Roth Conversions In Retirement

Roth conversions in retirement are becoming a very popular tax strategy. It can help you to realize income at a lower tax rate, reduce your RMD’s, accumulate assets tax free, and pass Roth money onto your beneficiaries. However, there are pros and cons that you need to be aware of, because processing a Roth conversion involves showing more taxable income in a given year. Without proper tax planning, it could lead to unintended financial consequences such as:

· Social Security taxed at a higher rate

· Higher Medicare premiums

· Assets lost to a long term care event

· Higher taxes on long term capital gains

· Losing tax deductions and credits

· Higher property taxes

· Unexpected big tax liability

In this video, Michael Ruger will walk you through some of the strategies that he uses with his clients when implementing Roth Conversions. This can be a very effective wealth building strategy when used correctly.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Retirement Account Withdrawal Strategies

The order in which you take distributions from your retirement accounts absolutely matters in retirement. If you don’t have a formal withdraw strategy it could end up costing you in more ways than one. Click to read more on how this can effect you.

The order in which you take distributions from your retirement accounts absolutely matters in retirement. If you don’t have a formal withdraw strategy it could end up costing you more in taxes long-term, causing you to deplete your retirement assets faster, pay higher Medicare premiums, and reduce the amount of inheritance that your heirs would have received. Retirees will frequently have some combination of the following income and assets in retirement:

· Pretax 401(k) and IRA’s

· Roth IRA IRA’s

· After tax brokerage accounts

· Social Security

· Pensions

· Annuities

As Certified Financial Planner’s®, we look at an individual’s income needs, long-term goals, and map out the optimal withdraw strategy. In this article, I will be sharing with you some of the considerations that we use with our clients when determining the optimal withdrawal strategy.

Layer One : Pension Income

When you develop a withdrawal strategy for your retirement assets it’s similar to building a house. You have to start with a foundation which is taxable income that you expect to receive before you begin taking withdrawals from your retirement accounts. For retirees that have pensions, this is the first layer. Income from pensions are typically taxable income at the federal level but may or may not be taxable at the state level depending on which state you live in and who the sponsor of the pension plan is. While pensions are great, retirees that have pension income have to be very careful about how they make withdrawals from their retirement accounts because any withdraws from pre-tax accounts will stack up on top of their pension income making those withdrawal potentially subject to higher tax rates or cause you to lose tax deductions and credits that were previously received.

Layer Two: Social Security

Social Security income is also something that has to be factored into the mix. Most retirees will have to pay federal income tax on a large portion of their Social Security benefit. When we are counseling clients on their Social Security filing strategy, one of the largest influencers in that decision is what type of retirement accounts that have and how much is in each account. Delaying Social Security each year, increases the amount that an individual receives in the range of 6% to 8% per year forever. As financial planners, we view this as a “guaranteed rate of return” which is tough to replicate in other asset classes. Not turning your Social Security benefit prior to your normal retirement age can:

· Increase 50% spousal benefit

· Increase the survivor benefit

· Increase the value of SS cost of living adjustments

· Reduce the amount required to be withdrawn for other sources

For purposes of this article, we will just look at Social Security as another layer of income but know that depending on your financial situation your Social Security filing strategy does factor into your asset withdrawal strategy.

Roth Accounts: Last To Touch

In most situations, Roth assets are typically the last asset that you touch in retirement. Since Roth assets accumulate and are withdrawn tax free, they are by far the most valuable vehicle to accumulate wealth long-term. The longer they accumulate, the more valuable they are.

The other wonderful feature about Roth IRAs is that there is no required minimum distributions (RMD’s) at age 72. Meaning the government does not force you to take distributions once you have reached a certain age so you can continue to accumulate wealth within that asset class.

Roth’s are also one of the most valuable assets to pass onto beneficiaries because they can continue to accumulate tax free and are withdrawn tax free. For spousal beneficiaries, they can roll over the balance into their own Roth IRA and continue to accumulate wealth tax free. For non-spouse beneficiaries, under the new 10 year rule, they can continue to accumulate wealth for a period of up to 10 years after inheriting the Roth before they are required to distribute the full balance but they don’t pay tax on any of it.

Financial Nerd Note: While Roth are great accumulation vehicles, it’s impossible to protect them from a long term care event spend down situation. They cannot be transferred into a Medicaid trust and they are subject to full spend down for purposes of qualifying for Medicaid in New York since there is no RMD requirements. It’s just a risk that I want you to be aware of.

Pre-tax Assets

Pre-taxed retirement assets often include:

· Traditional & Rollover IRAs

· 401k / 403b / 457 plans

· Deferred compensation plans

· Qualified Annuities

When you withdraw money from these pre-tax sources you have to pay federal income tax on the amount withdrawn but you may also have to pay state income tax as well. If you live in a state that has state income tax, it’s very important to understand the taxation rules for retirement accounts within your state.

For example, New York has a unique rule that each person over the age of 59½ is allowed to withdraw $20,000 from a pre-tax retirement account without having to pay state income tax. Any amounts withdrawn over that threshold in a given tax year are subject to state income tax.

Pretax retirement accounts are usually subject to something called a required minimum distribution (RMD). The IRS requires you to start taking small distributions out of your pre-tax retirement accounts at 72. Without proper guidance, retirees often make the mistake of withdrawing from their after tax assets first, and then waiting until they are required to take the RMD’s from their pre-tax retirement accounts at age 72 and beyond. But this creates a problem for many retirees because it causes:

· The distribution to be subject to higher tax rates

· Loss of tax deductions and credits

· Increase the tax ability of Social Security Increase Medicare premiums Loss of certain property tax credits for

seniors

· Other adverse consequences……

Instead as planners, we proactively plan ahead and ask questions like:

“instead of waiting until age 72 and taking larger RMD’s from the pre-tax account, does it make sense to start making annual distribution from the pre-tax retirement accounts leading up to age 72, thus spreading those distribution in lower amounts, across more tax year resulting in:

· Lower tax liability

· Lower Medicare premiums

· Maintaining tax deductions and credits

· The assets last longer due to a lower aggregate tax liability

· More inheritance for their family members

Since everyone’s tax situation and retirement income situation is different, we have to work closely with their tax professional to determine what the right amount is to withdraw out of the pre-tax retirement accounts each year to optimize their net worth long-term.

After Tax Accounts

After tax assets can include:

· Savings accounts

· Brokerage accounts

· Non-qualified annuities

· Life Insurance with cash value

Just because I’m listing them as “after tax assets” does not mean the whole account value is free and clear of taxes. What I’m referring to is the accounts listed above typically have some “cost basis” meaning a portion of the account it what was originally contributed to the account and can be withdrawal tax fee. The appreciation within the account would be taxes at either ordinary income or capital gains rates depending on the type of the account and how long the assets have been held in the account.

Having after tax assets often provides retirees with a tax advantage because they may be able to “choose their tax rate” when they retire. Meaning they can choose to withdrawal “X” amount from an after tax source and pay little know taxes and show very little taxable income in any given year which opens the door for more long term advanced tax planning.

Withdrawal Strategies

Now that have covered all of the different types of retirement assets and how they are taxed, let move into some of the common withdrawal strategies that we use with our clients:

Retirees With All Three: Pre-tax, Roth, and After-tax Assets

When retirees have all three types of retirement account sources, the strategy usually involves leaving the Roth assets for last, and then meeting with their accountant to determine the amount that should be withdrawn out of their pre-tax and after tax accounts year to minimize the amount of aggregate taxes that they pay long term.

