Potential Consequences of Taking IRA Distributions to Pay Off Debt

Once there is no longer a paycheck, retirees will typically meet expenses with a combination of social security, withdrawals from retirement accounts, annuities, and pensions. Social security, pensions, and annuities are usually fixed amounts, while withdrawals from retirement accounts could fluctuate based on need. This flexibility presents

Potential Consequences of Taking IRA Distributions to Pay Off Debt

Once there is no longer a paycheck, retirees will typically meet expenses with a combination of social security, withdrawals from retirement accounts, annuities, and pensions. Social security, pensions, and annuities are usually fixed amounts, while withdrawals from retirement accounts could fluctuate based on need. This flexibility presents opportunities to use retirement savings to pay off debt; but before doing so, it is important to consider the possible consequences.

Clients often come to us saying they have some amount left on a mortgage and they would feel great if they could just pay it off. Lower monthly bills and less debt when living on a fixed income is certainly good, both from a financial and psychological point of view, but taking large distributions from retirement accounts just to pay off debt may lead to tax consequences that can make you worse off financially.

Below are three items I typically consider before making a recommendation for clients. Every retiree is different so consulting with a professional such as a financial planner or accountant is recommended if you’d like further guidance.

Impact on State Income and Property Taxes

Depending on what state you are in, withdrawals from IRA’s could be taxed very differently. It is important to know how they are taxed in your state before making any big decision like this. For example, New York State allows for tax free withdrawals of IRA accounts up to a maximum of $20,000 per recipient receiving the funds. Once the $20,000 limit is met in a certain year, any distribution you take above that will be taxed.

If someone normally pulls $15,000 a year from a retirement account to meet expenses and then wanted to pull another $50,000 to pay off a mortgage, they have created $45,000 of additional taxable income to New York State. This is typically not a good thing, especially if in the future you never have to pull more than $20,000 in a year, as you would have never paid New York State taxes on the distributions.

Note: Another item to consider regarding states is the impact on property taxes. For example, New York State offers an “Enhanced STAR” credit if you are over the age of 65, but it is dependent on income. Here is an article that discusses this in more detail STAR Property Tax Credit: Make Sure You Know The New Income Limits.

What Tax Bracket Are You in at the Federal Level?

Federal income taxes are determined using a “Progressive Tax” calculation. For example, if you are filing single, the first $9,700 of taxable income you have is taxed at a lower rate than any income you earn above that. Below are charts of the 2019 tax tables so you can review the different tax rates at certain income levels for single and married filing joint ( Source: Nerd Wallet ).

There isn’t much of a difference between the first two brackets of 10% and 12%, but the next jump is to 22%. This means that, if you are filing single, you are paying the government 10% more on any additional taxable income from $39,475 – $84,200. Below is a basic example of how taking a large distribution from the IRA could impact your federal tax liability.

How Will it Impact the Amount of Social Security You Pay Tax on?

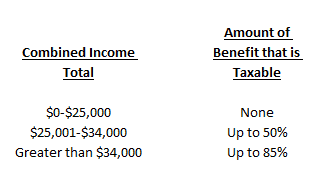

This is usually the most complicated to calculate. Here is a link to the 2018 instructions and worksheets for calculating how much of your Social Security benefit will be taxed ( IRS Publication 915 ). Basically, by showing more income, you may have to pay tax on more of your Social Security benefit. Below is a chart put together with information from the IRS to show how much of your benefit may be taxed.

To calculate “Combined Income”, you take your Adjusted Gross Income + Nontaxable Interest + Half of your Social Security benefit. For the purpose of this discussion, remember that any amount you withdraw from your IRA is counted in your Combined Income and therefore could make more of your social security benefit subject to tax.

Peace of mind is key and usually having less bills or debt can provide that, but it is important to look at the cost you are paying for it. There are times that this strategy could make sense, but if you have questions about a personal situation please consult with a professional to put together the correct strategy.

About Rob……...

