Social Security Will Only Increase by 2.5% In 2025

The Social Security Administration recently announced that the cost-of-living adjustment (COLA) for 2025 will only be 2.5% for 2025. That is a much lower COLA increase than we have seen in the past few years, with a COLA increase of 3.2% in 2024 and an increase of 8.7% in 2023. According to the Social Security Administration, the 2.5% increase in 2025 will result, on average, in a $50 per month increase to social security recipients.

The Social Security Administration recently announced that the cost-of-living adjustment (COLA) for 2025 will only be a 2.5% increase. This is significantly lower than the COLA increases in the past few years, which included a 3.2% increase in 2024 and a notable 8.7% increase in 2023. According to the Social Security Administration, the 2.5% increase in 2025 will result in an average $50 per month increase for Social Security recipients.

Immediately after the announcement, many retirees expressed concerns that a modest 2.5% increase is not sufficient to keep pace with the rising costs they face for groceries, insurance, rent, and other everyday expenses.

Medicare Premiums May Increase by More Than 2.5%

While the Medicare Part B and Part D premium amounts for 2025 have yet to be released, consensus expects increases greater than 3% for both Part B and Part D. If this holds true, retirees may gain an average of $50 per month from the COLA increase in their Social Security benefits, but a substantial portion of that could be offset by higher Medicare premiums, which are deducted directly from their monthly Social Security payments.

In 2024, the COLA increase for Social Security was 3.2%, but Medicare Part B premiums rose by 5.9%, leaving many retirees already behind in keeping up with inflation. We could potentially see a similar situation in 2025.

COLA Calculation Controversy

In recent years, there has been growing controversy over how the Social Security Administration calculates the annual cost-of-living adjustment for benefits. While the COLA is based on the Consumer Price Index (CPI), which tracks the prices of various goods and services within the U.S. economy, questions have arisen about whether the specific goods and services included in the CPI basket are still a good reflection of overall price increases across the economy.

Many consumers would agree that it feels like prices increased by more than 3.2% in 2024. If the Federal Reserve successfully delivers a soft landing, avoids a recession, and the economy starts growing at a faster pace, what are the chances that prices will rise by more than 2.5% in 2025? I'd say the chances are high.

Retirees Are in a Tough Spot

Many retirees live on fixed incomes, and Social Security benefits often represent a large portion of their total yearly income. If the COLA increases for Social Security do not adequately keep pace with rising costs, retirees may be forced to either reduce their spending or consider re-entering the workforce on a part-time basis to generate more income to meet their expenses.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Social Security: Suspending Payments vs. Withdraw of Benefits Election

It’s not an uncommon occurrence when a retiree turns on their social security benefits, but then all of a sudden take on either part-time or full-time employment, begin making more income than they expected, and they start searching for options to suspend their social security benefits until a later date.

The good news is there are “do-over” options for your social security benefit that exist depending on your age and how long it’s been since you started receiving your social security benefits. The are two different strategies:

If you have started receiving your social security benefits but you now want to suspend receiving your social security payments going forward, you have two options available to you. You can either:

Suspending Your Social Security Benefit

Withdrawing Your Social Security Benefit

They seem like the same thing, but they are two completely different strategies. One option requires you to pay back the social security benefits already received; the other does not. One option has an age restriction; the other does not.

Some of the most common reasons why retirees elect to either suspend or withdraw their social security benefits are:

Retirees either take on either part-time or full-time employment or receives an inheritance, they no longer need their social security benefit to supplement their income, and they would prefer to allow their social security benefit to keep growing by 6% - 8% per year.

A retiree turns on their social security prior to Full Retirement Age, begins making income over the allowable social security threshold, and is now faced with the social security earned income penalty

Since social security benefits are taxable income to many retirees, by suspending their social security payments, it opens up valuable tax and wealth accumulation strategies. We will cover a number of those strategies in this article.

Social Security: Withdraw of Benefits

The Withdraw of Benefits option is ONLY available if you started receiving your social security benefits within the past 12 months. If you are reading this article and you started receiving your social security benefits more than a year ago, you are not eligible for the withdraw of benefits strategy (however, you may still be eligible for a suspension of benefits covered later).

You can withdraw your benefits at any age: 62, 64, 68, etc. We find that the Withdrawal of Benefits strategy is the most common for retirees that retired before their Social Security Full Retirement Age (FRA), turned on their SS benefits early, began working again, and make more income than they expected. They realize very quickly that this scenario can have the following negative impacts on their social security benefits:

They may incur an Earning Income Penalty which claws back some of the social security benefits that they received.

A larger percentage of their social security benefit may be subject to taxation

They may have to pay a higher tax rate on their social security benefits

By turning on their social security early, they permanently reduced the amount of their social security benefit. Had they known they would earn this extra income, they would have waited and allowed their social security benefit to continue to grow.

You Must Repay The Social Security Benefits That You Received

Since the Withdrawal of Benefits option is the truest “Do-Over” option, you, unfortunately, must return to social security all of the benefit payments you received within the last 12 months. If you received $1,000 per month for the past 10 months and you file a Form SSA-521, you will be required to return the $10,000 that you received to social security. However, in addition to returning the social security benefits that you received, you also have to return the following:

Payments made to your spouse under the 50% spousal benefit

Payments to your children made under the dependent benefit

Voluntary federal and state taxes that were withheld from your social security payments

Medicare premiums that were withheld from your social security payments

This is why this option is the purest “do-over.” Once you have filed the Withdraw of Benefits and repaid social security the required amount, it’s like it never happened.

One Lifetime Withdrawal

To prevent abuse, you are only allowed one “Withdraw of Benefits” application during your lifetime.

How To Apply For A Social Security Withdraw of Benefits

You can apply to withdraw your benefits by mailing or hand-delivering form SSA-521 to your local social security office. Once Social Security has approved your withdrawal application, you have 60 days to change your mind.

Suspending Your Social Security Benefits

Now let’s shift gears to the second strategy, which involves voluntarily suspending your social security benefits. Why is a “Suspension” different than a “Withdrawal of Benefits”?

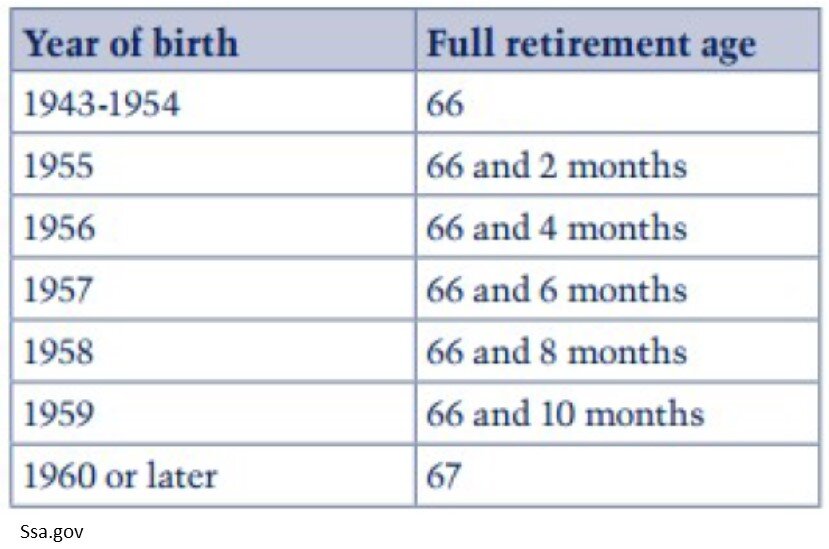

You are only allowed to “suspend” your social security benefits AFTER you have reached Full Retirement Age (FRA). For anyone born 1960 or later, that would be age 67. Suspending your benefit is not an option if you have not yet reached your social security full retirement age.

You do not have to repay the social security benefits you already received.

By suspending your benefits, the monthly payments cease as of the suspension date, and from that date forward, your social security benefit continues to grow at a rate of 8% per year until the maximum social security age of 70.

