schedule a paying off your loan in 10 years. While forgiveness may be waiting for you after 20 years, it could trigger a taxable event, making the forgiveness target even less attractive.

The SAVE program is positive because it may give some borrowers much-needed relief as student loan payments restart and for borrowers just graduating from college. However, for borrowers who enroll in the SAVE program, it may make financial sense to ignore the forgiveness aspect of the program and pay more than just the minimum monthly payment to pay off the loans faster. Debt-free living is a wonderful thing.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Big FAFSA Calculation & Application Changes Starting in 2023

Parents that are used to completing the FAFSA application for their children are in for a few big surprises starting in 2023. Not only is the FAFSA application being completely revamped but the FAFSA calculation itself is being changed which could result in substantially lower financial aid awards for many college-bound students.

Parents that are used to completing the FAFSA application for their children are in for a few big surprises starting in 2023. Not only is the FAFSA application being completely revamped but the FAFSA calculation itself is being changed which could result in substantially lower financial aid awards for many college-bound students.

FAFSA Application Delayed Until December 1st

In 2023, the FAFSA application will not become available for completion until December 1st. Normally the FAFSA application becomes available for completion on October 1st of each year but due to the changes that are being made to the application, software updates, and staff training, they have delayed the release of the FAFSA application for the 2024 – 2025 school year to December 1, 2023. This will reduce the window to time that parents have to submit the FAFSA application in 2023 so advanced preparation is advised.

A Simplified FAFSA Application

Completing the FAFSA application can be a very frustrating process; tons of questions, unclear wording as to what information FAFSA is actually asking parents to report, and you have to spend a lot of time collecting all of your personal financial documents that are needed to enter the information on the FAFSA application.

Fortunately, in 2020, Congress passed the FAFSA Simplification Act which will greatly simplify the FAFSA application in 2023 and years going forward. The old FAFSA application contained 108 questions, the new FAFSA application is only expected to contain 36 questions. In addition to cutting the questions in half, the wording of many of the questions will be amended to make it easier to understand how to report your financial assets. Two very welcome changes to the application.

EFC (Expected Family Contribution) Calculation Removed

In the past, completing the FAFSA application has resulted in an Expected Family Contribution (EFC) amount which is meant to provide a ballpark amount that a family may have to pay out of pocket before need-based financial aid is awarded to a student. The term EFC can be misleading because it’s not necessarily the hard dollar amount that parents will be required to pay out of pocket but rather it’s the family’s financial need relative to other applicants.

To remove this confusion, EFC will now be replaced by SAI (Student Aid Index), so now after parents complete the FAFSA application, it will result in an SAI amount.

Financial Aid Awards Reduced For Multiple Children

Parents that have multiple children in college at the same time may be in for an unfortunate surprise when they see the results of the new SAI calculation. In the past, if a parent completed the FAFSA application and it resulted in an EFC of $30,000, but they had two children in college at the same time, FAFSA would split the $30,000 between the two children, $15,000 each, which would potentially make each student eligible for a higher financial aid award.

Starting the 2024 – 2025 school year, FAFSA will no longer be providing this EFC (SAI) split for multiple children in college. If the FAFSA calculation results in a $30,000 SAI, that $30,000 will now apply to EACH student, instead of being split equally between each child, which could result in lower need-based financial aid awards going forward.

Divorced Parents FAFSA Calculation Change

When parents are divorced, and they have a child attending college, the custodial parent is the parent that submits the FAFSA application based on their income and assets. Historically, the FAFSA definition of the “custodial parent” was the parent that the child lived with for the majority of the 12-month period ending on the day the FAFSA application is filed. This often times created a very favorable financial aid award if the child was living for a majority of the year with the parent that had lower income and assets.

In 2023, for the 2024 – 2025 school year and years going forward, this is changing. The new FAFSA rules require the parent who provided the most financial support in the “prior-prior” tax year to complete the FAFSA application instead of the custodial parent. Prior-prior refers to the tax year 2 years ago from the beginning of the college semester. For the 2024 – 2025 award year, FAFSA would be looking at the 2022 tax year for this determination.

For example, Joe and Sue got divorced 5 years ago, and their daughter Mary is currently a sophomore in college. Sue is a homemaker, Mary lives with her mother for the majority of the year, Joe makes $300,000 per year, and pays Sue $25,000 per year in child support and $40,000 per year in alimony. For the 2023 – 2024, under the old FAFSA calculation, Sue was considered the custodial parent, and completed the FAFSA form using her annual income and assets. Since Joe is not the custodial parent, Joe’s income and assets are ignored for purposes of FAFSA.

For the 2024 – 2025 school year, under the new rules, that would now change. Since Joe is providing a majority of the financial support via child support and alimony payments, Joe would now be the parent required to submit the FAFSA application based on his income and assets. Since Joe’s income is substantially higher than Sue’s, it could result in a much lower college financial aid award.

There has been some initial guidance, that if there is a “tie” as to which parent provided the majority of the financial support, the ties are broken based on whichever parent has the higher adjusted gross income.

Changes to Pell Grants

One of the largest sources of need-based financial aid from the federal government is awarded via Pell Grants. For the 2024 – 2025 school year, the maximum Pell Grant amount has been increased but they have changed how the Pell Grant is calculated. The Pell Grant takes into account both the SAI result (new EFC) and the applicant’s adjusted gross income. Since the calculation of the SAI has changed, for reasons that we have already discussed, it could impact the amount of the Pell Grants awarded to students.

As a new benefit, parents will now be able to determine if their child will be eligible for a Pell Grant award based on income and family size before they even complete the FAFSA form.

Grandparent 529 Penalty Removed

A positive change that they made was eliminating the restriction associated with distributing money from a 529 account owned by a grandparent for the benefit of the grandchild. Previously, if distributions were made from a grandparent owned 529 accounts, those distributions were considered “income of the student” in the FAFSA calculation, which could dramatically reduce the financial aid awards in future years. The new legislation removed this restriction and made grandparent owned 529 accounts even more valuable than they were prior to this change.