Example: Jim and Carol are both age 67 and just retired and they financial picture consists of the following:

Joint brokerage account: $200,000

401(k)’s: $500,000

Roth IRA‘s: $50,000

Combined Social Security: $40,000

Annual Expenses $100,000

Residents of New York State

An optimal withdrawal strategy may include the following:

Assuming we recommend that they turn on Social Security at their normal retirement age, it will provide them with $40,000 pre-tax Income, 85% of their Social Security benefit will be taxed at the federal level but there will be no state tax deal, resulting in an estimated $35,000 after tax.

That means we need an additional $65,000 after-tax per year from another source to meet their $100,000 per year in expenses. Instead of taking all the money from their joint brokerage account, we could have them rollover their 401(k) balances into Traditional IRAs and then take $20,000 distributions each from their accounts which they not have to pay state income tax on because it’s below the $20K threshold. That would result in another $40,000 in pre-tax income, translating to $35,000 after-tax.

The final $30,000 that is needed to meet their annual expenses would most likely come from their after tax brokerage account unless their accountant advises differently.

This strategy accomplishes a number of goals:

1) We are withdrawing pre-tax retirement assets in smaller increments and taking advantage of the New York

State tax free portion every year. This should result in lower total taxes paid over their lifetime as opposed to waiting until RMD’s start at age 72 and then being required to take larger distributions which could push them over the $20,000 annual limit making them subject in your state tax income tax and higher federal tax rates.

2) We are preserving the after-tax brokerage account for a longer period of time as opposed to using it all to supplement their expenses which would only last for about two years and then they would be forced to take all of their distributions from their pre-tax retirement account making them subject to a higher tax liability

3) For the Roth accounts, we are law allowing them to continue to accumulate as much as possible resulting in more tax free dollars to be withdrawn in the future, or if they pass onto their children, they are inheriting a larger assets that can be withdrawn tax free.

All Pre-Tax Retirement Savings

It’s not uncommon for retirees to have 100% of their retirement savings all within a pre-tax sources like 401(k)s, 403(b)s, traditional IRA‘s, and other types of pre-tax retirement account. This makes the withdrawal strategy slightly more tricky because if there are any big one-time expenses that are incurred during retirement, it forces the retiree to take a large withdrawal from a pre-tax source which also increases the tax liability associate the distribution.

A common situation that we often have to maneuver around is retirees that have plans to purchase a second house in retirement but in order to do that they need to have the cash to come up with a down payment. If they don’t have any after-tax retirement savings, those amounts will most likely have to come from a pre-tax account. Withdrawing $60,000 or more for a down payment can lead to a higher tax liability, higher Medicare premiums the following year, and make a larger portion of your Social Security taxable. For clients in the situation, we often have to plan a few year ahead, and will begin taking pre-text Distributions over multiple tax years leading up to the purchase of the retirement house in an effort to spread the tax liability over multiple years and avoiding the adverse tax and financial consequences of taking one large distribution.

Since many retirees are afraid of taking on debt in retirement, we often get the question in these second house situations is “Should I just take a big distribution from my retirement, pay for the house in full, and not have a mortgage?” If all of the retirement assets are tied up in pre-tax sources, it typically makes the most sense to take a mortgage which allows you to then take smaller distributions from your IRA accounts over multiple tax years to make the mortgage payments compared to taking an enormous tax hit by withdrawing $200,000+ out of a pre-tax return account in a single year.

Pensions With No Need For Retirement Accounts

For retirees that have pensions, it’s not uncommon for their pension and Social Security to provide enough income to meet all of their expenses. But these individual may also have pre-tax retirement accounts and the question becomes “what do we do with them if we don’t need them, and we expect the kids to inherit them?”

This situation often involves a Roth conversion strategy where each year we convert money from the pre-tax IRA’s over to Roth IRA’s. This allows those retirement accounts to accumulate tax free and ultimately withdrawn tax free by the beneficiaries. Versus if they continue to accumulate in pre-tax retirement accounts, the beneficiaries will have to distribute those accounts within 10 years and pay tax on the full balance.

Also when those retirees turn age 72 they have to start taking required minimum distributions which they don’t necessarily need. Since they are receiving pension and Social Security income, those distributions from the retirement accounts could be subject to higher tax rates. By proactively moving assets from a pre-tax source to a Roth source we are essentially reducing the amount of retirement assets that will be subject to RMD’s at age 72 because Roth assets are not subject to RMD‘s.

Using this Roth conversion strategy, it’s also not uncommon for us to have these retirees delay their Social Security. Since Social Security is taxable at the federal level, if we delay Social Security, it gives us more room to process larger Roth conversions because it free up those lower tax brackets. At the same time, it also allows Social Security to accumulate at a guaranteed rate of 6% - 8%.

Nerd Note: When you process these Roth conversions, make sure you’re taking into account the tax liability that’s being generated. You have to have a way to pay the taxes on the amounts converted because the money goes directly from your traditional IRA to your Roth IRA. Retirees that implement this strategy typically have large cash holdings, after tax retirement holdings, or we convert some of the money, and take pre-tax IRA distribution to cover the taxes.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Coronavirus RMD Relief: Ability To Waive Mandatory IRA Distributions In 2020

Congress passed the CARES Act in March 2020 which provides individuals with IRA, 401(k), and other employer sponsored retirement accounts, the option to waive their required minimum distribution (RMD) for the 2020 tax year.

Congress passed the CARES Act in March 2020 which provides individuals with IRA, 401(k), and other employer sponsored retirement accounts, the option to waive their required minimum distribution (RMD) for the 2020 tax year. This option is available to both individual over the age of 70½ and non-spouse beneficiaries of inherited IRA’s. In this article we will review:

The new RMD waiver rules

RMD’s for individuals age 70.5

RMD’s for beneficiaries of Inherited IRA’s

What happens if you already took your distribution for 2020?

Options for putting the RMD back into your IRA

Who Qualifies For The RMD Waiver?

Unlike other provisions in the CARES Act that require an individual to demonstrate that they have been impacted by the Coronavirus to gain access, the waiver of 2020 required minimum distributions is available to everyone. If you were age 70½ prior to December 31, 2019 or are the non-spouse beneficiary of an IRA, you are typically required to take a small distribution from your IRA each year, called an “RMD”, and pay tax on those distributions. However, for 2020, if you want to keep that money in your IRA in 2020 and avoid the tax hit associated with taking the distribution, you have the option to do so.

What If You Already Took Your RMD for 2020?

If you already received the RMD amount from your IRA for 2020, you may be able to return it to your IRA, and avoid the tax hit.

If the distribution came from your own personal IRA, not an inherited IRA, you will have two options:

OPTION 1: If the distribution happened within the last 60 days, you can simply return the money to your IRA. For this option, you are utilizing the 60-day rollover rule which allows you to take money out of an IRA, return it within 60 days, and avoid the tax liability. You are only allowed one 60-day rollover every 12 months.