Restarting Your Suspended SS Benefits

If you decide to suspend your social security benefits, you can elect to turn that back on at any time. For example, you retire at age 67 and turn on your social security benefit of $2,000 per month, but then your friend approaches you about a consulting gig that will pay you $40,000 only working 2 days a week. You no longer need your social security benefits to cover your expenses, so you contact your local social security office and request that they suspend your benefits. A year later, the consulting gig ends; you can go back to the social security office, and request that they resume your social security payments which have now increased by 8% and will now be $2,160 per month.

How Do You Suspend Your Social Security Benefits?

You can request a suspension by phone, in writing, or by visiting your local social security office.

Reasons To Consider Suspending Your Social Security Benefit

As financial planners, we work with clients to identify wealth accumulation strategies, some basic and some more advanced. In this section I’m going to share with you some of the situations where we have advised clients to suspend their social security benefits:

Income Not Needed: This one we already cover in the example but if a client finds that they don’t need their social security income to meet their expenses, stopping the benefit, and taking advantage of the 8% guaranteed increase in the benefit every year until age 70 is an attractive option. I’m not aware of any investment options at this time that offers a guaranteed 8% rate of return.

Increasing The Survivor Benefits: By suspending your social security benefit, if your social security benefit is higher than your spouse’s benefit, you are increasing the social security survivor benefit that would be available to your spouse if you pass away first. When one spouse passes away, only one social security payment continues, and it’s the higher of the two.

Reduce Taxable Income: Retirees are often surprised to find out that up to 85% of the social security benefits received could be taxed as ordinary income at the federal level and there are a handful of states that tax social security at the state level. If there is temporary income right now that will sunset, instead of your social security benefit being stacked on top of your other taxable income, making it subject to higher tax rates, it may be beneficial to suspend your social security benefit until a later date.

Roth Conversions: Roth conversions can be a fantastic long-term wealth accumulation strategy in retirement but what makes these conversions work, is after you have retired, most retirees are in a lower tax bracket which allows them to convert pre-tax retirement accounts to a Roth IRA, and realize those conversions at a low tax rate. However, as I just mentioned, social security is taxable income, by suspending your social security benefit, and removing that taxable income from the table, it can open up room for larger Roth conversions.

Reduce Future RMDs: For pre-tax IRAs and 401(k), once you reach either 73 or 75 depending on your date of birth, the IRS forces you to start taking taxable required minimum distributions (RMDs) from those retirement accounts. It’s not uncommon for retirees with pensions to retire, they turn on their pension payment and social security payments, and that is more than enough to meet their retirement income needs. However, often times these retirees also have pre-tax retirement accounts that they do not need to take withdraws from to supplement their income so the plan is to just let them continue to accumulate in value.

The problem becomes, if no distributions are taken from those accounts, the balances continue to grow, making the RMDs larger later on, which could make those distributions subject to higher tax rates. Instead, it may be a better strategy to suspend your social security benefits which would allow you to start taking distribution from your pre-tax retirement accounts now, in an effort to reduce the future RMD amounts.

Life Expectancy Protection: With everyone living longer, there is the risk that a retiree could outlive their personal retirement savings but social security payments last for the rest of your life. By suspending your social security benefit and receiving the 8% per year increase, your social security benefit will support a larger percentage of your annual expenses. Also, unlike IRA accounts, social security receives a COLA (cost of living adjustment) each year which increases your social security benefit for inflation. By delaying the benefit, the COLA is now being applied to a higher social security benefit.

Choosing Between Withdraw or Suspend

If you have already reached FRA and you turned on your social security benefit less than 12 months ago, you have the option to either “Suspend” your benefit or “Withdraw” your benefit.

If you suspend your benefit, you do not have to pay back any of the social security benefits that you already received, and your social security benefit will continue to accumulate at 8% per year until you elect to turn your social security back on.

If instead, you decide to withdraw your benefit, yes, you have to pay back any social security payments that you already received but there is one advantage. Since the withdrawal of benefits is a complete “do-over”, you received credit for the 8% per year increase all the way back to your start date. This is not the case with the suspend strategy. If a client has $20,000 in idle cash and they received $20,000 in social security benefits over the past 11 months, if they use their $20,000 to pay back social security, it’s like you are receiving an 8% return on that $20,000 because your social security will be 8% a year from your start date. Not a bad return on your idle cash.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Turn on Social Security at 62 and Your Minor Children Can Collect The Dependent Benefit

Not many people realize that if you are age 62 or older and have children under the age of 18, your children are eligible to receive social security payments based on your earnings history, and it’s big money. However, social security does not advertise this little know benefit, so you have to know how to apply, the rules, and tax implications.

Not many people realize that if you are age 62 or older and have children under the age of 18, your children are eligible to receive social security payments based on your earnings history, and it’s big money. However, social security does not advertise this little know benefit, so you have to know how to apply, the rules, and tax implications. In this article, I will walk you through the following:

The age limit for your children to be eligible to receive SS benefits

The amount of the payments to your kids

The family maximum benefit calculation

How the benefits are taxed to your children

How to apply for the social security dependent benefits

Pitfall: You may have to give the money back to social security…..

Eligibility Requirements for Dependent Benefits

Three requirements make your children eligible to receive social security payments based on your earnings history:

You have to be age 62 or older

You must have turned on your social security benefit payments

Your child must be unmarried and meet one of the following eligibility requirements:

Under the age of 18

Between the ages of 18 and 19 and a full-time student K – 12

Age 18 or older with a disability that began before age 22

How Much Does Your Child Receive?

If you are 62 or older, you have turned on your social security benefits, and your child meets the criteria above, your child would be eligible to receive 50% of your Full Retirement Age (FRA) Social Security Benefit EVERY YEAR, until they reach age 18. This can sometimes change a parent’s decision to turn on their social security benefit at age 62 instead of waiting until their Full Retirement Age of 67 (for individuals born in 1960 or later). But it gets better because the 50% of your FRA social security benefit is for EACH child.

For example, Jim is retired, age 62, and he has one child under age 18, Josh, who is age 12. If he turns on his social security benefit at age 62, he would receive $1,200 per month, but if he waits until his FRA of 67, he would receive $1,700 per month. Even though Jim would receive a lower social security benefit at age 62, if he turns on his benefit at age 62, Jim and his child Josh would receive the following monthly payments from social security:

Jim: $1,200 ($14,400 per year)

Josh: $850 ($10,200 per year)

Even though Jim receives a reduced SS benefit by turning on his benefit at age 62, the 50% dependent child benefit is still calculated based on Jim’s Full Retirement Age benefit of $1,700. Josh will be eligible to continue to receive monthly payments from social security until the month of his 18th birthday. That’s a lot of money that could go towards college savings, buying a car, or a down payment on their first house.

The Family Maximum Benefit Limit

If you have 10 children, I have bad news; social security imposes a “family maximum benefit limit” for all dependents eligible to collect on your earnings history. The family benefits are limited to 150% to 188% of the parent’s full retirement age benefit.

I’ll explain this via an example. Let’s assume everything is the same as in the previous example with Jim, but now Jim has four children, all under 18. Let’s also assume that Jim’s Family maximum benefit is 150% of his FRA benefit, which would equal a maximum family benefit of $2,550 per month ($1,700 x 150%). We now have the following:

Jim: $1,200

Child 1: $850

Child 2: $850

Child 3: $850

Child 4: $850

If you total up the monthly social security benefits paid to Jim and his children, it equals $4,600, which is $2,050 over the $2,550 family maximum benefit limit.

Always Use Your FRA Benefit In The Family Max Calculation

Here is another important rule to note when calculating the family maximum benefit, regardless of when your file for your social security benefits, age 62, 64, 67, or 70, you always use your Full Retirement Age benefit when calculating the Family Maximum Benefit amount. In the example above, Jim filed for social security benefits early at age 62. Instead of using Jim’s age $1,200 social security benefit to calculate the remaining amount available for his children, Jim has to use his FRA benefit of $1,700 in the formula before determining how much his children are eligible to receive.