Income Protection Allowance Increased

The FAFSA calculation has income thresholds that exclude specific amounts of income of both the parents and the child in the calculation of the Student Aid Index. Those income exclusion allowances have been increased starting in the 2024 – 2025 school year. For example, the income allowance for students for the 2023 – 2024 school year was $7,040, meaning a student could earn up to $7,040 without their income factoring into the FAFSA calculation. For the 2024 – 2025 school year, the student income allowance will be $9,410.

The income protection allowance for parents will be increased by about 20%.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Top 10: Little-Known Facts About 529 College Savings Accounts

While 529 college savings accounts seem relatively straightforward, there are a number of little-known facts about these accounts that can be used for advanced wealth planning, tax strategy, and avoiding common pitfalls when taking distributions from these college savings accounts.

While 529 college savings accounts seem relatively straightforward, there are a number of little-known facts about these accounts that can be used for advanced wealth planning, tax strategy, and avoiding common pitfalls when taking distributions from these accounts.

1: Roth Transfers Will Be Allowed Starting in 2024

Starting in 2024, the IRS will allow direct transfers from 529 accounts to Roth IRAs. This is a fantastic new benefit that opens up a whole new basket of multi-generation wealth accumulation strategies for families.

2: Anyone Can Start A 529 Account For A Child

Do you have to be the parent of the child to open a 529 account? No. 529 account can be opened by parents, grandparents, aunts, or friends. Even if a parent has already established a 529 for their child there is no limit to the number of 529 accounts that can be opened for a single beneficiary.

3: State Tax Deduction For Contributions

There are currently 38 states that offer either state tax deductions or tax credits for contributions to 529 accounts. Here is the list. There are no federal tax deductions for contributions to 529 accounts. Also, you don’t have to be the parent of the child to receive the state tax benefits.

4: A Tax Deduction For Kids Already In College

For parents that already have kids in college, if you have not already established a 529 account and you are issuing checks for college tuition, for states that offer tax deductions for contributions, you may be able to open a 529 account, contribute to the account up to the state tax deduction limit, and as soon as the check clears, request a distribution to pay the college expenses. This allows you to capture the state tax deduction for the contributions to the account in that tax year.

5: Rollovers Count Toward State Tax Deduction

If you just moved to New York and have a 529 with another state, like Vermont, you are allowed to roll over the balance of the Vermont 529 account into a New York 529 account for the same beneficiary and those rollover amounts count toward the state tax deduction for that year. We had a New York client that had a Vermont 529 for their daughter with a $30,000 balance, and we had them rollover $10,000 per year over a 3-year period to capture the maximum NYS 529 state tax deduction of $10,000 each year.

6: Not All States Allow Distributions for K – 12 Tuition Expenses

In 2018, the federal government changes the tax laws allowing up to $10,000 to be distributed from a 529 account each year to pay for K – 12 tuition expenses. However, if you live in a state that has state income taxes, states are not required to adopt changes that are made at the federal level. There are a number of states, including New York, that do not recognize K – 12 tuition expenses as qualified expenses so the earnings portion of those withdrawals would be subject to state income tax and recapture of the tax deductions that were awarded for those contributions.

7: Transfers Between Beneficiaries

529 rules can vary state by state but most 529 accounts allow account owners to transfer all or a portion of balances between 529 account with different beneficiaries. This is common for families that have multiple children and a 529 account for each child. If the oldest child does not use their full 529 balance, all or a portion of their 529 account can be transferred the 529 accounts of their younger siblings.

8: Contributions Can Be Withdrawn Tax and Penalty Free

If you ever need to withdraw money from a 529 account that is not used for qualified college expenses, ONLY the earnings are subject to taxes and the 10% penalty. The contributions that you made to the account can always be withdrawn tax and penalty-free.

9: 529 Accounts May Reduce College Financial Aid

The balance in a 529 account that is owned by the parent of the student counts against the FAFSA calculation. Fortunately, assets of the parents only count 5.64% against the financial aid award, so if you have a $50,000 balance, it may only reduce the financial aid award by $2,820. However, 529 accounts owned by a grandparent or another relative, are invisible to the FAFSA calculation.

10: Maximum Balance Restrictions

529 plans do not have annual contribution limits but each state has “aggregate 529 plan limits”. These limits apply to the total 529 balances for any single 529 beneficiary in a particular state. Once the combined 529 plan balances for that beneficiary reach a state’s aggregate limit, no additional contributions can be made to any 529 plan administered by that state. Luckily, the limits for most states are very high. For example, the New York limit is $520,000 per beneficiary.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

529 to Roth IRA Transfers: A New Backdoor Roth Contribution Strategy Is Born

With the passing of the Secure Act 2.0, starting in 2024, owners of 529 accounts will now have the ability to transfer up to $35,000 from their 529 college savings account directly to a Roth IRA for the beneficiary of the account. While on the surface, this would just seem like a fantastic new option for parents that have money leftover in 529 accounts for their children, it is potentially much more than that. In creating this new rule, the IRS may have inadvertently opened up a new way for high-income earners to move up to $35,000 into a Roth IRA, creating a new “backdoor Roth IRA contribution” strategy for high-income earners and their family members.

With the passing of the Secure Act 2.0, starting in 2024, owners of 529 accounts will now have the ability to transfer up to $35,000 from their 529 college savings account directly to a Roth IRA for the beneficiary of the account. While on the surface, this would just seem like a fantastic new option for parents that have money leftover in 529 accounts for their children, it is potentially much more than that. In creating this new rule, the IRS may have inadvertently opened up a new way for high-income earners to move up to $35,000 into a Roth IRA, creating a new “backdoor Roth IRA contribution” strategy for high-income earners and their family members.

Money Remaining In the 529 Account for Your Children

I will start by explaining this new 529 to Roth IRA transfer provision using the scenario that it was probably intended for; a parent that owns a 529 account for their children, the kids are done with college, and there is still a balance remaining in the 529 account.

The ability to shift money from a 529 account directly to a Roth IRA for your child is a fantastic new distribution option for balances that may be leftover in these accounts after your child or grandchild has completed college. Prior to the passage of the Secure Act 2.0, there were only two options for balances remaining in 529 accounts:

Change the beneficiary on the account to someone else

Process a non-qualified distribution from the account

Both options created potential challenges for the owners of 529 accounts. For the “change the beneficiary option”, what if you only have one child, or what if the remaining balance is in the youngest child’s account? There may not be anyone else to change the beneficiary to.