OPTION 2: If the distribution took place more than 60 days ago, you will only be allowed to return it to your IRA if you qualify based on one of the four Coronavirus-Related Distribution criteria:

You, your spouse, or a dependent was diagnosed with the COVID-19

You are unable to work due to lack of childcare resulting from COVID-19

You own a business that has closed or is operating under reduced hours due to COVID-19

You have experienced adverse financial consequences as a result of being quarantined, furloughed, laid off, or having work hours reduced because of COVID-19

If you qualify under one of these items, then you will have 3-years from the date of the distribution to return the money back to your IRA and avoid the tax hit. However, while you have 3-years to return it to the IRA, if you don’t return the money to your IRA prior to December 31, 2020, you will have a tax liability in 2020 for all or a portion of that IRA distribution. It’s only when you actually return the money to your IRA that the tax liability is nullified. If you return it in a future tax year, you would have to go back and amend your 2020 tax return to recapture the taxes that were paid.

Inherited IRA – Non-spouse Beneficiary

However, if you are a non-spouse beneficiary of an IRA, the rules for returning the money to your IRA are different. If you are a non-spouse beneficiary of an IRA and you already received your RMD for 2020, you cannot return that money to your IRA to avoid the tax liability. Why is this? Beneficiaries are not eligible to make rollovers, so that disqualifies them from return the money to the IRA under the rollover rules in the CARES Act.

A Note To Our Greenbush Financial Clients

If you wish to waiver your RMD to 2020 or if have already received your RMD, and wish to process a rollover back into your IRA, 401(k), or employer sponsored plan, please contact us.

Michael Ruger

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

IRA RMD Start Date Changed From Age 70 ½ to Age 72 Starting In 2020

The SECURE Act was passed into law on December 19, 2019 and with it came some big changes to the required minimum distribution (“RMD”) requirements from IRA’s and retirement plans. Prior to December 31, 2019, individuals

The SECURE Act was passed into law on December 19, 2019 and with it came some big changes to the required minimum distribution (“RMD”) requirements from IRA’s and retirement plans. Prior to December 31, 2019, individuals were required to begin taking mandatory distributions from their IRA’s, 401(k), 403(b), and other pre-tax retirement accounts starting in the year that they turned age 70 ½. The SECURE Act delayed the start date of the RMD’s to age 72. But like most new laws, it’s not just a simple and straightforward change. In this article we will review:

Old Rules vs New Rules surrounding RMD’s

New rules surrounding Qualified Charitable Distributions from IRA’s

Who is still subject to the 70 ½ RMD requirement?

The April 1st delay rule

Required Minimum Distributions

A quick background on required minimum distributions, also referred to as RMD’s. Prior to the SECURE Act, when you turned age 70 ½ the IRS required you to take small distributions from your pre-tax IRA’s and retirement accounts each year. For individuals that did not need the money, they did not have a choice. They were forced to withdraw the money out of their retirement accounts and pay tax on the distributions. Under the current life expectancy tables, in the year that you turned age 70 ½ you were required to take a distribution equaling 3.6% of the account balance as of the previous year end.

With the passing of the SECURE Act, the start age from these RMD’s is now delayed until the calendar year that an individual turns age 72.

OLD RULE: Age 70 ½ RMD Begin Date

NEW RULE: Age 72 RMD Begin Date

Still Subject To The Old 70 ½ Rule

If you turned age 70 ½ prior to December 31, 2019, you will still be required to take RMD’s from your retirement accounts under the old 70 ½ RMD rule. You are not able to delay the RMD’s until age 72.

Example: Sarah was born May 15, 1949. She turned 70 on May 15, 2019 making her age 70 ½ on November 15, 2019. Even though she technically could have delayed her first RMD to April 1, 2020, she will not be able to avoid taking the RMD’s for 2019 and 2020 even though she will be under that age of 72 during those tax years.

Here is a quick date of birth reference to determine if you will be subject to the old 70 ½ start date or the new age 72 start date:

Date of Birth Prior to July 1, 1949: Subject to Age 70 ½ start date for RMD

Date of Birth On or After July 1, 1949: Subject to Age 72 start date for RMD

April 1 Exception Retained

OLD RULE: In the the year that an individual turned age 70 ½, they had the option to delay their first RMD until April 1st of the following year. This is a tax strategy that individuals engaged in to push that additional taxable income associated with the RMD into the next tax year. However, in year 2, the individual was then required to take two RMD’s in that calendar year: One prior to April 1st for the previous tax year and the second prior to December 31st for the current tax year.

NEW RULE: Unchanged. The April 1st exception for the first RMD year was retained by the SECURE Act as well as the requirement that if the RMD was voluntarily delayed until the following year that two RMD’s would need be taken in the second year.

Qualified Charitable Distributions (QCD)

OLD RULES: Individuals that had reached the RMD age of 70 ½ had the option to distribute all or a portion of their RMD directly to a charitable organization to avoid having to pay tax on the distribution. This option was reserved only for individuals that had reached age 70 ½. In conjunction with tax reform that took place a few years ago, this has become a very popular option for individuals that make charitable contributions because most individual taxpayers are no longer able to deduct their charitable contributions under the new tax laws.

NEW RULES: With the delay of the RMD start date to age 72, do individuals now have to wait until age 72 to be eligible to make qualified charitable distributions? The answer is thankfully no. Even though the RMD start date is delayed until age 72, individuals will still be able to make tax free charitable distributions from their IRA’s in the calendar year that they turn age 70 ½. The limit on QCDs is still $100,000 for each calendar year.

NOTE: If you plan to process a qualified charitable distributions from your IRA after age 70 ½, you have to be well aware of the procedures for completing those special distributions otherwise it could cause those distributions to be taxable to the owner of the IRA. See the article below for more on this topic:

ANOTHER NEW RULE: There is a second new rule associated with the SECURE Act that will impact this Qualified Charitable Distribution strategy. Under the old tax law, individuals were unable to contribute to Traditional IRA’s past the age of 70 ½. The SECURE Act eliminated that rule so individuals that have earned income past age 70 ½ will be eligible to make contributions to Traditional IRAs and take a tax deduction for those contributions.

As an anti-abuse provision, any contributions made to a Traditional IRA past the age of 70 ½ will, in aggregate, dollar for dollar, reduce the amount of your qualified charitable distribution that is tax free.

Example: A 75 year old retiree was working part-time making $20,000 per year for the past 3 years. To reduce her tax bill, she contributed $7,000 per year to a traditional IRA which is allowed under the new tax laws. This year she is required to take a $30,000 required minimum distribution (RMD) from her retirement accounts and she wants to direct that all to charity to avoid having to pay tax on the $30,000. Because she contributed $21,000 to a traditional IRA past the age of 70 ½, $21,000 of the qualified charitable distribution would be taxable income to her, while the remaining $9,000 would be a tax free distribution to the charity.