Social security would reduce the children’s benefits by an equal amount until their total benefit is reduced to the family maximum limit.

These are the steps:

Jim Max Family Benefit = $1,700 (FRA) x 150% = $2,550

$2,550 (Family Max) - $1,700 (Jim FRA) = $850

Divide $850 by Jim’s 4 eligible children = $212.50 for each child

This results in the following social security benefits paid to Jim and his 4 children:

Jim: $1,200

Child 1: $212.50

Child 2: $212.50

Child 3: $212.50

Child 4: $212.50

A note about ex-spouses, if someone was married for more than 10 years, then got divorced, the ex-spouse may still be entitled to the 50% spousal benefit, but that does not factor into the family maximum calculation, nor is it reduced for any family maximum benefit overages.

Social Security Taxation

Social security payments received by your children are considered taxable income, but that does not necessarily mean that they will owe any tax on the amounts received. Let me explain, your child’s income has to be above a specific threshold before they owe any federal taxes on the social security benefits they receive.

You have to add up all of their regular taxable income and tax-exempt income and then add 50% of the social security benefits that they received. If your child has no other income besides the social security benefits, it’s just 50% of the social security benefits that were paid to them. If that total is below $25,000, they do not have to pay any federal tax on their social security benefit. If it’s above that amount, then a portion of the social security benefits received will be taxable at the federal level.

States have different rules when it comes to taking social security benefits. Most states do not tax social security benefits, but there are about 13 states that assess state taxes on social security benefits in one form or another, but our state New York, is thankfully not one of them.

You Can Still Claim Your Child As A Dependent On Your Tax Return

More good news, even though your child is showing income via the social security payment, you can still claim them as a dependent on your tax return as long as they continue to meet the dependent criteria.

How To Apply For Social Security Dependent Benefits

You cannot apply for your child’s dependent benefits online; you have to apply by calling the Social Security Administration at 800-772-1213 or scheduling an appointment at your local Social Security office.

Be Care of This Pitfall

There is one pitfall to the social security payment received by your child or children, it’s not a pitfall about the money received, but the issue revolves around the titling of the account that the social security benefits are deposited into when they are received on behalf of the child.

The premise behind social security providing these benefits to the minor children of retirees is that if someone retires at age 62 and still has minor children as dependents, they may need additional income to support the household expenses. Whether that is true or not does not prevent you from taking advantage of these dependent payments to your children, but it does raise the issue of the “conserved benefits” letter that many people receive once the child turns age 18.

You may receive a letter from social security once your child is 18 instructing you to return any of the social security dependent payments received on your child’s behalf and saved. So wait, if you save this money for our child to pay for college, you have to hand it back to social security, but if you spend it, you get to keep it? On the surface, the answer is “yes,” but it all depends on who is listed as the account owner that the social security payments are deposited into on behalf of your child.

If the parent is listed as an owner or joint owner of the account, you are expected to return the saved or “conserved” payment to the Social Security Administration. However, if the account that the social security payments are deposited into is owned 100% by your child, you do not have to return the saved money to social security.

Then I will get the question, “Well, what type of account can you set up for a 12-year-old that they own 100%?” Some banks will allow you to set up savings accounts in the name of a child at age 14, UTMA accounts can be set up at any age, and they are considered accounts owned 100% by the child even though a parent is listed as a custodian.

Watch out for the 529 account pitfall. For parents that want to use these Social Security payments to help subsidize college savings, they will sometimes set up a 529 account and deposit the payments into that account to take advantage of the tax benefits. Even though these 529 accounts are set up with the child listed as the beneficiary, they are often considered assets of the parents because the parent has control over the distributions from the account. However, you can set up 529 accounts as UTMA 529, which avoids this issue since the child is now technically the owner and has complete control over the assets at the age of majority.

FAFSA Considerations

Be aware that if your child is college bound and you expect to qualify for need-based financial aid, assets owned by the child count against the FAFSA calculation. The way the calculation works is that about 20% of any assets owned by the child count against the need-based financial aid that is awarded. There is no way around this issue, but it’s not the end of the world because that means 80% of the balance does not count against the FAFSA calculation and it was free money from Social Security that can be used to pay for college.

Social Security Filing Strategy

If you are age 62 or older and have minor children, it may very well make sense to file for Social Security early, even though it may permanently reduce your Social Security benefit once you factor in the Social Security payments that will be made to your children as dependents. But, you have to make sure you understand how Social Security is taxed, the Security earned income penalty, the impact of Social Security survivor benefits for your spouse, and many other factors before making this decision.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Do You Have To Pay Tax On Your Social Security Benefits?

I have some unfortunate news. If you look at your most recent paycheck, you are going to see a guy by the name of “FICA” subtracting money from your take-home pay. Part of that FICA tax is sent to the Social Security system, which entitles you to receive Social Security payments when you retire. The unfortunate news is that, even though it was a tax that you paid while you were working, when you go to receive your payments from Social Security, most retirees will have to pay some form of Income Tax on it. So, it’s a tax you pay on a tax? Pretty much!

In this article, I will be covering:

· The percent of your Social Security benefit that will be taxable

· The tax rate that you pay on your Social Security benefits

· The Social Security earned income penalty

· State income tax exceptions

· Withholding taxes from your Social Security payments

What percent of your Social Security benefit is taxable?

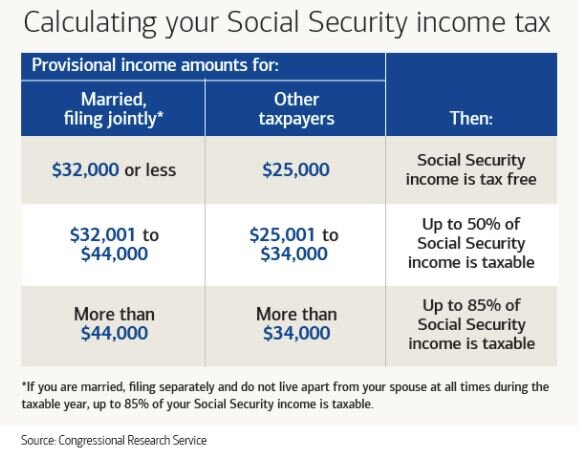

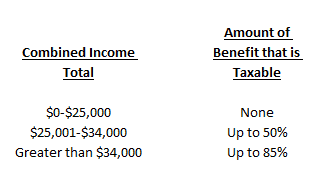

First, let’s start off with how much of your Social Security will be considered taxable income. It ranges from 0% to 85% of the amount received. Where you fall in that range will depend on the amount of income that you have each year. Here is the table for 2021:

But, here’s the kicker. 50% of your Social Security benefit that you receive counts towards the income numbers that are listed in the table above to arrive at your “combined Income” amount. Here is the formula:

Adjusted Gross Income (AGI) + nontaxable interest + 50% of your SS Benefit = Combined Income

If you are a single tax filer, and you are receiving $30,000 in Social Security benefits, you are already starting at a combined income level of $15,000 before you add in any of your other income from employment, pensions, pre-tax distributions from retirement accounts, investment income, or rental income.

As you will see in the table, if your combined income for a single filer is below $25,000, or a joint filer below $32,000, you will not have to pay any tax on your Social Security benefit. Taxpayers above those thresholds will have to pay some form of tax on their Social Security benefits. But, I have a small amount of good news: no one has to pay tax on 100% of their benefit, because the highest percentage is 85%. Therefore, everyone at a minimum receives 15% of their benefit tax free.

NOTE: The IRS does not index the combined income amounts in the table above for inflation, meaning that even though an individual’s Social Security and wages tends to increase over time, the dollar amounts listed in the table stay the same from year to year. This has caused more and more taxpayers to have to pay tax on a larger portion of their Social Security benefit over time.