The second option, processing a “non-qualified distribution” from the 529 account, if there were investment earnings in the account, those investment earnings are subject to taxes and a 10% penalty because they were not used to pay a qualified education expense.

The “Roth Transfer Option” not only gives account owners a third attractive option, but it’s so attractive that planners may begin advising clients to purposefully overfund these 529 accounts with the intention of processing these Roth transfers after the child has completed college.

Requirements for 529 to Roth IRA Transfers

Before I get into explaining the advanced tax and wealth accumulation strategies associated with this new 529 distribution option, like any new tax law, there is a list of rules that you have to follow to be eligible to process these 529 to Roth IRA transfers.

The 15 Year Rule

The first requirement is the 529 account must have been in existence for at least 15 years to be eligible to execute a Roth transfer from the account. The clock starts when you deposit the first dollar into that 529 account. The planning tip here is to fund the 529 as soon as you can after the child is born, if you do, the 529 account will be eligible for Roth IRA transfers by their 15th or 16th birthday.

There is an unanswered question surrounding rollovers between state plans and this 15-year rule. Right now, you are allowed to rollover let’s say a Virginia 529 account into a New York 529 account. The question becomes, since the New York 529 account is a new account, would that end up re-setting the 15-year inception clock?

Contributions Within The Last 5 Years Are Not Eligible

When you go to process a Roth transfer from a 529 account, contributions made to the 529 account within the previous 5 years are not eligible for Roth transfers.

The Beneficiary of the 529 Account and the Owners of the Roth IRA Must Be The Same Person

A third requirement is the beneficiary listed on the 529 account and the owner of the Roth IRA account must be the same person. If your daughter is the beneficiary of the 529 account, she would also need to be the owner of the Roth IRA that is receiving the transfer directly from the 529 account. There is a big question surrounding this requirement that we still need clarification on from the IRS. The question is this: Is the account owner allowed to change the beneficiary on the 529 account without having to re-satisfy a new 15-year account inception requirement?

If they allow beneficiary changes without a new 15-year inception period, with 529 accounts, the account owner can change the beneficiary on these accounts to whomever they want……..including themselves. This would allow a parent to change the beneficiary to themselves on the 529 account and then transfer the balance to their own Roth IRA, which may not be the intent of the new law. We will have to wait for guidance on this.

No Roth IRA Income Limitations

As many people are aware, if you make too much, you are not allowed to contribute to a Roth IRA. For 2023, the ability to make Roth IRA contributions begins to phase out at the following income levels:

Single Filer: $138,000

Married Filer: $218,000

These transfers directly from 529 accounts to the beneficiary’s Roth IRA do not carry the income limitation, so regardless of the income level of the 529 account owner or the beneficiary, there a no maximum income limit that would preclude these 529 to Roth IRA transfers from taking place.

The IRA Owner Must Have Earned Income

With exception of the Roth IRA income phaseout rules, the rest of the Roth RIA rules still apply when determining whether or not a 529 to Roth IRA transfer is allowed in a given tax year. First, the beneficiary of the 529 (also the owner of the Roth IRA) needs to have earned income in the year that the transfer takes place to be eligible to process a transfer from the 529 to their Roth IRA.

Annual 529 to Roth IRA Transfer Limits

The amount that can be transferred from the 529 to the Roth IRA is also limited each year by the regular Roth IRA annual contribution limits. For 2023, an individual under the age of 50, is allowed to make a Roth IRA contribution of up to $6,500. That is the most that can be moved from the 529 account to Roth IRA in a single tax year. But in addition to this hard dollar limit, you have to also take into account any other Roth IRA contributions that were made to the IRA owner’s account and the IRA owners earned income for that tax year.

The annual contribution limit to a Roth IRA for 2023 is actually the LESSER of:

$6,500; or

100% of the earned income of the account owner

Assuming the IRA contribution limits stay the same in 2024, if a child only has $3,000 in income, the maximum amount that could be transferred from the 529 to the Roth IRA in 2024 is $3,000.

If the child made a contribution of their own to the Roth IRA, that would also count against the amount that is available for the 529 to Roth IRA transfer. For example, the child makes $10,000 in earned income, making them eligible for the full $6,500 Roth IRA contribution, but if the child contributes $2,000 to their Roth IRA throughout the year, the maximum 529 to Roth IRA transfer would be $4,500 ($6,500 - $2,000 = $4,500)

The IRA limits could be the same or potentially higher in 2024 when this 529 to Roth IRA transfer option goes into effect.

$35,000 Limiting Maximum Per Beneficiary

The maximum lifetime amount that can be transferred from a 529 to a Roth IRA is $35,000 for each beneficiary. Given the annual contribution limits that we just covered, you would not be allowed to just transfer $35,000 from the 529 to the Roth IRA all in one shot. The $35,000 lifetime limit would be reached after making multiple years of transfers from the 529 to the Roth IRA over a number of tax years.

Advanced 529 Planning Strategies Using Roth Transfers

Now I’m going to cover some of the advanced tax and wealth accumulation strategies that may be able to be executed under this 529 Roth Transfer provision. Disclosure, writing this in February 2023, we are still waiting on guidance from the IRS on what they may or may not have intended with this new 529 to Roth transfer option that becomes available starting in 2024, so their guidance could either reinforce that these strategies can be used or limit the use of these advanced strategies. Time will tell.

Super Funding A Roth IRA For Your Child

While 529 accounts have traditionally been used to save exclusively for future college expenses for your children or grandchild, they just become much more than that. Parents and grandparents can now fund these accounts when a child is young with the pure intention of NOT using the funds for college but rather creating a supercharged Roth IRA as soon as that child begins earning income in their teenage years and into their 20s.

This is best illustrated in an example. You have a granddaughter that is born in 2023, you open a 529 account for her and fund it with $15,000. By the time your granddaughter has reached age 18, let’s assume through wise investment decisions, the account has tripled to $45,000. Between ages 18 and 21, she works a summer job making $8,000 in earned income each year and then gets a job after graduating college making $80,000 per year. Assuming she made no contributions to a Roth IRA over the years, you would be able to make transfers between her 529 account and her Roth IRA up to the annual contribution limit until the total transfers reached the $35,000 lifetime maximum.