$30,000 QCD – $21,000 IRA Contribution After Age 70 ½ = $9,000 tax free QCD

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

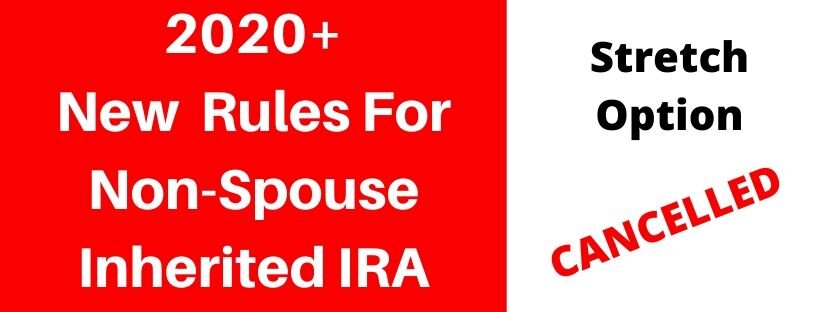

New Rules For Non Spouse Beneficiaries Of Retirement Accounts Starting In 2020

The SECURE Act was signed into law on December 19, 2019 and with it comes some very important changes to the options that are available to non-spouse beneficiaries of IRA’s, 401(k), 403(b), and other types of retirement accounts

The SECURE Act was signed into law on December 19, 2019 and with it comes some very important changes to the options that are available to non-spouse beneficiaries of IRA’s, 401(k), 403(b), and other types of retirement accounts starting in 2020. Unfortunately, with the passing of this law, Congress took away one of the most valuable distribution options available to non-spouse beneficiaries called the “stretch” provision. Non-spouse beneficiaries would utilize this distribution option to avoid the tax hit associated with having to take big distributions from pre-tax retirement accounts in a single tax year. This article will cover:

The old inherited IRA rules vs. the new inherited IRA rules

The new “10 Year Rule”

Who is grandfathered in under the old inherited IRA rules?

Impact of the new rules on minor children beneficiaries

Tax traps awaiting non spouse beneficiaries of retirement accounts

The “Stretch” Option Is Gone

The SECURE Act’s elimination of the stretch provision will have a big impact on non-spouse beneficiaries. Prior to January 1, 2020, non-spouse beneficiaries that inherited retirement accounts had the option to either:

Take a full distribution of the retirement account within 5 years

Rollover the balance to an inherited IRA and stretch the distributions from the retirement account over their lifetime. Also known as the “stretch option”.

Since any money distributed from a pre-tax retirement account is taxable income to the beneficiary, many non-spouse beneficiaries would choose the stretch option to avoid the big tax hit associated with taking larger distributions from a retirement account in a single year. Under the old rules, if you did not move the money to an inherited IRA by December 31st of the year following the decedent’s death, you were forced to take out the full account balance within a 5 year period.

On the flip side, the stretch option allowed these beneficiaries to move the retirement account balance from the decedent’s retirement account into their own inherited IRA tax and penalty free. The non-spouse beneficiary was then only required to take small distributions each year from the account called a RMD (“required minimum distribution”) but was allowed to keep the retirement account intact and continuing to accumulate tax deferred over their lifetime. A huge benefit!

The New 10 Year Rule

For non-spouse beneficiaries, the stretch option was replaced with the “10 Year Rule” which states that the balance in the inherited retirement account needs to be fully distributed by the end of the 10th year following the decedent’s date of death. The loss of the stretch option will be problematic for non-spouse beneficiaries that inherit sizable retirement accounts because they will be forced to take larger distributions exposing those pre-tax distributions to higher tax rates.

No RMD Requirement Under The 10 Year Rule

Even though the stretch option has been lost, beneficiaries will have some flexibility as to the timing of when distributions will take place from their inherited IRA. Unlike the stretch provision that required the non-spouse beneficiary to start taking the RMD’s the year following the decedent’s date of death, there are no RMD requirements associated with the new 10 year rule. Meaning in extreme cases, the beneficiary could choose not to take any distributions from the retirement account for 9 years and then in year 10 distribute the full account balance.

Now, unless you love paying taxes, very few people would elect to distribute a large pre-tax retirement account balance in a single tax year but the new rules give you a decade to coordinate a distribution strategy that will help you to manage your tax liability under the new rules.

Tax Traps For Non-Spouse Beneficiaries

These new inherited IRA distribution rules are going to require pro-active tax and financial planning for the beneficiaries of these retirement accounts. I’m lumping financial planning into that mix because taking distributions from pre-tax retirement accounts increases your taxable income which could cause the following things to happen:

Reduce the amount of college financial aid that your child is receiving

Increase the amount of your social security that is considered taxable income

Loss of property tax credits such as the Enhanced STAR Program

Increase your Medicare Part B and Part D premiums the following year

You may phase out of certain tax credits or deductions that you were previously receiving

Eliminate your ability to contribute to a Roth IRA

Loss of Medicaid or Special Needs benefits

Ordinary income and capital gains taxed at a higher rate

You really have to plan out the next 10 years and determine from a tax and financial planning standpoint what is the most advantageous way to distribute the full balance of the inherited IRA to minimize the tax hit and avoid triggering an unexpected financial consequence associated with having additional income during that 10 year period.

Who Is Grandfathered In?

If you are the non-spouse beneficiary of a retirement account and the decedent passed away prior to January 1, 2020, you are grandfathered in under the old inherited IRA rules. Meaning you are still able to utilize the stretch provision. Here are a few examples:

Example 1: If you had a parent pass away in 2018 and in 2019 you rolled over their IRA into your own inherited IRA, you are not subject to the new 10 year rule. You are allowed to stretch the IRA distributions over your lifetime in the form of those RMD’s.

Example 2: On December 15, 2019, you father passed away and you are listed as the beneficiary on his 401(k) account. Since he passed away prior to January 1, 2020, you would still have the option of setting up an Inherited IRA prior to December 31, 2020 and then stretching the distributions over your lifetime.

Example 3: On February 3, 2020, your uncle passes away and you are listed as a beneficiary on his Rollover IRA. Since he passed away after January 1, 2020, you would be required to distribute the full IRA balance prior to December 31, 2030.

You are also grandfathered in under the old rules if:

The beneficiary is the spouse

Disabled beneficiaries

Chronically Ill beneficiaries

Individuals who are NOT more than 10 years younger than the decendent

Certain minor children (see below)

Even beyond 2020, the beneficiaries listed above will still have the option to rollover the balance into their own inherited IRA and then stretch the required minimum distributions over their lifetime.

Minor Children As Beneficiaries

The rules are slightly different if the beneficiary is the child of the decedent AND they are still a minor. I purposely capitalized the word “and”. Within the new law is a “Special Rule for Minor Children” section that states if the beneficiary is a child of the decedent but has not reached the age of majority, then the child will be able to take age-based RMD’s from the inherited IRA but only until they reach the age of majority. Once they are no longer a minor, they are required to distribute the remainder of the retirement account balance within 10 years.

Example: A mother and father pass away in a car accident and the beneficiaries listed on their retirement accounts are their two children, Jacob age 10, and Sarah age 8. Jacob and Sarah would be able to move the balances from their parent’s retirements accounts into an inherited IRA and then just take small required minimum distributions from the account based on their life expectancy until they reach age 18. In their state of New York, age 18 is the age of majority. The entire inherited IRA would then need to be fully distributed to them before the end of the calendar year of their 28th birthday.

This exception only applies if they are a child of the decedent. If a minor child inherits a retirement account from a non-parent, such as a grandparent, then they are immediately subject to the 10 year rule.

Note: the age of majority varies by state.

Plans Not Impacted Until January 1, 2022

The replacement of the stretch option with the new 10 Year Rule will impact most non-spouse beneficiaries in 2020. There are a few exceptions to that effective date:

403(b) & 457 plans sponsored by state and local governments, including Thrift Savings Plans sponsored by the Federal Government will not lose the stretch option until January 1, 2022

Plans maintained pursuant to a collective bargaining agreement also do not lose the stretch option until January 1, 2022

Advanced Planning

Under the old inherited IRA rules there was less urgency for immediate tax planning because the non-spouse beneficiaries just had to move the money into an inherited IRA the year after the decedent passed away and in most cases the RMD's were relatively small resulting in a minimal tax impact. For non-spouse beneficiaries that inherit a retirement account after January 1, 2020, it will be so important to have a tax plan and financial plan in place as soon as possible otherwise you could lose a lot of your inheritance to higher taxes or other negative consequences associated with having more income during those distribution years.