Tax Rate on Social Security Benefits

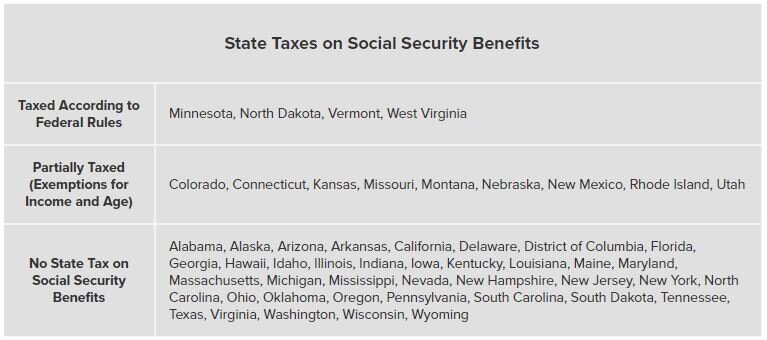

Your Social Security benefits are taxed as ordinary income. There are no special tax rates for Social Security like capital gains rates for investment income. Social Security is taxed at the federal level but may or may not be taxed at the state level. Currently there are 37 states in the U.S. that do not tax Social Security benefits. There are 4 states that tax it at the same level as the federal government and there are 13 states that partially tax the benefit. Here is table:

Withholding Taxes From Your Social Security Benefit

For taxpayers that know that will have to pay tax on their Social Security benefit, it is usually a good idea to have Social Security withholding taxes taken directly from your Social Security payments. Otherwise, you will have to issue checks for estimated tax payments throughout the year which can be a headache. They only provide you with four federal tax withholding options:

· 7%

· 10%

· 12%

· 22%

These percentages are applied to the full amount of your Social Security benefit, not to just the 50% or 85% that is taxable. Just something to consider when selecting your withholding elections.

To make a withholding election, you have to complete Form W-4V (Voluntary Withholding Request). Once you have completed the form, which only has 7 lines, you can mail it or drop it off at the closest Social Security Administration office.

Social Security Earned Income Penalty

If you elect to turn on your Social Security benefit prior to your Normal Retirement Age (NRA) AND you plan to keep working, you have to be aware of the Social Security earned income penalty. Your Normal Retirement Age is the age that you are entitled to receive your full Social Security benefit, and it’s based on your date of birth.

The earned income penalty ONLY applies to taxpayers that turn on their Social Security prior to their normal retirement age. Once you have reached your normal retirement age, this penalty does not apply.

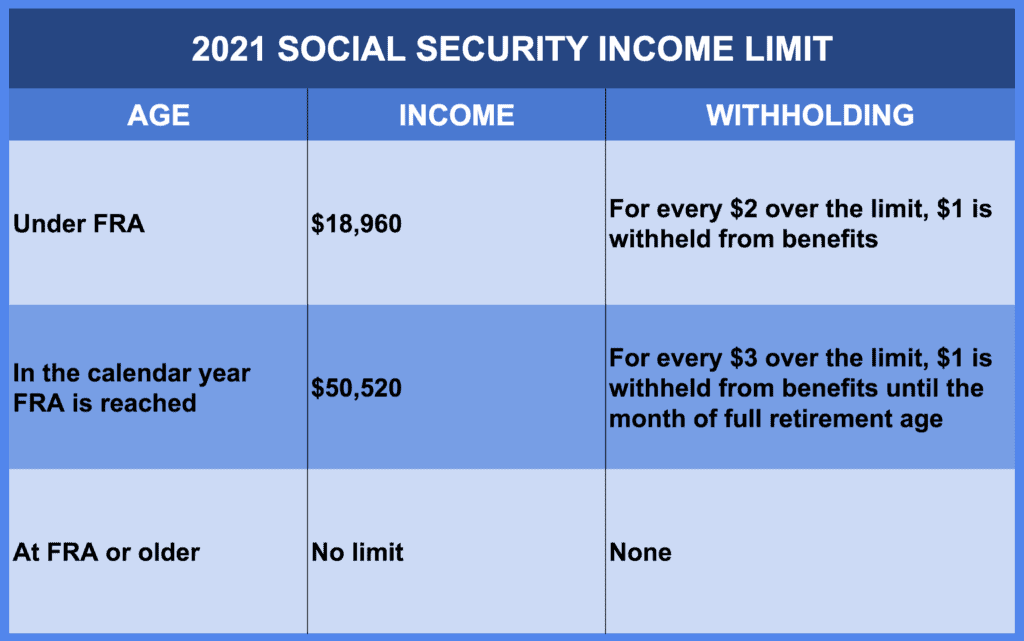

Basically, the IRS limits how much you are allowed to make each year if you elect to turn on your Social Security early. If you earn over those amounts, you may have to pay all or a portion of the Social Security benefit back to the government. In the Chart below “FRA” stands for “Fully retirement age”, which is the same as “Normal Retirement Age” (NRA). Also note that for married couples, the earned income numbers below apply to your personal earnings, and do not take into consideration your spouse’s income.

INCOME UNDER $18,960: If you earned income is below $18,960, no penalty, you get to keep your full social security benefit

INCOME OVER $18,960: You lose $1 of your social security benefit for every $2 you earn over the threshold. Example:

· You turn on your social security at age 63

· Your social security benefit is $20,000 per year

· You make $40,000 per year in wages

Since you made $40,000 in wages, you are $21,040 over the $18,960 limit:

$21,040 x 50% ($1 reduction for every $2 earned) = $10,520 penalty.

The following year, your $20,000 Social Security benefit would be reduced by $10,520 for the assessment of the earned income penalty. Ouch!!

As a general rule of thumb, if you plan on working prior to your Social Security normal retirement age, and your wages will be in excess of the $18,960 limit, it usually make sense to wait to turn on your Social Security benefit until your wages are below the threshold or you reach normal retirement age.

NOTE: You will see in the middle row of the table “In the calendar year FRA is reached”. In the year that you reach your full retirement age for social security the wage threshold his higher and the penalty is lower (a $1 penalty for every $3 over the threshold).

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

How Do Social Security Survivor Benefits Work?

Social Security payments can sometimes be a significant portion of a couple’s retirement income. If your spouse passes away unexpectedly, it can have a dramatic impact on your financial wellbeing in retirement. This is especially

Social Security payments can sometimes be a significant portion of a couple’s retirement income. If your spouse passes away unexpectedly, it can have a dramatic impact on your financial wellbeing in retirement. This is especially true if there was a big income difference between you and your spouse. In this article we will review:

Who is eligible to receive the Social Security Survivor Benefit

How the benefit is calculated

Electing to take the benefit early vs. delaying the benefit

Filing strategies that allow the surviving spouse to receive more from Social Security

Social Security Earned Income Penalty

Social Security filing strategies that married couples should consider to preserve the Survivor Benefit

Divorce: 2 Ex-spouses & 1 Current Spouse: All receiving the same Survivor Benefit

How Much Social Security Does A Surviving Spouse Receive?

When your spouse passes away, as the surviving spouse, you are entitled to receive the higher of the two benefits. You do not continue to collect both benefits simultaneously.

Example: Jim is age 80 and he is collecting a Social Security benefit of $2,500 per month. His wife Sarah is 79 and is collecting $2,000 per month for her Social Security benefit.

If Jim passes away first, Sarah would begin to receive $2,500 per month, but her $2,000 per month benefit would end.

If Sarah passes away first, Jim would continue to receive his $2,500 per month because his benefit was the higher of the two, and Sarah’s Social Security payments would end.

Married For 9 Month

To be eligible for the Social Security Survivor Benefit as the spouse, you have to have been married for at least nine months prior to your spouse passing away. If the marriage was shorter than that, you are not entitled to the Social Security Survivor Benefit.

Increasing Your Spouse’s Survivor Benefit

Due to this higher of the two rule, as financial planners we work this into the Social Security filing strategy for our clients. Before we get into the strategy, let’s do a quick review of your filing options and how it impacts your Social Security benefit.

Normal Retirement Age

Each of us has a Normal Retirement Age for Social Security which is based on our date of birth. The Normal Retirement Age is the age that you are entitled to your full Social Security benefit:

Should You Turn On The Benefit Early?