If that $35,000 lifetime maximum is reached when she turns age 24, assuming she also makes wise investment decisions and earns 8% per year on her Roth IRA until she reaches age 60, at age 60 she would have $620,000 in that Roth IRA account that could be withdrawal ALL TAX-FREE.

Now multiply that $620,000 across EACH of your children or grandchildren, and it becomes a truly fantastic way to build tax-free wealth for the next generation.

529 Backdoor Roth Contribution Strategy

A fun fact, there are no age limits on either the owner or beneficiary of a 529 account. At the age of 40, I could open a 529 account, be the owner and the beneficiary of the account, fund the account with $15,000, wait the 15 years, and then when I turn age 55, begin processing transfers directly from the 529 to my Roth IRA up to the maximum annual IRA limit each year until I reach my $35,000 lifetime limit.

I really don’t care that the money has to sit in the 529 for 15 years because 529 accumulate tax deferred anyways, and by the time I hit age 59.5, making me eligible for tax-free withdrawal of the earnings, I will have already moved most of the balance over to my Roth IRA. Oh and remember, even if you make too much to contribute directly to a Roth IRA, the income limits do not apply to these 529 to Roth IRA direct transfers.

The IRS may have inadvertently created a new “Backdoor Roth IRA Contribution” strategy for high-income earners.

Now there may be some limitations that can come into play with the age of the individual executing this strategy, it’s really less about their age, and more about whether or not they will have earned income 15 years from now when the 529 to Roth IRA transfer window opens. If you are 65, fund a 529, and then at age 80 want to begin these 529 to Roth IRA transfers, if you have no earned income, you can process these 529 to Roth IRA transfers because you are limited by the regular IRA annual contribution limits that require you to have earned income to process the transfers.

Advantage Over Traditional Backdoor Roth Conversions

For individuals that have a solid understanding of how the traditional “Backdoor Roth IRA Contribution” strategy works, the new 529 to Roth IRA transfer strategy potentially contains additional advantages over and above the traditional backdoor Roth strategy. These movements from the 529 to Roth IRA are not considered “conversions”, they are considered direct transfers. Why is that important? Under the traditional Backdoor Roth Contribution strategy the taxpayer is making a non-deductible contribution to a traditional IRA and then processes a conversion to a Roth IRA.

One of the IRS rules during this conversion process is the “aggregation rule”. When a Roth conversion is processed, the taxpayer has to aggregate all of their pre-tax IRA balance together in determining how much of the conversion is taxable, so if the taxpayer has other pre-tax IRAs, it came sometimes derail the backdoor Roth contribution strategy. If they instead use the 529 to Roth IRA direct transfer processes, since as of right now it is not technically a “conversion”, the aggregate rule is avoided.

The second big advantage is with the 529 to Roth IRA transfer strategy, the Roth IRA is potentially being funded with “untaxed earnings” as opposed to after-tax dollar. Again, in the traditional Backdoor Roth Strategy, the taxpayer is using after-tax money to make a nondeductible contribution to a Traditional IRA and then converting those dollars to a Roth IRA. If instead the taxpayer funds a 529 with $15,000 in after-tax dollars, but during the 15-year holding, The account grows the $35,000, they are then able to begin direct transfers from the 529 to the Roth IRA when $20,000 of that account balance represents earnings that were never taxed. Pretty cool!!

State Tax Deduction Clawbacks?

There are some states, like New York, that offer tax deductions for contributions to 529 accounts up to annual limits. When the federal government changes the rules for 529 accounts, the states do not always follow suit. For example, when the federal government changed the tax laws allowing account owners to distribute up to $10,000 per year for K – 12 qualified expenses from 529 accounts, some states, like New York, did not follow suit, and did not recognize the new “qualified expenses”. Thus, if someone in New York distributed $10,000 from a 529 for K – 12 expenses, while they would not have to pay federal tax on the distribution, New York viewed it as a “non-qualified distribution”, not only making the earnings subject to state taxes but also requiring a clawback of any state tax deduction that was taken on the contribution amounts.

The question becomes will the states recognize these 529 to Roth IRA transfers as “qualified distributions,” or will they be subject to taxes and deduction clawbacks at the state level? Time will tell.

Waiting for Guidance From The IRS

This new 529 to Roth IRA transfer option that starts in 2024 has the potential to be a tremendous tax-free wealth accumulation strategy for not just children but for individuals of all ages. However, as I mentioned multiple times in the article, we have to wait for formal guidance from the IRS to determine which of these advanced wealth accumulation strategies will be allowed from tax years 2024 and beyond.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Grandparent Owned 529 Accounts Just Got Better

A 529 account owned by a grandparent is often considered one of the most effective ways to save for college for a grandchild. But in 2023, the rules are changing………

Grandparent Owned 529 Accounts Just Got Better

A 529 account owned by a grandparent is often considered one of the most effective ways to save for college for a student. Mainly because 529 accounts owned by the grandparents are invisible to the college financial aid calculation (FAFSA) when determining the financial aid package that will be awarded to a student. But there is a little-known pitfall about distributions from grandparent owned 529 accounts and the rules are changing in 2023. In this article, we will review:

Advantages of grandparent owned 529 accounts

The FAFSA pitfall of distributions from grandparent owned 529 accounts

The FAFSA two-year lookback period

The change to the 529 rules starting in 2023

Tax deductions for contributions to 529 accounts

What if your grandchild does not go to college?

Paying K – 12 expenses with a 529 account

Pitfall of Grandparent Owned 529 Accounts

Historically, there has been a major issue when grandparents begin distributing money out of these 529 accounts to pay college expenses for their grandchildren which can hurt their financial aid eligibility. While these accounts are invisible to the FAFSA calculation as an asset, in the year that the distribution takes place from a grandparent owned 529 account, those distributions now count as “income of the student” in the year that the distribution takes place. Income of the student counts heavily against the need-based financial aid award. Currently, any income of the student above the $7,040 threshold counts 50% against the financial aid award.