Please feel free to contact us if you have any questions on the new inherited IRA rules. We would also be more than happy to share with you some of the advanced tax strategies that we will be using with our clients to help them to minimize the tax impact of the new 10 year rule.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Understanding Required Minimum Distributions & Advanced Tax Strategies For RMD's

A required minimum distribution (RMD) is the amount that the IRS requires you to take out of your retirement account each year when you hit a certain age or when you inherit a retirement account from someone else. It’s important to plan tax-wise for these distributions because they can substantially increase your tax liability in a given year;

Understanding Required Minimum Distributions & Advanced Tax Strategies For RMD’s

A required minimum distribution (RMD) is the amount that the IRS requires you to take out of your retirement account each year when you hit a certain age or when you inherit a retirement account from someone else. It’s important to plan tax-wise for these distributions because they can substantially increase your tax liability in a given year; consequentially, not distributing the correct amount from your retirement accounts will invite huge tax penalties from the IRS. Luckily, there are advanced tax strategies that can be implemented to help reduce the tax impact of these distributions, as well as special situations that exempt you from having to take an RMD.

Age 72

LAW CHANGE: There were changes to the RMD age when the SECURE Act was passed into law on December 19, 2019. Prior to the law change, you were required to start taking RMD’s in the calendar year that you turned age 70 1/2. For anyone turning age 70 1/2 after December 31, 2019, their RMD start age is now delayed to age 72.

The most common form of required minimum distribution is age 72. In the calendar year that you turn 72, you are required to take your first distribution from your pretax retirement accounts.

The IRS has a special table called the “Uniform Lifetime Table”. There is one column for your age and another column titled “distribution period”. The way the table works is you find your age and then identify what your distribution period is. Below is the calculation step by step:

1) Determine your December 31 balance in your pre-tax retirement accounts for the previous year end

2) Find the distribution period on the IRS uniform lifetime table

3) Take your 12/31 balance and divide that by the distribution period

4) The previous step will result in the amount that you are required to take out of your retirement account by 12/31 of that year

Example: If you turn age 72 in March of 2023, you would be required to take your first RMD in that calednar year unless you elect the April 1st delay in the first year. After you find your age on the IRS uniform lifetime table, next to it you will see a distribution period of 25.6. The balance in your traditional IRA account on December 31, 2018 was $400,000, so your RMD would be calculated as follows:

$400,000 / 25.6 = $15,625

Your required minimum distribution amount for the 2023 tax year is $15,625. The first RMD will represent about 3.9% of the account balance, and that percentage will increase by a small amount each year.

RMD Deadline

There are very important dates that you need to be aware of once you reach age 72. In most years, you have to make your required minimum distribution prior to December 31 of that tax year. However, there is an exception for the year that you turn age 72. In the year that you turn 72, you have the option of taking your first RMD either prior to December 31 or April 1 of the following year. The April 1 exception only applies to the year that you turn 72. Every year after that first year, you are required to take your distribution by December 31st.

Delay to April 1st

So why would someone want to delay their first required minimum distribution to April 1? Since the distribution results in additional taxable income, it’s about determining which tax year is more favorable to realize the additional income.

For example, you may have worked for part of the year that you turned age 72 so you’re showing earned income for the year. If you take the distribution from your IRA prior to 12/31 that represents more income that you have to pay tax on which is stacked up on top of your earned income. It may be better from a tax standpoint to take the distribution in the following January because the amount distributed from your retirement account will be taxed in a year when you have less income.

Very important rule:

If you decide to delay your first required minimum distribution past 12/31, you will be required to take two RMD‘s in that following year.

Example: I retire from my company in September 2023 and I also turned 72 that same year. If I elect to take my first RMD on February 1, 2024, prior to the April 1 deadline, I will then be required to take a second distribution from my IRA prior to December 31, 2024.

If you are already retired in the year that you turn age 72 and your income level is going to be relatively the same between the current year and the following year, it often makes sense to take your first RMD prior to December 31st, so are not required to take two RMD‘s the following year which can subject those distributions to a higher tax rate and create other negative tax events.

IRS Penalty

If you fail to distribute the required amount by the given deadline, the IRS will be kind enough to assess a 50% penalty on the amount that you should have taken for your required minimum distribution. If you were required to take a $14,000 distribution and you failed to do so by the applicable deadline, the IRS will hit you with a $7,000 penalty. If you make the distribution, but the amount is not sufficient enough to meet the required minimum distribution amount, they will assess the 50% penalty on the shortfall instead. Bottom line, don’t miss the deadline.

Exceptions If You Are Still Working

There is an exception to the 72 RMD rule. If your only retirement asset is an employer sponsored retirement plan, such as a 401(k), 403(b), or 457, as long as you are still working for that employer, you are not required to take an RMD from that retirement account until after you have terminated from employment regardless of your age.

Example: You are age 73 and your only retirement asset is a 401(k) account with your current employer with a $100,000 balance, you will not be required to take an RMD from your 401(k) account in that year even though you are over the age of 72.

In the year that you terminate employment, however, you will be required to take an RMD for that year. For this reason, be very careful if you’re working over the age of 72 and leave employment in late December. Your retirement plan provider will have a very narrow window of time to process your required minimum distribution prior to the December 31st deadline.

This employer sponsored retirement plan exception only applies to balances in your current employer’s retirement plan. You do not receive this exception for retirement plan balances with previous employers.

If you have retirement account such as IRA’s or other retirement plan outside of your current employer’s plan, you will still be required to take RMD’s from those accounts, even though you are still working.

Advanced Tax Strategies

There are two advanced tax strategies that we use when individuals are age 72 and still working for a company that sponsors are qualified retirement plan.

It’s not uncommon for employees to have a retirement plans with their current employer, a rollover IRA, and some miscellaneous balance in retirement plans from former employers. Since you only have the exception to the RMD within your current employers plan, and most 401(k), 403(b), and 457 plans accept rollovers from IRAs and other qualified plans, it may be advantageous to complete rollovers of all those retirement accounts into your current employer’s plan so you can completely avoid the RMD requirement.

Strategy number two. If you are still working and you have access to an employer sponsored plan, you are usually able to make employee contributions pre-tax to the plan. If you are required to take a distribution from your IRA which results in taxable income, as long as you are not already maxing out your employee deferrals in your current employer’s plan, you can instruct payroll to increase your contributions to the plan to reduce your earned income by the amount of the required minimum distribution coming from your other retirement accounts.

Example: You are age 72 and working part time for an employer that gives you access to a 401(k) plan. Your 401(k) has a balance of $20,000 with that employer, but you also have a Rollover IRA with a balance of $200,000. In this case, you would not be required to take an RMD from your 401(k) balance, but you would be required to take an RMD from your IRA which would total approximately $7,500. Since the $7,500 will represent additional income to you in that tax year, you could turn around and instruct the payroll company to take 100% of your paychecks and put it pre-tax into your 401(k) account until you reach $7,500 which would wipe out the tax liability from the distribution that occurred from the IRA.