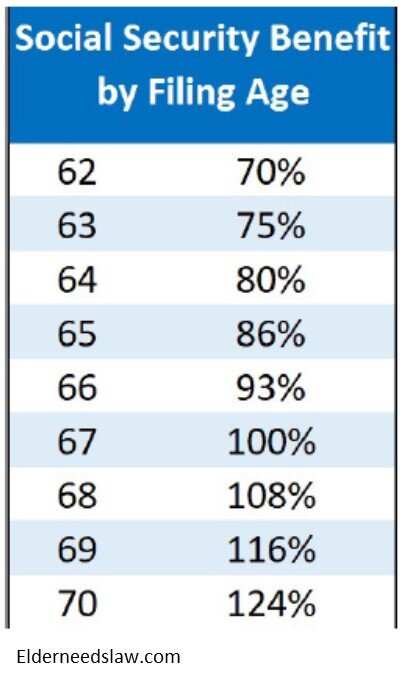

For your own personal Social Security benefit, once you reach age 62, you have the option to turn on your Social Security benefit early. However, if you elect to turn on your Social Security benefit prior to Normal Retirement Age, your monthly benefit is permanently reduced by approximately 6% per year for each year you take it early. So, if your normal retirement age is 67 and you file for Social Security at age 62, you only receive 70% of your full benefit and that is a permanent reduction.

On the flip side, if you delay filing for Social Security past your normal retirement age, your Social Security benefit increases by about 8% per year until you reach age 70.

There is no benefit to delaying Social Security past age 70.

How This Factors Into The Survivor Benefit

The decision of when you turn on your Social Security benefit will ultimately impact the Social Security Survivor Benefit that is available to your spouse should you pass away first. Remember, it’s the higher of the two. When there is a large gap between the amount that you and your spouse will receive from Social Security, it’s not uncommon for us to recommend that the higher income earner should delay filing for Social Security as long as possible. By delaying the start date, it increases the monthly amount that higher income earning spouse receives, which in turn preserves a higher monthly survivor benefit regardless of which spouse passes away first.

Example: Matt and Sarah are married, they are both 62, they retired last year, and they are trying to decide if they should turn on their Social Security benefit now, waiting until Normal Retirement Age, or delay it until age 70. Matt’s Social Security benefit at age 67 would be $2,700 per month. Sarah Social Security benefit at age 67 would be $2,000 per month.

They need $7,000 per month to meet their expenses. If Matt and Sarah both took their Social Security benefits at age 62, Matt’s benefit would be reduced to $1,890 per month and Sarah’s benefit would be reduced to $1,400 per month. At age 75, Matt passes away from a heart attack. Sarah’s Social Security benefit would increase to the amount that Matt was receiving, $1,890, and Sarah’s benefit of $1,400 per month would end. Since Sarah’s monthly expenses are still close to $7,000 per month, with the loss of the second Social Security benefit, she would have to withdraw $5,110 per month from another source to meet the $7,000 in monthly expenses. That’s $61,320 per year!!

Let’s compare that scenario to Matt waiting to file for his Social Security benefit until age 70 and Sarah turning on her Social Security benefit at age 62. By turning on Sarah’s benefit at age 62, it provides them with some additional income to meet expense, but when Matt turns 70, he will now receive $3,348 per month from Social Security. If Matt passes away at age 75, Sarah now receives Matt’s $3,348 per month from Social Security and her lower benefit ends. However, since the Social Security payments are higher than the previous example, now Sarah only needs to withdraw $3,652 per month from her personal savings to meet her expenses. That equals $43,824 per year.

If Sarah lives to age 90, by Matt making the decision to delay his Social Security Benefit to age 70, that saved Sarah an additional $262,400 that she otherwise would have had to withdraw from her personal savings over that 15 year period.

Age 60 - Surviving Spouse Benefit

As mentioned above, with your personal Social Security retirement benefits, you have the option to turn on your Social Security payments as early as age 62 at a reduced amount. In contrast, if your spouse predeceases you, you are allowed to turn on the Social Security Survivor Benefit as early as age 60.

Similar to turning on your personal Social Security benefit at age 62, if you elect to receive the Social Security Survivor Benefit prior to reaching your normal retirement age, Social Security reduces the benefit by approximately 6% per year, for each year that you start receiving the benefit prior to your normal retirement age.

Advance Filing Strategy

There is an advanced filing strategy associated with the Survivor Benefit. Social Security allows you to turn on the Survivor Benefit which is based on your spouse’s earnings history and defer your personal benefit until a future date. This allows your benefit to continue to grow even though you are currently receiving payments from Social Security. When you turn age 70, you can switch over to your own benefit which is at its maximum dollar threshold. But you would only do this, if your benefit was higher than the survivor benefit.

Example: Mike and Lisa are married and are both entitled to receive $2,000 per month from Social Security at age 67. Mike passes away unexpectedly at age 50. When Lisa turns 60, she will have to option to turn on the Social Security Survivor Benefit based on Mike’s earnings history at a reduced amount of $1,160 per month. In the meantime, Lisa can allow her personal Social Security benefit to continue to grow, and at age 70, Sarah can switch from the Surviving Spouse Benefit of $1,160 over to her personal benefit of $2,480 per month.

Beware of the Social Security Earned Income Penalty

If you are considering turning on your Social Security benefits prior to your normal retirement age, you must be aware of the Social Security earned income penalty. This is true for both your own personal Social Security benefits and the benefits you may receive as the surviving spouse. In 2020, if you are receiving Social Security benefits prior to your normal retirement age and you have earned income over $18,240 for that calendar year, not only are you receiving the benefit at a permanently reduced amount but Social Security assesses a penalty at the end of the year which is equal to $1 for every $2 of income over that threshold.

Example: Jackie decides to turn on her Social Security Survivor Benefits at age 60 in the amount of $1,000 per month. She is still working and will receive $40,000 in W-2 income. Based on the formula, of the $12,000 in Social Security payments that Jackie received, Social Security would assess a $10,880 penalty against that amount. So she basically loses it all to the penalty.

For clarification purposes, when Social Security levies the earned income penalty, they do not require you to issue them a check for the dollar amount of the penalty; instead, they deduct the amount that is due to them from your future Social Security payments. This usually happens shortly after you file your tax return for the previous year because the IRS uses your tax return to determine if the earned income penalty applies.

For this reason, there is a general rule of thumb that if you have not reached your normal retirement age for Social Security and you anticipate receiving income during the year well above the $18,240 threshold, it typically does not make sense to turn on the Social Security benefits early. It just ends up creating more taxable income for you, and you end up losing most or all of the money the next year when Social Security assesses the earned income penalty against your future benefits.

Once you reach normal retirement age, this earned income penalty no longer applies. You can turn on Social Security benefits and make as much as you want without a penalty.

Divorce

We find that many ex-spouses are not aware that they are also entitled to the Social Security Survivor Benefit if they were married to the decedent for more than 10 years prior to the divorce. Meaning if your ex-spouse passes away and you were married more than 10 years, if the monthly benefit that they were receiving from Social Security is higher than yours, you go back to Social Security, file under the Survivor Benefit, and your benefit will increase to their amount.

The only way you lose this option is if you remarry prior to age 60. However, if you get remarried after age 60, it does not jeopardize your ability to claim the Survivor Benefit based on your ex-spouse’s earnings history.

If your ex-spouse was remarried at the time they passed away, you are still entitled to receive the Survivor Benefit. In addition, their current spouse will also be able to claim the Survivor Benefit simultaneously and it does not reduced the amount that you receive as the ex-spouse.