For example, if a grandparent distributes $30,000 from the 529 account to pay college expenses for the grandchild, in that determination year, assuming the child has no other income, that distribution could reduce the financial aid award two years later by $11,480.

FAFSA Two-Year Lookback

FAFSA has a two-year lookback for purposes of determining income in the EFC calculation (expected family contribution), so the family doesn’t realize the misstep until two years later. For example, if the distribution takes place in the fall of the student’s freshman year, the financial aid package would not be reduced until the fall of their junior year.

Since we are aware of this income two-year lookback rule, the workaround has been to advise grandparents not to distribute money from the 529 accounts until the spring of their sophomore year. If the child graduates in four years by the time they are submitting the FAFSA application for their senior year, that determination year that 529 distribution took place is no longer in play.

Quick Note: All of this only matters if the student qualifies for need-based financial aid. If the student, through their parent’s FAFSA application, does not qualify for any need-based financial aid, then the impact of these distributions from the grandparent owned 529 accounts is irrelevant because they were not receiving any financial aid anyways.

New Rules Starting in 2023

But the rules are changing starting in 2023 to make these grandparent owned 529 accounts even more advantageous. Under the new rules, distribution from grandparent owned 529 account will no longer count as income of the student. These 529 accounts owned by the grandparents are now completely invisible to the FAFSA calculation for both assets and income, which makes them even more valuable.

Tax Deduction For 529 Contributions

There can also be tax benefits for grandparents contributing to 529 accounts for their grandkids. Certain states allow state income tax deductions for contributions up to a certain thresholds. In New York State, there is a $5,000 state tax deduction for single filers and a $10,000 deduction for joint filers each tax year. The amounts vary from state to state and some states have no deduction, so you have to do your homework.

What If The Grandchild Does Not Go To College?

What happens if you fund this 529 account for your grandchild but then they decide not to go to college? There are a few options here. The grandparent can change the beneficiary of the account to another grandchild or family member. The second option, you can just take a distribution of the account balance. If the balance is distributed but it’s not used for college expenses, the contribution amounts are returned tax and penalty-free but the earnings portion of the account is subject to ordinary income taxes and a 10% penalty since it wasn’t used for qualified college expenses.

K - 12 Qualified Expenses

The federal government made changes to the tax rules in 2017 which also allow up to $10,000 per year to be distributed from 529 accounts for K - 12 expenses. If you have grandchildren that are attending a private k -12 school, this is another way for grandparents to potentially capture a tax deduction, and help pay those expenses.

However, and this is very important, while the federal government recognizes the K – 12 $10,000 per year as a qualified distribution, the states which sponsor these 529 plans may not adhere to those same rules. In fact, in New York State, not only does New York not recognize K – 12 expenses as “qualified expenses” for purposes of distributions from a 529 account, but these nonqualified withdrawals also require a recapture of any New York State tax benefits that have accrued on the contributions. Double ouch!! These rules vary state by state so you have to do your homework before paying K – 12 expenses out of a 529 account.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Potential investors of 529 plans may get more favorable tax benefits from 529 plans sponsored by their own state. Consult your tax professional for how 529 tax treatments and account fees would apply to your particular situation. To determine which college saving option is right for you, please consult your tax and accounting advisors. Neither APFS nor its affiliates or financial professionals provide tax, legal or accounting advice. Please carefully consider investment objectives, risks, charges, and expenses before investing. For this and other information about municipal fund securities, please obtain an offering statement and read it carefully before you invest. Investments in 529 college savings plans are neither FDIC insured nor guaranteed and may lose value.

College Savings Account Options

There are a lot of different types of accounts that you can use to save for college. But, certain accounts have advantages over others such as:

· Tax deductions for contributions

· Tax free accumulation and withdrawal

· The impact on college financial aid

· Who has control over the account

· Accumulation rate

The types of college savings account that I will be covering in this article are:

· 529 accounts

· Coverdell accounts (also know as ESA’s)

· UTMA / UGMA accounts

· Brokerage Accounts

· Savings Accounts

To make it easy to compare and contrast each option, I will have a grading table at the beginning of each section that will provide you with some general information on each type of account, as well as my overall grade on the effectiveness of each college saving option.

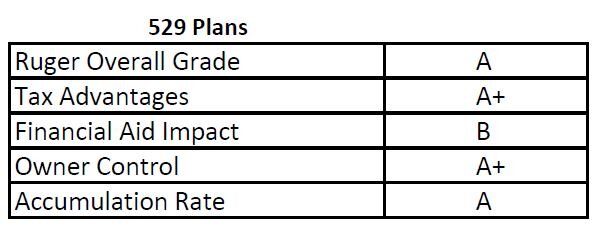

529 Plans

I’ll start with my favorite which are 529 College Savings Plan accounts. As a Financial Planner, I tend to favor 529 accounts as primary college savings vehicles due to the tax advantages associated with them. Many states offer state income tax deductions for contributions up to specific dollar amounts, so there is an immediate tax benefit. For example, New York provides a state tax deduction for up to $5,000 for single filers, and $10,000 for joint filers for contributions to NYS 529 accounts year. There is no income limitation for contributing to these accounts.

NOTE: Every now and then I come across individuals that have 529 accounts outside of their home state and they could be missing out on state tax deductions.

However, the bigger tax benefit is that fact that all of the investment returns generated by these accounts can be withdrawn tax free, as long as they are used for a qualified college expense. For example, if you deposit $5K into a 529 account when your child is 2 years old, and it grows to $15,000 by the time they go to college, and you use the account to pay qualified expenses, you do not pay tax on any of the $15,000 that is withdrawn. That is huge!! With many of the other college savings options like UTMA or brokerage accounts, you have to pay tax on the gains.

There is also a control advantage, in that the parent, grandparent, or whoever establishes the accounts has full control as to when and how much is distributed from the account. This is unlike UTMA / UGMA accounts, where once the child reaches a certain age, the child can do whatever they want with the account without the account owner’s consent.

A 529 account does count against the financial aid calculation, but it is a minimal impact in most cases. Since these accounts are typically owned by the parents, in the FAFSA formula, 5.6% of the balance would count against the financial aid reward. So, if you have a $50,000 balance in a 529 account, it would only set you back $2,800 per year in financial aid.