Or, if you have a spouse that still working and they have access to a qualified retirement plan, the same strategy can be implemented. Additionally, if you file a joint tax return, it doesn’t matter whose retirement plan it goes into because it’s all pre-tax at the end of the day.

5% or More Owner

Unfortunately, I have some bad news for business owners. If you are a 5% or more owner of the company, it does not matter whether or not you are still working for the company, you are required to take an RMD from the company’s employer sponsored retirement plan regardless. The IRS is well aware that the owner of the business could decide to work for two hours a week just to avoid required minimum distributions. Sorry entrepreneurs.

A Spouse That Is More Than 10 Years Younger

I mentioned above that the IRS has a uniform lifetime table for calculating the RMD amount. If your spouse is more than 10 years younger than you are, there is a special RMD table that you will need to use called the “joint life table” with a completely different set of distribution periods, so make sure you’re using the correct table when calculating the RMD amount.

Charitable contributions

There is also an advanced tax strategy that allows you to make contributions to charity directly from your IRA and you do not have to pay tax on those disbursements. The special charitable distributions from IRA’s are only allowed for individuals that are age 72 or older. If you regularly make contributions to a charity, church, or not for profit, or if you do not need the income from the RMD, this may be a great strategy to shelter what otherwise would have been more taxable income. There are a lot of special rules surrounding how these charitable contributions work. For more information on this strategy see the following article:

Lower Your Tax Bill By Directing Your Mandatory IRA Distributions To Charity

Roth IRA’s

You are not required to take RMD‘s from Roth IRA accounts at age 72, this is one of the biggest tax advantages of Roth IRAs.

Inherited IRA

When you inherit an IRA from someone else, those IRAs have their own set of required minimum distribution rules which vary from the rules at the age 72. The SECURE Act that was passed in 2019 split non-spouse beneficiaries of IRA into two categories. For individuals that inherited retirement accounts prior to December 31, 2019, they are still able to stretch the RMD over their lifetime and the required minimum distributions must begin by December 31st of the year following the decedent date of death. For individuals that inherited a retirement account after December 31, 2019, the New 10 Rule replaced the stretch option and no RMDs are required for non-spouse beneficiaries. For the full list of rule, deadlines, and tax strategies surrounding inherited IRA’s see the articles listed below:

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Beware of the 5 Year Rule for Your Roth Assets

Being able to save money in a Roth account, whether in a company retirement plan or an IRA, has great benefits. You invest money and when you use it during retirement you don't pay taxes on your distributions. But is that always the case? The answer is no. There is an IRS rule that you must take note of known as the "5 Year Rule". There are a number

Beware of the 5 Year Rule for Your Roth Assets

Being able to save money in a Roth account, whether in a company retirement plan or an IRA, has great benefits. You invest money and when you use it during retirement you don't pay taxes on your distributions. But is that always the case? The answer is no. There is an IRS rule that you must take note of known as the "5 Year Rule". There are a number of scenarios where this rule could impact you and rather than getting too much into the weeds, this post is meant to serve as a public service announcement so you are aware it exists.

Advantages of a Roth

As previously mentioned, the benefit of Roth assets is that the account grows tax deferred and if the distributions are "qualified" you don't have to pay taxes. This is compared to a Traditional IRA/401(k) where the full distribution is taxed at ordinary income tax rates and regular investment accounts where you pay taxes on dividends/interest each year and capital gains taxes when you sell holdings. A quick example of Roth vs. Traditional below:

Roth Traditional

Original Investment $ 10,000.00 $ 10,000.00

Earnings $ 10,000.00 $ 10,000.00

Total Account Balance $ 20,000.00 $ 20,000.00

Taxes (Assume 25%) $ - $ 5,000.00

Account Value at Distribution $ 20,000.00 $ 15,000.00

This all seems great, and it is, but there are benefits of both Roth and Traditional (Pre-Tax) accounts so don’t think you have to start moving everything to Roth now. This article gives more detail on the two different types of accounts and may help you decide which is best for you Traditional vs. Roth IRA’s: Differences, Pros, and Cons.

Qualified Disbursements

Note the “occurs at least five years after the year of the employee’s first designated Roth contribution”. This is the “5 Year Rule”. The other qualifications are the same for Traditional IRA’s, but the “5 Year Rule” is special for Roth money. Not always good to be special.

It seems pretty straight forward and in most cases it is. Open a Roth IRA, let it grow at least 5 years, and as long as I’m 59.5 my distributions are qualified. Someone who has Roth money in a 401(k) or other employer sponsored plan may think it is just as easy. That isn’t always the case. Typically, an employee retires, and they roll their retirement savings into a Traditional or a Roth IRA. Say I worked at the company for 10 years, and I now retire and want to use all the savings I’ve created for myself throughout the years. I can start taking qualified distributions from my Roth IRA because I started contributing 10 years ago, correct? Wrong! The time you we’re contributing to the Roth 401(k) is not transferred to the new Roth IRA. If you took distributions directly from the 401(k) and we’re at least 59.5 they would be qualified. In most cases however, people don’t start using their 401(k) money until retirement and most plans only allow for lump sum distributions once you are no longer with the company.

So what do you do?

Open a Roth IRA outside of the plan with a small balance well before you plan to use the money. If I fund a Roth IRA with $100, 10 years from now I retire and roll my Roth 401(k) into that Roth IRA, I have satisfied the 5 year rule because I opened that Roth IRA account 10 years ago. The clock starts on the date the Roth IRA was opened, not the date the assets are transferred in.

About Rob.........

Hi, I’m Rob Mangold. I’m the Chief Operating Officer at Greenbush Financial Group and a contributor to the Money Smart Board blog. We created the blog to provide strategies that will help our readers personally, professionally, and financially. Our blog is meant to be a resource. If there are questions that you need answered, please feel free to join in on the discussion or contact me directly.

Can I Open A Roth IRA For My Child?

Parents always want their children to succeed financially so they do everything they can to set them up for a good future. One of the options for parents is to set up a Roth IRA and we have a lot of parents that ask us if they are allowed to establish one on behalf of their son or daughter. You can, as long as they have earned income. This can be a

Parents will often ask us: “What type of account can I setup for my kids that will help them to get a head start financially in life"?”. One of the most powerful wealth building tools that you can setup for your children is a Roth IRA because all of accumulation between now and when they withdrawal it in retirement will be all tax free. If your child has $10,000 in their Roth IRA today, assuming they never make another deposit to the account, and it earns 8% per year, 40 years from now the account balance would be $217,000.

Contribution Limits

The maximum contribution that an individual under that age of 50 can make to a Roth IRA in 2022 is the LESSER of:

$6,000

100% of earned income

For most children between the age of 15 and 21, their Roth IRA contributions tend to be capped by the amount of their earned income. The most common sources of earned income for young adults within this age range are:

Part-time employment

Summer jobs

Paid internships

Wages from parent owned company

If they add up all of their W-2's at the end of the year and they total $3,000, the maximum contribution that you can make to their Roth IRA for that tax year is $3,000.

Roth IRA's for Minors

If you child is under the age of 18, you can still establish a Roth IRA for them. However, it will be considered a "custodial IRA". Since minors cannot enter into contracts, you as the parent serve as the custodian to their account. You will need to sign all of the forms to setup the account and select the investment allocation for the IRA. It's important to understand that even though you are listed as a custodian on the account, all contributions made to the account belong 100% to the child. Once the child turns age 18, they have full control over the account.