There was even a case where an individual was divorced twice, both marriages lasted more than 10 years, and he was remarried at the time he passed away. After his passing, the two ex-spouses and the current spouse were all eligible to receive the full Social Security Survivor Benefit based on his earnings history.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Potential Consequences of Taking IRA Distributions to Pay Off Debt

Once there is no longer a paycheck, retirees will typically meet expenses with a combination of social security, withdrawals from retirement accounts, annuities, and pensions. Social security, pensions, and annuities are usually fixed amounts, while withdrawals from retirement accounts could fluctuate based on need. This flexibility presents

Potential Consequences of Taking IRA Distributions to Pay Off Debt

Once there is no longer a paycheck, retirees will typically meet expenses with a combination of social security, withdrawals from retirement accounts, annuities, and pensions. Social security, pensions, and annuities are usually fixed amounts, while withdrawals from retirement accounts could fluctuate based on need. This flexibility presents opportunities to use retirement savings to pay off debt; but before doing so, it is important to consider the possible consequences.

Clients often come to us saying they have some amount left on a mortgage and they would feel great if they could just pay it off. Lower monthly bills and less debt when living on a fixed income is certainly good, both from a financial and psychological point of view, but taking large distributions from retirement accounts just to pay off debt may lead to tax consequences that can make you worse off financially.

Below are three items I typically consider before making a recommendation for clients. Every retiree is different so consulting with a professional such as a financial planner or accountant is recommended if you’d like further guidance.

Impact on State Income and Property Taxes

Depending on what state you are in, withdrawals from IRA’s could be taxed very differently. It is important to know how they are taxed in your state before making any big decision like this. For example, New York State allows for tax free withdrawals of IRA accounts up to a maximum of $20,000 per recipient receiving the funds. Once the $20,000 limit is met in a certain year, any distribution you take above that will be taxed.

If someone normally pulls $15,000 a year from a retirement account to meet expenses and then wanted to pull another $50,000 to pay off a mortgage, they have created $45,000 of additional taxable income to New York State. This is typically not a good thing, especially if in the future you never have to pull more than $20,000 in a year, as you would have never paid New York State taxes on the distributions.

Note: Another item to consider regarding states is the impact on property taxes. For example, New York State offers an “Enhanced STAR” credit if you are over the age of 65, but it is dependent on income. Here is an article that discusses this in more detail STAR Property Tax Credit: Make Sure You Know The New Income Limits.

What Tax Bracket Are You in at the Federal Level?

Federal income taxes are determined using a “Progressive Tax” calculation. For example, if you are filing single, the first $9,700 of taxable income you have is taxed at a lower rate than any income you earn above that. Below are charts of the 2019 tax tables so you can review the different tax rates at certain income levels for single and married filing joint ( Source: Nerd Wallet ).

There isn’t much of a difference between the first two brackets of 10% and 12%, but the next jump is to 22%. This means that, if you are filing single, you are paying the government 10% more on any additional taxable income from $39,475 – $84,200. Below is a basic example of how taking a large distribution from the IRA could impact your federal tax liability.

How Will it Impact the Amount of Social Security You Pay Tax on?

This is usually the most complicated to calculate. Here is a link to the 2018 instructions and worksheets for calculating how much of your Social Security benefit will be taxed ( IRS Publication 915 ). Basically, by showing more income, you may have to pay tax on more of your Social Security benefit. Below is a chart put together with information from the IRS to show how much of your benefit may be taxed.

To calculate “Combined Income”, you take your Adjusted Gross Income + Nontaxable Interest + Half of your Social Security benefit. For the purpose of this discussion, remember that any amount you withdraw from your IRA is counted in your Combined Income and therefore could make more of your social security benefit subject to tax.

Peace of mind is key and usually having less bills or debt can provide that, but it is important to look at the cost you are paying for it. There are times that this strategy could make sense, but if you have questions about a personal situation please consult with a professional to put together the correct strategy.

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

Social Security Filing Strategies

Making the right decision of when to turn on your social security benefit is critical. The wrong decision could cost you tens of thousands of dollars over the long run. Given all the variables surrounding this decision, what might be the right decision for one person may be the wrong decision for another. This article will cover some of the key factors to

Making the right decision of when to turn on your social security benefit is critical. The wrong decision could cost you tens of thousands of dollars over the long run. Given all the variables surrounding this decision, what might be the right decision for one person may be the wrong decision for another. This article will cover some of the key factors to consider:

Normal Retirement Age

First, you have to determine your "Normal Retirement Age" (NRA). This is listed on your social security statement in the "Your Estimated Benefits" section. If you were born between 1955 – 1960, your NRA is between age 66 – 67. If you were born 1960 or later, your NRA is age 67. You can obtain a copy of your statement via the social security website.

Before Normal Retirement Age

You have the option to turn on social security prior to your normal retirement age. The earliest you can turn on social security is age 62. However, they reduce your social security benefit by approximately 7% per year for each year prior to your normal retirement age. See the chart below from USA Today which illustrates an individual with a normal retirement age of 66. If they turn on their social security benefit at age 62, they would only receive 75% of their full benefit. This reduction is a permanent reduction. It does not increase at a later date, outside of the small cost of living increases.

taking social security early

The big questions is: “If I start taking it age 62, at what age is the breakeven point?” Remember, if I turn on social security at 62 and my normal retirement age is 66, I have received 4 years of payments from social security. So at what age would I be kicking myself wishing that I had waited until normal retirement age to turn on my benefit. There are a few different ways to calculate this accounting for taxes, the rates of return on other retirement assets, inflations, etc. but in general it’s sometime between the ages of 78 and 82.

Since the breakeven point may be in your early 80’s, depending on your health, and the longevity in your family history, it may or may not make sense to turn on your benefit early. If we have a client that is in ok health but not great health and both of their parents passed way prior to age 85, then it may make sense to for them to turn on their social security benefit early. We also have clients that have pensions and turning on their social security benefit early makes the different between retiring now or have to work for 5+ more years. As long as the long-term projections work out ok, we may recommend that they turn on their social security benefit early so they can retire sooner.

Are You Still Working?

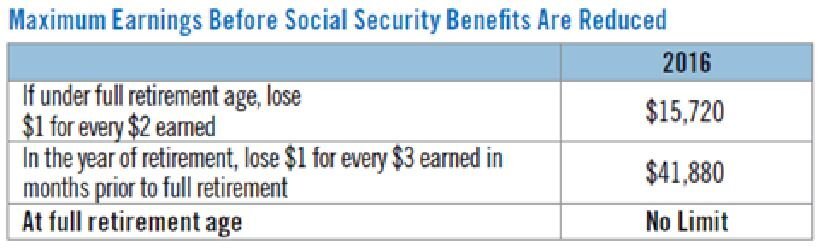

This is a critical question for anyone that is considering turning on their social security benefits early. Why? If you turn on your social security benefit prior to reaching normal retirement age, there is an “earned income” penalty if you earn over the threshold set by the IRS for that year. See the table listed below:

In 2016, for every $2 that you earned over the $15,720 threshold, your social security was reduced by $1. For example, let’s say I’m entitled to $1,000 per month ($12,000 per year) from social security at age 62 and in 2016 I had $25,000 in W2 income. That is $9,280 over the $15,720 threshold for 2016 so they would reduce my annual benefit by $4,640. Not only did I reduce my social security benefit permanently by taking my social security benefit prior to normal retirement age but now my $12,000 in annual social security payments they are going to reduce that by another $4,640 due to the earned income penalty. Ouch!!!

Once you reach your normal retirement age, this earned income penalty no longer applies and you can make as much as you want and they will not reduce your social security benefit.

Because of this, the general rule of thumb is if you are still working and your income is above the IRS earned income threshold for the year, you should hold off on turning on your social security benefits until you either reach your normal retirement age or your income drops below the threshold.

Should I Delay May Benefit Past Normal Retirement Age

As was illustrated in first table, if you delay your social security benefit past your normal retirement age, your benefit will increase by approximately 8% per year until you reach age 70. At age 70, your social security benefit is capped and you should elect to turn on your benefits.

So when does it make sense to wait? The most common situation is the one where you plan to continue working past your normal retirement age. It’s becoming more common that people are working until age 70. Not because they necessarily have too but because they want something to keep them busy and to keep their mind fresh. If you have enough income from employment to cover you expenses, in many cases, is does make sense to wait. Based on the current formula, your social security benefit will increase by 8% per year for each year you delay your benefit past normal retirement age. It’s almost like having an investment that is guaranteed to go up by 8% per year which does not exist.