I gave these account an “A” for an accumulation rating because they have a lot of investment option available, and account owners can be as aggressive or conservative as they would like with these accounts. Many states also offer “age based portfolios” where the account is allocated based on the age of the child, and when the will turn 18. These portfolios automatically become more conservative as they get closer to the college start date.

The contributions limits to these accounts are also very high. Lifetime contributions can total $400,000 or more (depending on your state) per beneficiary.

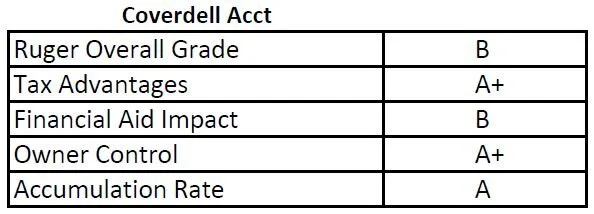

Coverdell Accounts (Education Savings Accounts)

Coverdell accounts have some of the benefits associated with 529 accounts, but there are contribution and income restrictions associated with these types of accounts. First, as of 2021, only taxpayers with adjusted gross income below $110,000 for single filers and $220,000 for joint filers are eligible to contribute to Coverdell accounts.

The other main limiting factor is the contribution limits. You are limited to a $2,000 maximum contribution each year until the beneficiary’s 18th birthday. Given the rising cost of college, it is difficult to accumulate enough in these accounts to reach the college savings goals for many families. Similar to 529 accounts, these accounts are counted as an asset of the parents for purposes of financial aid.

The one advantage these accounts have over 529 accounts is that the balance can be used without limitations for qualified expenses to an elementary or secondary public, private, or religious school. The federal rules recently changed for 529 accounts allowing these types of qualified withdrawal, but they are limited to $10,000 and depending on the state you live in, the state may not recognize these as qualified withdrawals from a 529 account.

If there is money left over in these Coverdell account, they also have to be liquidated by the time the beneficiary of the account turns age 30. 529 accounts do not have this restriction.

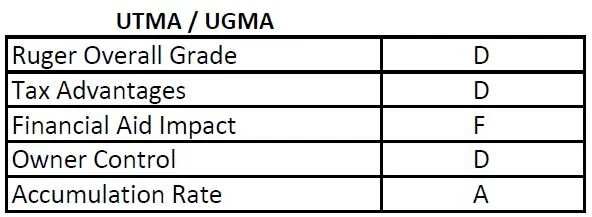

UTMA & UGMA Accounts

UGMA & UTMA accounts get the lowest overall grade from me. With these accounts, the child is technically the owner of the account. While the child is a minor, the parent is often assigned as the custodian of the account. But once the child reaches legal age, which can be 18, 19, or 21, depending on the state you live in, the child is then awarded full control over the account. This can be a problem when your child decides at age 18 that buying a Porsche is a better idea than spending that money on college tuition.

Also, because these accounts are technically owned by the child, they are a wrecking ball for the financial aid calculation. As I mentioned before, when it is an asset of the parent, 5.6% of the balance counts against financial aid, but when it is an asset of the child, 20% of the account balance counts against financial aid.

There are no special tax benefits associated with UTMA and UGMA accounts. No tax deductions for contributions and the child pays taxes on the gains.

Unlike 529 and Coverdell accounts, where you can change the beneficiary list on the account, with UTMA and UGMA accounts, the beneficiary named on the account cannot be changed.

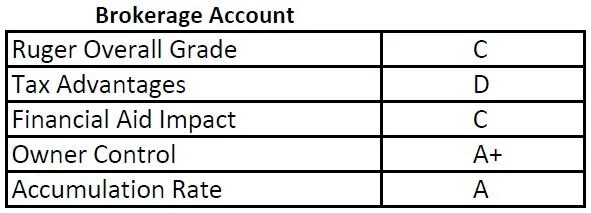

Brokerage Accounts

Parents can use brokerage accounts to accumulate money for college instead of the cash sitting in their checking account earning 0.25% per year. The disadvantage is the parents have to pay tax on all of the investment gains in the account once they liquidate them to pay for college. If the parents are in a higher tax bracket, they could lose up to 40%+ of those gains to taxes versus the 529 accounts where no taxes are paid on the appreciation. But, it also has the double whammy that if the parents realize capital gains from the liquidation, their income will be higher in the FAFSA calculation two years from now.

Sometimes, a brokerage account can complement a 529 account as part of a comprehensive college savings strategy. Many parents do not want to risk “over funding” a 529 account, so once the 529 accounts have hit a comfortable level, they will begin contributing the rest of the college savings to a brokerage account to maintain flexibility.

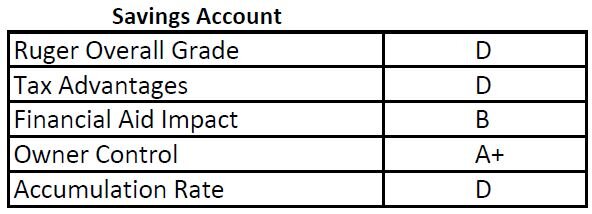

Savings Accounts

The pros and cons of a savings account owned by the parent or guardian of the child will have similar pros and cons of a brokerage account with one big drawback. Last I checked, most savings accounts were earning under 1% in interest. The cost of college since 1982 has increased by 6% per year (JP Morgan College Planning Essentials 2021). If the cost of college is going up by 6% per year, and your savings is only earning 1% per year, even though the balance in your savings account did not drop, you are losing ground to the tune of 5% PER YEAR. By having your college savings accounts invested in a 529, Coverdell, or brokerage account, it will at least provide you with the opportunity to keep pace with or exceed the inflation rate of college costs.

Can The Cost of College Keep Rising?

Let’s say the cost of attending college keeps rising at 6% per year, and you have a 2-year-old child that you want to send to state school which may cost $25,000 per year today. By the time they turn 18, it would cost $67,000 PER YEAR, times 4 years of college, which is $268,000 for a bachelor’s degree! The response I usually get when people hear these number is “there is no way that they can allow that to happen!!”. People were saying that 10 years ago, and guess what? It happened. This is what makes having a solid college savings strategy so important for your overall financial plan.