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

STAR Property Tax Credit: Make Sure You Know The New Income Limits

The STAR Credit is a great way to reduce your property taxes in New York. If you are over the age of 65, it gets even better with the Enhanced STAR Credit. But you have to know the income limits associated with the credit otherwise you could unexpectedly lose the credit which could cost you thousands of dollars in additional property taxes. They

The STAR Credit is a great way to reduce your property taxes in New York. If you are over the age of 65, it gets even better with the Enhanced STAR Credit. But you have to know the income limits associated with the credit otherwise you could unexpectedly lose the credit which could cost you thousands of dollars in additional property taxes. They made some big changes to the credit that a lot of homeowners are not aware of. In this article we will review:

The income limits for the STAR Credit

Eligibility requirements for the Enhanced STAR Credit

How much money the STAR credit saves you

The most common mistakes that people make that disqualify them from the credit

The changes that were made to the property tax credit

STAR Property Tax Exemption

Let’s start with the basics. STAR stands for School Tax Relief. It’s a partial exemption from school taxes for your primary residence. There are two different STAR programs:

Basic STAR

Enhanced STAR

You Have To Apply For The Credit

You have to apply for the credit to receive it. It’s not automatic. Also, if you turn 65 this year and you want to further reduce your property taxes, there is a special application process for the Enhanced STAR Credit which requires you to enroll in the annual Income Verification Program (IVP). We will cover this in more detail later on in the article.

How Does The STAR Credit Work

The STAR credit exempts a specified dollar amount from the assessed value of your house prior to the calculation of your school tax bill. Here are the current exemption amounts:

Basic STAR: $30,000

Enhanced STAR: $65,000

The actual dollar amount that you save in school taxes will vary based on where you live in New York State. But if you live in a $300,000 house, you qualify for Basic STAR, and your school taxes before the STAR’s credit are $7,000. It could save you around $700 per year in school taxes. If you qualify for the enhanced STAR, you can more than double that savings number. In a high property tax state like New York, every little bit helps.

Income Limits For The STAR Credit

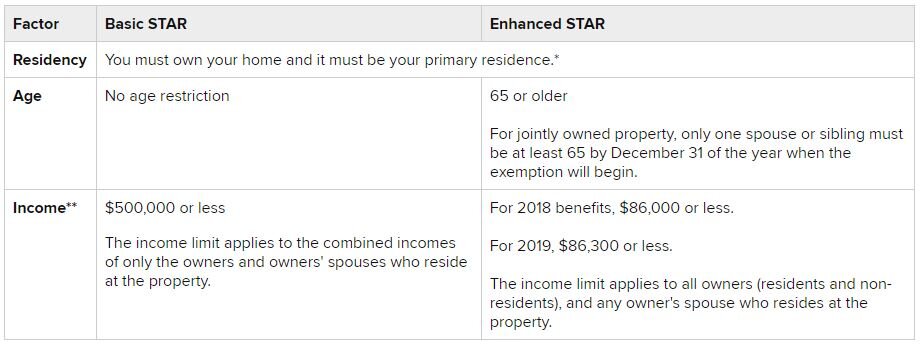

Here is a table from NYS Department of Taxation and Finance that summarizes the eligibility requirements for the Basic STAR and Enhanced STAR credit:

Requirement #1: It must be your primary residence. The credit does not apply for rental properties or second homes.

Requirement #2: To qualify for the Enhanced STAR, one of the homeowners must be age 65

Requirement #3: The income limitations. We see fewer issues with the Basic STAR since the income limit is $500,000. We see a lot more issues with the Enhanced STAR credit with the income limit at $86,300. Mainly because when you add up social security, pension payments, and required minimum distributions from IRA’s, you have homeowners that flirt with that income limit on a year by year basis. Crossing the income line would drop you back into the Basic STAR program which will most likely result in an unfriendly property tax surprise.