Also, for high-income earners, a majority of their social security benefit will be taxable income. Why would you want to add more income to the picture during your highest tax years? It may very well make sense to delay the benefit and allow the social security benefit to increase.

Death Benefit

The social security death benefit also comes into play as well when trying to determine which strategy is the right one for you. For a married couple, when their spouse passes away they do not continue to receive both benefits. Instead, when the first spouse passes away, the surviving spouse will receive the “higher of the two” social security benefits for the rest of their life. Here is an example:

Spouse 1 SS Benefit: $2,000

Spouse 2 SS Benefit: $1,000

If Spouse 1 passes away first, Spouse 2 would bump up to the $2,000 monthly benefit and their $1,000 monthly benefit would end. Now let’s switch that around, let’s say Spouse 2 passes away first, Spouse 1 will continue to receive their $2,000 per month and the $1,000 benefit will end.

If social security is a large percentage of the income picture for a married couple, losing one of the social security payments could be detrimental to the surviving spouse. Due to this situation, it may make sense to have the spouse with the higher benefit delay receiving social security past normal retirement to further increase their permanent monthly benefit which in turn increases the death benefit for the surviving spouse.

Spousal Benefit

The “spousal benefit” can be a powerful filing strategy. If you are married, you have the option of turning on your benefit based on your earnings history or you are entitled to half of your spouse’s benefit, whichever benefit is higher. This situation is common when one spouse has a much higher income than the other spouse.

Here is an important note. To be eligible for the spousal benefit, you personally must have earned 40 social security “credits”. You receive 1 credit for each calendar quarter that you earn a specific amount. In 2016, the figure was $1,260. You can earn up to 4 credits each calendar year.

Another important note, under the new rules, you cannot elect your spousal benefit until your spouse has started receiving social security payments.

Here is where the timing of the social security benefits come into play. You can turn on your spousal benefit as early as 62 but similar to the benefit based on your own earnings history it will be reduce by approximately 7% per year for each year you start the benefit prior to normal retirement age. At your normal retirement age, you are entitled to receive your full spousal benefit.

What happens if you delay your spousal benefit past normal retirement age? Here is where the benefit calculation deviates from the norm. Typically when you delay benefits, you receive that 8% annual increase in the benefits up until age 70. The spousal benefit is based exclusively on the benefit amount due to your spouse at their normal retirement age. Even if your spouse delays their social security benefit past their normal retirement age, it does not increase the 50% spousal benefit.

Here is the strategy. If it’s determine that the spousal benefit will be elected as part of a married couple’s filing strategy, since delaying the start date of the benefits past normal retirement age will only increase the social security benefit for the higher income earning spouse and not the spousal benefit, in many cases, it does not make sense to delay the start date of the benefits past normal retirement age.

Divorce

For divorced couples, if you were married for at least 10 years, you can still elect the spousal benefit even though you are no longer married. But you must wait until your ex-spouse begins receiving their benefits before you can elect the spousal benefit.

Also, if you were married for at least 10 years, you are also entitled to the death benefit as their ex-spouse. When your ex-spouse passes away, you can notify the social security office, elect the death benefit, and you will receive their full social security benefit amount for the rest of your life instead of just 50% of their benefit resulting from the “spousal benefit” calculation.

Whether or not your ex-spouse remarries has no impact on your ability to elect the spousal benefit or death benefit based on their earnings history.

Consult A Financial Planner

Given all of the variables in the mix and the importance of this decision, we strongly recommend that you consult with a Certified Financial Planner® before making your social security benefit elections. While the interaction with a fee-based CFP® may cost you a few hundred dollars, making the wrong decision regarding your social security benefits could cost you thousands of dollars over your lifetime. You can also download a Financial Planner Budget Worksheet to give you that extra help when sorting out your finances and monthly budgeting.

About Michael.........

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Social Security Loophole: Age 62+ With Kids In High School

There is a little known loophole in the social security system for parents that are age 62 or older with children still in high school or younger. Since couples are having children later in life this situation is becoming more common and it could equal big dollars for families that are aware of this social security filing strategy.

There is a little known loophole in the social security system for parents that are age 62 or older with children still in high school or younger. Since couples are having children later in life this situation is becoming more common and it could equal big dollars for families that are aware of this social security filing strategy.

Here is how it works. If you are age 62 or older and you have children under that age of 18, they can collect a social security benefit based on your earnings history equal to half of the parents social security benefit at normal retirement age. This amount could equal as much as $16,122 per year for one child for higher income earners. If you have multiple children the total annual amount paid to your family members could equal between 150% to $180% of your normal retirement benefit which could be in excess of $40,000 per year depending on your earnings history.

There are some key considerations. First, your children cannot collect on this “family benefit” until you have begun to collect your social security benefit. You can turn on your social security benefit as early as age 62 but they reduce the monthly amount that you receive if you turn on the benefit prior to your normal retirement age. However, it may make sense to do so depending on the amount of the family benefit paid and the duration of the benefit. If you wait until normal retirement age, you will receive a slightly higher social security benefit for yourself, but all of the social security dollars that could have been paid to your children is lost.

Second, if you are still working and your earned income exceeds certain thresholds this filing strategy may not be advantageous due to the earned income penalty. They reduce your social security benefit by $1 for every $2 earned over a given threshold ($16,920 in 2017). Not only is your social security benefit reduce but also the benefit to your dependents.

Due to these restrictions, this filing strategy yields that greatest benefit to parents that are either fully or partially retired, age 62 or older, with a child or children below the age of 18.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

How Much Money Do I Need To Save To Retire?

This is by far the most popular question that we come across as financial planners. You may have heard some of the "rules of thumb" like “80% of your current take-home pay” or “1 million dollars”. In reality, the answer varies greatly on an individual by individual basis. This article will outline the procedures that we follow as financial planners to help

poc

This is by far the most popular question that we come across as financial planners. You may have heard some of the "rules of thumb" like “80% of your current take-home pay” or “1 million dollars”. In reality, the answer varies greatly on an individual by individual basis. This article will outline the procedures that we follow as financial planners to help individuals answer this very important question.

Step 1: Estimate Your Annual Expenses In Retirement

The first step is to get a ballpark idea of what your annual expenses might look like in retirement. The best place to start is to list your current monthly and annual expenses. Then create a separate column labeled “expenses in retirement”. Whether you are 2 years, 10 years, or 20 years away from retirement the idea is to pretend as if you were retiring tomorrow and determining what your annual expenses might look like. Some of your expenses in retirement will be lower, others may be higher, but most people find that a lot of their current expenses will carry over at the same level into the retirement years. This is because most people have become accustom to a certain standards of living and they intend to maintain that standard of living in retirement. Here are a few important questions that you should ask yourself when forecasting your retirement expenses:

How much should I budget for health insurance?

Will I have a mortgage or debt when I retire?

Do I plan to move when I retire?

Since I will not be working, should I budget additional expenses for vacations and hobbies?

Will I need to keep my life insurance policies after I retire?

Step 2: Adjust Your Retirement Expenses For Inflation

Now that you have a ballpark number of your annual expenses in retirement, you will need to adjust those expenses for inflation. Inflation is just a fancy word for “the price of everything that we buy today will gradually go up in price over time”. If the price of a gallon of milk today is $2 then most likely 20 years from now that same gallon of milk will cost $3.51. A 75% increase!! Historically inflation has grown at a rate of about 3% per year. There are periods of time when the rate of inflation grows faster or slower but on average it grows at 3% per year.