NOTE: As Financial Planners, we are seeing a lot more retirees carry mortgages and HELOC’s into retirement and the reason is usually “I helped the kids pay for college”.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Understanding FAFSA & How To Qualify For More College Financial Aid

As the cost of college continues to rise, so does the financial stress that it puts on families trying to determine the optimal solution to pay for college. It’s never been more important for parents and family members of these students

As the cost of college continues to rise, so does the financial stress that it puts on families trying to determine the optimal solution to pay for college. It’s never been more important for parents and family members of these students to understand:

How is college financial aid calculated?

Are there ways to increase the amount of financial aid you can receive?

What are the income and asset thresholds where financial aid evaporates?

Understanding the FAFSA 2 Year Lookback Rule

The difference between financial aid at public colleges vs private colleges

In this article we will provide you with guidance on these topics as well as introduce strategies that we as financial planners use with our clients to help them qualify for more financial aid.

How is college financial aid calculated?

Too often we see families jump to the incorrect assumption that “I make too much to qualify for financial aid.” Depending on what your asset and income picture looks like there may be strategies that will allow you to shift assets around during the financial aid determination years to qualify for need based financial aid. But you first need to understand how need based financial aid is calculated.

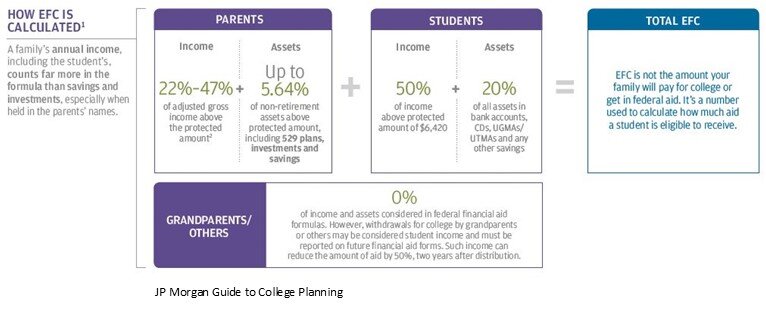

The Department of Education has a formula to calculate your “Expected Family Contribution” (EFC). The Expected Family Contribution is the amount that a family is expected to pay out of pocket each year before financial aid is awarded. Here is the general formula for financial aid:

It’s pretty simple and straight forward. Cost of the college, minus the EFC, equals the amount of your financial aid award. Now let’s breakdown how the EFC is calculated

Expected Family Contribution (EFC) Calculation

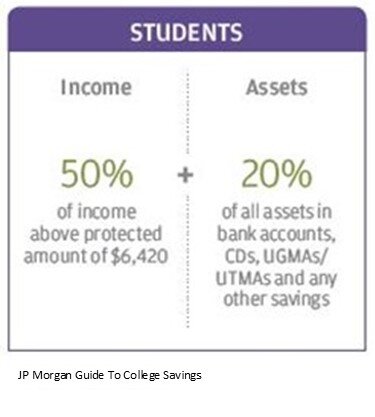

Both the parent’s income and assets, as well as the student’s income and assets come into play when calculating a family’s EFC. But they are weighted differently in the formula. Let’s look at the parent’s income and assets first.

Parent’s Income & Assets

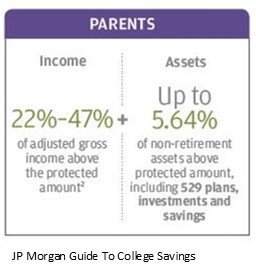

Parents Income: The parent’s income is one of the largest factors in the EFC calculation. The percentage of the parents income that counts toward the EFC calculation is expressed as a range between 22% - 47% because it depends on a number of factors such as household size and the number of children that you have attending college at the same time.

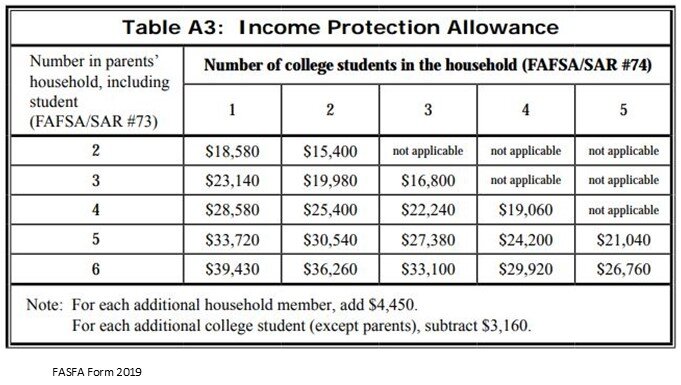

However, there is an “Income Protection Allowance” that allows parents to shelter a portion of their income from the formula based on the household size and the number of children attending college. See that chart below for the 2019-2020 FAFSA form:

Parents Assets: Any assets owned by the parents of the student are multiplied by 5.64% and that amount counts towards the EFC. Here are a few assets that are specifically EXCLUDED from this calculation:

Retirement Accounts: 401(k), 403(b), IRA’s, SEP, Simple

Pensions

Primary Residence

Family controlled business (less than 100 employees and 51%+ ownership by parents)

On the opposite side of that coin, here is a list of some assets that are specifically INCLUDED in the calculation:

Balance in 529 accounts

Real estate other than the primary residence

Even if held in an LLC – Reported separately from “business assets”

Non-retirement investment accounts, savings account, CD’s

Trusts where the student is a beneficiary of the trust (even if not entitled to distributions yet)

Business interest (less than 51% family owned by parents or more than 100 employees)

Similar to the Income Allowance Table, there is also a Parents’ Asset Protection Allowance Table that allows them to shelter a portion of their countable assets from the EFC formula. See the table below for the 2019-2020 school year.