Age 18+

If the child is age 18 or older, they will be required to sign the forms to setup the Roth IRA and it's usually a good opportunity to introduce them to the investing world. We encourage our clients to bring their children to the meeting to establish the account so they can learn about investing, stocks, bonds, the benefits of compounded interest, and the stock market in general. It's a great learning experience.

Contribution Deadline & Tax Filing

The deadline to make a Roth IRA contribution is April 15th following the end of the calendar year. We often get the question: "Does my child need to file a tax return to make a Roth IRA contribution?" The answer is "no". If their taxable income is below the threshold that would otherwise require them to file a tax return, they are not required to file a tax return just because a Roth IRA was funded in their name.

Distribution Options

While many of parents establish Roth IRA’s for their children to give them a head start on saving for retirement, these accounts can be used to support other financial goals as well. Roth contributions are made with after tax dollars. The main benefit of having a Roth IRA is if withdrawals are made after the account has been established for 5 years and the IRA owner has obtained age 59½, there is no tax paid on the investment earnings distributed from the account.

If you distribute the investment earnings from a Roth IRA before reaching age 59½, the account owner has to pay income tax and a 10% early withdrawal penalty on the amount distributed. However, income taxes and penalties only apply to the “earnings” portion of the account. The contributions, since they were made with after tax dollar, can be withdrawal from the Roth IRA at any time without having to pay income taxes or penalties.

Example: I deposit $5,000 to my daughters Roth IRA and four years from now the account balance is $9,000. My daughter wants to buy a house but is having trouble coming up with the money for the down payment. She can withdrawal $5,000 out of her Roth IRA without having to pay taxes or penalties since that amount represents the after tax contributions that were made to the account. The $4,000 that represents the earnings portion of the account can remain in the account and continue to accumulate tax-free. Not only did I provide my daughter with a head start on her retirement savings but I was also able to help her with the purchase of her first house.

We have seen clients use this flexible withdrawal strategy to help their children pay for their wedding, pay for college, pay off student loans, and to purchase their first house.

Not Limited To Just Your Children

This wealth accumulate strategy is not limited to just your children. We have had grandparents fund Roth IRA's for their grandchildren and aunts fund Roth IRA's for their nephews. They do not have to be listed as a dependent on your tax return to establish a custodial IRA. If you are funded a Roth IRA for a minor or a college student that is not your child, you may have to obtain the total amount of wages on their W-2 form from their parents or the student because the contribution could be capped based on what they made for the year.

Business Owners

Sometime we see business owners put their kids on payroll for the sole purpose of providing them with enough income to make the $6,000 contribution to their Roth IRA. Also, the child is usually in a lower tax bracket than their parents, so the wages earned by the child are typically taxed at a lower tax rate. A special note with this strategy, you have to be able to justify the wages being paid to your kids if the IRS or DOL comes knocking at your door.

About Michael.........

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Spouse Inherited IRA Options

If your spouse passes away and they had either an IRA, 401(k), 403(b), or some other type of employer sponsored retirement account, you will have to determine which distribution option is the right one for you. There are deadlines that you will need to be aware of, different tax implications based on the option that you choose, forms that need to be

If your spouse passes away and they had either an IRA, 401(k), 403(b), or some other type of employer sponsored retirement account, you will have to determine which distribution option is the right one for you. There are deadlines that you will need to be aware of, different tax implications based on the option that you choose, forms that need to be completed, and accounts that may need to be established.

Spouse Distribution Options

As the spouse, if you are listed as primary beneficiary on a retirement account or IRA, you have more options available to you than a non-spouse beneficiary. Non-spouse beneficiaries that inherited retirement accounts after December 31, 2019 are required to fully distribution the account 10 years following the year that the decedent passed away. But as the spouse of the decedent, you have the following options:

Fulling distribute the retirement account with 10 years

Rollover the balance to an inherited IRA

Rollover the balance to your own IRA

To determine which option is the right choice, you will need to take the following factors into consideration:

Your age

The age of your spouse

Will you need to take money from the IRA to supplement your income?

Taxes

Cash Distributions

We will start with the most basic option which is to take a cash distribution directly from your spouse’s retirement account. Be very careful with this option. When you take a cash distribution from a pre-tax retirement account, you will have to pay income tax on the amount that is distributed to you. For example, if your spouse had $50,000 in a 401(k), and you decide to take the full amount out in the form of a lump sum distribution, the full $50,000 will be counted as taxable income to you in the year that the distribution takes place. It’s like receiving a paycheck from your employer for $50,000 with no taxes taken out. When you go to file your taxes the following year, a big tax bill will probably be waiting for you.

In most cases, if you need some or all of the cash from a 401(k) account or an IRA, it usually makes more sense to first rollover the entire balance into an inherited IRA, and then take the cash that you need from there. This strategy gives you more control over the timing of the distributions which may help you to save some money in taxes. If as the spouse, you need the $50,000, but you really need $30,000 now and $20,000 in 6 months, you can rollover the full $50,000 balance to the inherited IRA, take $30,000 from the IRA this year, and take the additional $20,000 on January 2nd the following year so it spreads the tax liability between two tax years.

10% Early Withdrawal Penalty

Typically, if you are under the age of 59½, and you take a distribution from a retirement account, you incur not only taxes but also a 10% early withdrawal penalty on the amount this is distributed from the account. This is not the case when you take a cash distribution, as a beneficiary, directly from the decedents retirement account. You have to report the distribution as taxable income but you do not incur the 10% early withdrawal penalty, regardless of your age.

IRA Options

Let's move onto the two IRA options that are available to spouse beneficiaries. The spouse has the decide whether to:

Rollover the balance into their own IRA

Rollover the balance into an inherited IRA

By processing a direct rollover to an IRA in either case, the beneficiary is able to avoid immediate taxation on the balance in the account. However, it’s very important to understand the difference between these two options because all too often this is where the surviving spouse makes the wrong decision. In most cases, once this decision is made, it cannot be reversed.

Spouse IRA vs Inherited IRA

There are some big differences comparing the spouse IRA and inherited IRA option.

There is common misunderstanding of the RMD rules when it comes to inherited IRA’s. The spouse often assumes that if they select the inherited IRA option, they will be forced to take a required minimum distribution from the account just like non-spouse beneficiaries had to under the old inherited IRA rules prior to the passing of the SECURE Act in 2019. That is not necessarily true. When the spouses establishes an inherited IRA, a RMD is only required when the deceases spouse would have reached age 70½. This determination is based on the age that your spouse would have been if they were still alive. If they are under that “would be” age, the surviving spouse is not required to take an RMD from the inherited IRA for that tax year.

For example, if you are 39 and your spouse passed away last year at the age of 41, if you establish an inherited IRA, you would not be required to take an RMD from your inherited IRA for 29 years which is when your spouse would have turned age 70½. In the next section, I will explain why this matters.

Surviving Spouse Under The Age of 59½

As the surviving spouse, if you are under that age of 59½, the decision between either establishing an inherited IRA or rolling over the balance into your own IRA is extremely important. Here’s why .

If you rollover the balance to your own IRA and you need to take a distribution from that account prior to reaching age 59½, you will incur both taxes and the 10% early withdrawal penalty on the amount of the distribution.

But wait…….I thought you said the 10% early withdrawal penalty does not apply?