Income Calculation

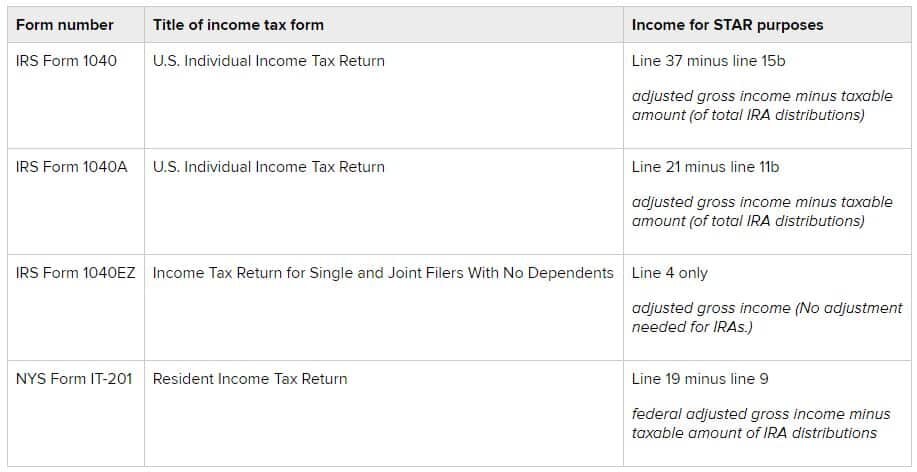

The eligibility for the 2019 STAR credit is actually based on your income from 2017. You can reference your 2017 federal and state tax returns against the table listed below:

Enhanced STAR Credit

Once you or your spouse turn age 65, you are then eligible to apply for the Enhanced STAR program.

Unlike the basic STAR program, the Enhanced STAR program required homeowners to file renewal applications with their local assessor each year to remain in the program. Under the new rules, new applicants are required to enroll in the Enhanced STAR Income Verification Process.

The application deadline is typically March 1st if you are filing at the county level but it can vary from county to county. You should contact your assessor to verify the application deadline in your area. The good news about enrolling in the Enhance STAR Income Verification Program is you only have to do it once. Once enrolled you will receive the Enhanced STAR credit each year as long as your income is below the required threshold.

Common Mistakes With The Enhanced STAR Credit

Since the income threshold for the Enhanced STAR program is much lower than the Basic STAR program this is where we see homeowners get into trouble. For most retirees, their income is relatively the same from year to year. However, there are frequently one-time events that occur that can push a retiree’s income higher for a given year. Not only do they end up with a large tax bill when they file their taxes but they also find out that they lost the Enhanced STAR Credit for that year. Double ouch!!

Here are the most common income events that retirees have to watch out for:

Capital gains and dividends from taxable investment accounts

Taking larger distributions from IRA’s or pre-tax retirement plans

Age 70 ½ - Required minimum distributions start from IRA’s

Receive an inheritance (some sources can be taxable)

Sell real estate or land other than the primary residence

Surrendering a life insurance policy

Part-time income

The year you turn on social security benefits

If you experience financial events that are expected to increase your taxable income for a given year, you should work closely with you financial advisor or accountant during those years because there may be ways to reduce your income to maintain the Enhanced STAR credit with some advanced planning.

Changes To The STAR Credit

New York made some significant changes to both the Basic STAR and the Enhanced STAR credit that not many homeowners are aware of. The amount of the credit did not change but the methods for applying for and receiving the credit did change.

If you were receiving the Basic STAR credit before and you have not moved since 2016, there is nothing that you have to do. Everything will continue to operate the same. However, if you move or if you are new homeowner, the STAR process will be different. Under the old method, you would simply see a deduction for your STAR credit on your school tax bill. Going forward, when you buy a new house, you will have to pay your full school tax bill, and then New York will mail you a physical check for your STAR credit. In order to receive your check in September, you must register for the Basic STAR program through the state Department of Taxation and Finance by July 1st.

After July 1st, you can still apply for the STAR credit, and the state will provide you with a check, but you may receive the check after September. The same manual check process is applicable with the Enhanced STAR program as well.

If you were receiving the Enhanced STAR and you have not moved, New York is allowing those homeowners to continue to file their renewal applications with their local assessor each year without having to enroll in the new Enhanced STAR Income Verification Program. However, if you move, you will have to enroll in the Income Verification Program in order to remain in the Enhanced STAR Program.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.