Student’s Income & Assets

Now let’s switch gears over to the student side of the EFC formula. The income and the assets of the student are weighted differently than the parent’s income and assets. Here is the student side of the EFC formula:

As you can clearly see, income and assets in the student’s name compared to the parent name will dramatically increase the Expected Family Contribution and in turn decrease the amount of financial aid awarded. It is because of this, that as a general rule, if you think your asset and income picture may qualify you for financial aid, do not put assets in the name of your child. The most common error that we see people make are assets in an UGMA or UTMA account. Even though parents control those accounts, they are technically considered an asset of the child. If there is $30,000 sitting in an UTMA account for the student, they are automatically losing around $6,000 EACH YEAR in financial aid. Multiply that by 4 years of college, it ends up costing the family $24,000 out of pocket that otherwise could have been covered by financial aid.

EFC Formula Illustration

If we put all of the pieces together, here is an illustration of the full EFC Formula:

Grandparent Owned 529 Plans For The Student

As you will see in the EFC formula above, assets owned by the grandparents with the student listed as the beneficiary, like 529 accounts, are not counted at all toward the EFC calculation. This can be a very valuable college savings strategy for families since the parent owned 529 accounts count toward the Expected Family Contribution. However, there are some pitfalls and common mistakes that we have seen people make with regard to grandparent owned 529 accounts. See the article below for more information specific to this topic:

Article: Common Mistakes With Grandparent Owned 529 Accounts

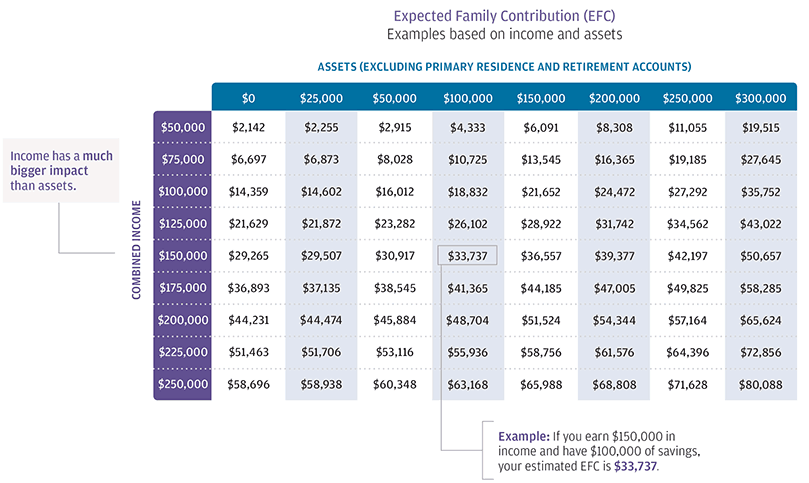

Financial Aid Chart

Our friends over at JP Morgan were kind enough to put a summary chart together for this EFC calculation which allows families to get a ballpark idea of what their Expected Family Contribution might be without getting out a calculator. The chart below is based on the following assumptions:

Two parent household

2 Children: One attending college and the other still at home

The child attending college has no assets or income

The oldest parent is age 49

Using the chart above, if the parents combined income is $150,000 and they have $100,000 in countable assets, the Expected Family Contribution would be $33,737 for that school year. What does that mean? If the student is attending a state college and the tuition with room and board is $26,000, since the EFC is greater than the total cost of college for that year, that family would receive no financial aid. However, if that student applies to a private school and the CSS Profile form results in approximately that same EFC of $33,737 but the private school costs $60,000 per year, then the family may receive need based financial aid or a grant from the private school equaling $26,263 per year.

Public Colleges vs. Private Colleges

It’s important to point out that FAFSA and the EFC calculation primarily applies to students that plan on attending a Community College, State College, or certain Private Colleges. Since Private Colleges do not receive federal financial aid they do not have to adhere to the EFC calculation that is used by FAFSA. Private college can choose to use to FAFSA criteria but many of the private colleges will require students to complete both the FAFSA form and the CSS Profile Form.

Here are a few examples of how the financial reporting deviates:

If the parents have a 100% family owned business, they would not have to list that as an asset on the FAFSA application but they would have to list the business as an assets on the CSS Profile form.

The equity in your primary residence is not counted as an asset for FAFSA but it is listed as an asset on the CSS Profile Form.

For parents that are divorced. FAFSA only looks at the assets and income of the custodial parent. The CSS Profile Form captures the assets and income of both the custodial and non-custodial parent.

Because of the deviations between the FAFSA application and the CSS Profile Form, we have seen situations where a student received no need based financial aid when applying to a $50,000 per year private school but they received financial aid for attending a state school even though the annual cost to attend the state school was half the cost of the private school.

Top 10 Ways To Increase College Financial Aid

Here is a quick list of the top strategies that we use to help families to qualify for more financial aid.

Disclosure: There are details associated with each strategy listed below that need to be executed correctly in order for the strategy to have a positive impact on the EFC calculation. Not all strategies will work depending on the financial circumstances of each household and where the child plans to attend college. Contact us for details.

Get assets out of the name of the student

Grandparent owned 529 accounts

Use countable assets of the parents to pay down debt

Move UTGMA & UGMA accounts to 529 UGMA or 529 UTMA accounts

Increase contributions to retirement accounts

Minimize distributions from retirement accounts

Minimize capital gain and dividend income

Accelerate necessary expenses

Use home equity line of credit instead of home equity loan

Families that own small businesses have a lot of advanced planning options

FAFSA – 2 Year Lookback

It’s important to understand the FAFSA application process because you have know when they take the snapshot of your income and assets for the EFC calculation in order to have a shot at increasing the financial aid that you may be able to qualify for.

FAFSA looks back 2 years to determine what your income will be for the upcoming school year. For example, if your child is going to be a freshman in college in the fall of 2020, you will report your 2018 income on the FAFSA application. This is important because you have to start putting some of these strategies into place in the spring of your child’s sophomore year in high school otherwise you could miss out on planning opportunities for their freshman year in college.

If your child is already a junior or senior in high school and you are just reading this article now, there is still an opportunity to implement some of the strategies listed above. Income has a 2 year lookback but assets are reported as of the day of the application. Also the FAFSA application is completed each year that your child is attending college, so even though you may have missed income reduction strategies for their freshman year, at some point the 2 year lookback will influence the financial aid picture during the four years of their undergraduate degree.

IMPORTANT NOTE: Income has a 2-year lookback