Another way to look at inflation is $20,000 in today’s dollars will not buy the same amount of goods and services 10 years from now because inflation erodes the purchasing power of your $20,000. If I did my annual expense planner and it tells me that I need $50,000 per year in retirement to meet all of my estimated expenses, let’s look at what adjusting that $50,000 for inflation does over different periods of time assuming a 3% rate of inflation:

Today’s Dollars 5 Years From Now 10 Years From Now 20 Years From Now

$50,000 $56,275 $65,238 $87,675

In the above example, if I am retiring in 10 years, and my estimated annual expenses in retirement will be $50,000 in today’s dollars, by the time I retire 10 years from now my annual expenses will increase to $65,238 per year just to stay in the same place that I am in today. Also, inflation does not stop when you retire, it continues into the retirement years. If I am 50 today and plan to live until 90, I have to apply this inflation adjustment for 40 years. It’s clear to see how inflation can have a significant impact on the amount that you may need to withdrawal for your account to meet you estimated expenses at a future date.

Step 3: Gather The Information On Your Current Assets

Once you know your expenses, you now need to gather all of the information on your retirement accounts and pension plans. You should collect the most recent statement for all of your investment accounts (401K, 403B, IRA’s, brokerage accounts, stocks, etc.), pension statements (if applicable), obtain your most recent social security statement, and gather information on the other sources of income and/or assets that may be available when you retire. Such as:

Sale of a business

Downsizing the primary residence

Rental income

Part-time employment

Step 4: Project The Growth Of Your Retirement Assets

There are three main categories to consider when calculating the growth rate of your retirement assets:

Annual contributions

Withdrawals

Investment rate of return

For annual contributions, it’s determining which accounts you plan on making deposits too each year and how much? For most individuals, their employer sponsored retirement plan is the main source of new contributions to their retirement nest egg. If your employer makes regular employer contributions to your retirement plan, you should factor those in as well. For example, if I am contributing 8% of my pay into the plan and my employer is providing me with a 4% matching contributions, I would reasonably assume that I’m adding 12% of my pay to my 401(k) plan each year.

The most popular question that we get in this category is “how much should I be contributing each year to my retirement account with my employer?” We advise employees that they should have a goal of contributing 10% of their pay each year to their retirement accounts. This is an aggregate total between your personal contributions and the employer contributions. Even if you cannot reach that level right now, 10%+ is the target.

Let’s move onto the next category…….withdrawals. Pre-retirement withdrawals from retirement accounts have become much more common in recent years due largely to the rising cost of college education. Parents will take loans from their 401K/403B plans or take early withdrawals from IRA accounts to fulfill the need for additional income during the years that their children are in college. If part of your overall financial plan is to use your retirement accounts to pay for one-time expenses such as college, you will need to factor that into your projections.

The third variable to consider when determining the growth of your assets is the assumed annual rate of return on your investments. There are many items to consider when determining a reasonable annual rate of return for your accounts. Some of those considerations include:

Time horizon to retirement

Allocation of your portfolio (stocks vs bonds)

Concentrated holdings (10%+ of your portfolio allocated to a single investment)

Accumulation phase versus distribution phase

The answer to the question: “what rate of return should I expect from my retirement accounts?”, can really only be determine on a case by case basis. Using an unreasonable rate of return assumption can create a significant disconnect between your retirement projections versus what is likely to actually occur within your investment accounts. Be careful with this step.

Step 5: Factor In Taxes

Don’t forget about the lovely IRS. All assets are not treated equally from a tax standpoint. For most individuals, the majority of their retirement savings will be in pre-tax retirement vehicles such as 401(k), 403(b), and Traditional IRA’s. That means when you take distributions from those accounts, you will realize earned income, and have to pay tax. For example, if you have $400,000 in your 401K account and you are in the 25% tax bracket, $100,000 of that $400,000 will be lost to taxes as withdrawals are made from the account.

If you have after tax investment accounts, it’s possible that you may owe little to no taxes on withdrawals. However, if there are unrealized investment gains built up in your after tax investment accounts then you may owe capital gains tax when liquidating positons.

Also note, you may have to pay taxes on a portion of your social security benefit. The amount of your social security benefit that is taxable varies based on your level of income.

Step 6: Spend Down Your Assets

In the final step, you should run long term projections to illustrate the spend down of your assets in retirement. Here are the steps:Example

Start with your annual after tax expense number $60,000

Subtract social security less taxes: ($20,000)

Subtract pension payments less taxes (if applicable): ($10,000)

Annual Expenses Net SS and Pensions: $30,000

In the example above, this individual would need an additional $30,000 after-tax to meet their anticipated annual expenses in Year 1 of retirement. I stress “after-tax” because if all of the retirement assets are in a pre-tax retirement account then they would need to gross up their distributions for taxes to get to the $30,000 after tax. If it is assumed that $40,000 has to be withdrawn from an IRA each year, the 3% inflation rate is applied to the annual expenses, and the life expectancy of this individual is 20 years from the date that they retire, this individual would need to withdrawal $1,074,814 out of their retirement accounts over the next 20 years to meet their income needs.

Step 7: Identify Multiple Solutions

There are often times multiple roads to reach a destination and the same is true when planning for retirement. If you find that you assets are falling short of the amount that is needed to sustain your expenses in retirement, you should work with a knowledgeable financial planner to identify alternative solutions. It may help you to answer questions like:

If I decided to work part-time in retirement how much would I have to earn?

If I downsize my primary residence in retirement how does this impact the overall picture?

If I can’t retire at age 63, what age can I comfortably retire at?

What are the pros and cons of taking social security benefits prior to normal retirement age

I also encourage clients to spend time looking at their annual expenses. If you find that your are cutting it close on income versus expenses in retirement, it's usually easier to cut expenses than it is to create more income in the retirement year.

Michael Ruger

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

How is my Social Security Benefit Calculated?

The top two questions that we receive from individuals approaching retirement are:

What amount will I received from social security?

When should I turn on my social security benefits?

how is social security calculated

The top two questions that we receive from individuals approaching retirement are:

What amount will I received from social security?

When should I turn on my social security benefits?

Are you eligible to receive benefits?

As you work and pay taxes, you earn Social Security “credits.” In 2015, you earn one credit for each $1,220 in earnings—up to a maximum of four credits a year. The amount of money needed to earn one credit usually goes up every year. Most people need 40 credits (10 years of work) to qualify for benefits.

When will I begin receiving my social security benefit?

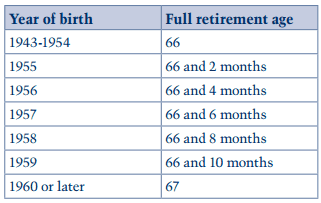

You are entitled to your full social security benefit at your “Normal Retirement Age” (NRA). Your NRA varies based on your date of birth. Below is the chart that social security uses to determine your “normal retirement age” or “full retirement age”:

social security retirement age

For example, if you were born in 1965, your NRA would be 67. At 67, you would be eligible for your full retirement benefit.

Delayed Retirement or Early Retirement

You can claim benefits as early as age 62, but your monthly check will be cut by 25% for the rest of your life. The way the math works out, for each year you take your social security benefit prior to your normal retirement age, you benefit is permanently reduce by 6% for each year you take it prior to your NRA.

On the opposite end of that scenario, if you delay claiming past your NRA, you will get a delayed credit of approximately 8% per year plus cost of living adjustments.

There are a number of variables that factor into this decision as to when to turn on your benefit. Some of the main factors are:

Your health

Do you plan to keep working?

What is your current tax bracket?

The amount of retirement savings that you have

Income difference between spouses

social security age chart

What amount will I receive from social security?

Social security uses a fairly complex formula for calculating social security retirement benefits but the short version is the formula uses your highest 35 years of income. If you have less than 35 years are income, zeros are entered into the average for the number of years you are short of 35 years of income. They also apply an inflation adjustment to your annual earnings in the calculation.

You can obtain your Social Security statement by creating an account at www.ssa.gov. Your statement contains lots of valuable information, such as:

Your estimated benefit amount at full retirement age

Eligibility for benefits

A detailed history of how much you've earned each year

Keep in mind that the figures in your statement are just estimates, and your eventual benefit amount could be quite different, especially if you're relatively young now.

Michael Ruger

About Michael……...