The 10% early withdrawal penalty does not apply for distributions from an “inherited IRA” or for distributions to a beneficiary directly from the decedents retirement account. However, since you moved the balance into your own IRA, you have essentially forfeited the ability to avoid the 10% early withdrawal penalty for distributions taken before age 59½.

The Switch Strategy

There is also a little know “switch strategy” for the surviving spouse. Even if you initially elect to rollover the balance to an inherited IRA to maintain the ability to take penalty free withdrawals prior to age 59½, at any time, you can elect to rollover that inherited IRA balance into your own IRA.

Why would you do this? If there is a big age gap between you and your spouse, you may decide to transition your inherited IRA to your own IRA prior to age 59½. Example, let’s assume the age gap between you and your spouse was 15 years. In the year that you turn age 55, your spouse would have turned age 70½. If the balance remains in the inherited IRA, as the spouse, you would have to take an RMD for that tax year. If you do not need the additional income, you can choose to rollover the balance from your inherited IRA to your own IRA and you will avoid the RMD requirement. However, in doing so, you also lose the ability to take withdrawals from the IRA without the 10% early withdrawal penalty between ages 55 to 59½. Based on your financial situation, you will have to determine whether or not the “switch strategy” makes sense for you.

The Spousal IRA

So when does it make sense to rollover your spouse’s IRA or retirement account into your own IRA? There are two scenarios where this may be the right solution:

The surviving spouse is already age 59½ or older

The surviving spouse is under the age of 59½ but they know with 100% certainty that they will not have to access the IRA assets prior to reaching age 59½

If the surviving spouse is already 59½ or older, they do not have to worry about the 10% early withdrawal penalty.

For the second scenarios, even though this may be a valid reason, it begs the question: “If you are under the age of 59½ and you have the option of changing the inherited IRA to your own IRA at any time, why take the risk?”

As the spouse you can switch from inherited IRA to your own IRA but you are not allowed to switch from your own IRA to an inherited IRA down the road.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.

Lower Your Tax Bill By Directing Your Mandatory IRA Distributions To Charity

When you turn 70 1/2, you will have the option to process Qualified Charitable Distributions (QCD) which are distirbution from your pre-tax IRA directly to a chiartable organizaiton. Even though the SECURE Act in 2019 changed the RMD start age from 70 1/2 to age 72, your are still eligible to make these QCDs beginning the calendar year that you

When you turn 70 1/2, you will have the option to process Qualified Charitable Distributions (QCD) which are distribution from your pre-tax IRA directly to a chartable organization. Even though the SECURE Act in 2019 changed the RMD start age from 70 1/2 to age 72, your are still eligible to make these QCDs beginning the calendar year that you turn age 70 1/2. At age 72, you must begin taking required minimum distributions (RMD) from your pre-tax IRA’s and unless you are still working, your employer sponsored retirement plans as well. The IRS forces you to take these distributions whether you need them or not. Why is that? They want to begin collecting income taxes on your tax deferred retirement assets.

Some retirees find themselves in the fortunate situation of not needing this additional income so the RMD’s just create additional tax liability. If you are charitably inclined and would prefer to avoid the additional tax liability, you can make a charitable contribution directly from your IRA and avoid all or a portion of the tax liability generated by the required minimum distribution requirement.

It Does Not Work For 401(k)’s

You can only make “qualified charitable contributions” from an IRA. This option is not available for 401(k), 403(b), and other qualified retirement plans. If you wish to execute this strategy, you would have to process a direct rollover of your FULL 401(k) balance to a rollover IRA and then process the distribution from your IRA to charity.

The reason why I emphases the word “full” for your 401(k) rollover is due to the IRS “aggregation rule”. Assuming that you no longer work for the company that sponsors your 401(k) account, you are age 72 or older, and you have both a 401(k) account and a separate IRA account, you will need to take an RMD from both the 401(k) account and the IRA separately. The IRS allows you to aggregate your IRA’s together for purposes of taking RMD’s. If you have 10 separate IRA’s, you can total up the required distribution amounts for each IRA, and then take that amount from a single IRA account. The IRS does not allow you to aggregate 401(k) accounts for purposes of satisfying your RMD requirement. Thus, if it’s your intention to completely avoid taxes on your RMD requirement, you will have to make sure all of your retirement accounts have been moved into an IRA.

Contributions Must Be Made Directly To Charity

Another important rule. At no point can the IRA distribution ever hit your checking account. To complete the qualified charitable contribution, the money must go directly from your IRA to the charity or not-for-profit organization. Typically this is completed by issuing a “third party check” from your IRA. You provide your IRA provider with payment instructions for the check and the mailing address of the charitable organization. If at any point during this process you take receipt of the distribution from your IRA, the full amount will be taxable to you and the qualified charitable contribution will be void.

Tax Lesson

For many retirees, their income is lower in the retirement years and they have less itemized deductions since the kids are out of the house and the mortgage is paid off. Given this set of circumstances, it may make sense to change from itemizing to taking the standard deduction when preparing your taxes. Charitable contributions are an itemized deduction. Thus, if you take the standard deduction for your taxes, you no longer receive the tax benefit of your contributions to charity. By making IRA distributions directly to a charity, you are able to take the standard deduction but still capture the tax benefit of making a charitable contribution because you avoid tax on an IRA distribution that otherwise would have been taxable income to you.

Example: Church Offering

Instead of putting cash or personal checks in the offering each Sunday, you may consider directing all or a portion of your required minimum distribution from your IRA directly to the church or religious organization. Usually having a conversation with your church or religious organization about your new “offering structure” helps to ease the awkward feeling of passing the offering basket without making a contribution each week.

Example: Annual Contributions To Charity

In this example, let’s assume that each year I typically issue a personal check of $2,000 to my favorite charity, Big Brother Big Sisters, a not-for-profit organization. I’m turning 70½ this year and my accountant tells me that it would be more beneficial to take the standard deduction instead of itemizing. My RMD for the year is $5,000. I can contact my IRA provider, have them issuing a check directly to the charity for $2,000 and issue me a check for the remaining $3,000. I will only have to pay taxes on the $3,000 that I received as opposed to the full $5,000. I win, the charity wins, and the IRS kind of loses. I’m ok with that situation.

Don’t Accept Anything From The Charity In Return

This is a very important rule. Sometimes when you make a charitable contribution, as a sign of gratitude, the charity will send you a coffee mug, gift basket, etc. When this happens, you will typically get a letter from the charity confirming your contribution but the amount listed in the letter will be slightly lower than the actual dollar amount contributed. The charity will often reduce the contribution by the amount of the gift that was given. If this happens, the total amount of the charitable contribution fails the “qualified charitable contribution” requirement and you will be taxed on the full amount. Plus, you already gave the money to charity so you have spend the funds that you could use to pay the taxes. Not good

Limits

While this will not be an issue for many of us, there is a $100,000 per person limit for these qualified charitable contributions from IRA’s.

Summary

While there are a number of rules to follow when making these qualified charitable contributions from IRA’s, it can be a great strategy that allows retirees to continue contributing to their favorite charities, religious organizations, and/or not-for-profit organizations, while reducing their overall tax liability.

About Michael……...

Hi, I’m Michael Ruger. I’m the managing partner of Greenbush Financial Group and the creator of the nationally recognized Money Smart Board blog . I created the blog because there are a lot of events in life that require important financial decisions. The goal is to help our readers avoid big financial missteps, discover financial solutions that they were not aware of, and to optimize their financial future.